In recent months, the US bond yield curve has signaled financial markets unambiguously - the US Federal Reserve would raise rates quickly and sharply. Around 8 rate hikes are currently expected by year end. But the markets also seem to believe that this US monetary policy tightening should be followed by rate cuts from 2023 onwards since the consensus now anticipate a sharp slowdown in US growth as early as next year. "Stagflation" and "recession" are now among the most frequently searched terms on Google.

There is even talk of a "war recession", as the current macroeconomic cycle is unlike anything we have seen in recent decades. Indeed, recessions or sharp economic downturns usually result in lower inflation due to a slowdown in demand. But the current context is different: we could very well experience a downturn in demand while costs and inflation continue to rise or, at the very least, remain very high. This is due to the many supply shortages in the labour market, in the housing sector and of course in commodities.

It is quite possible that despite these downside risks to growth, central bankers will have no choice but to maintain their planned rate increases and liquidity withdrawals via quantitative tightening. Indeed, the gap between the current level of inflation and interest rates just looks too wide. A few figures to consider: the inflation rate in the US reached 8.5% over a 12-month rolling period in March. The last time price inflation reached this level was in 1981. At that time, the Fed funds rate was 13% compared with 0.33% today. It thus seems that the Federal Reserve still has a lot of catching up to do...

Of course, once the tightening of financial conditions would start to have a significant impact on the growth of the economy and the production of goods and services, it is quite possible that the Fed will abandon - or at least scale back - its restrictive monetary policy program. But it seems that such a scenario is well off the mark.

Indeed, several elements indicate that we are facing some structural inflation, i.e. not or only slightly affected by a potential drop in demand. Among the factors which could keep inflation high:

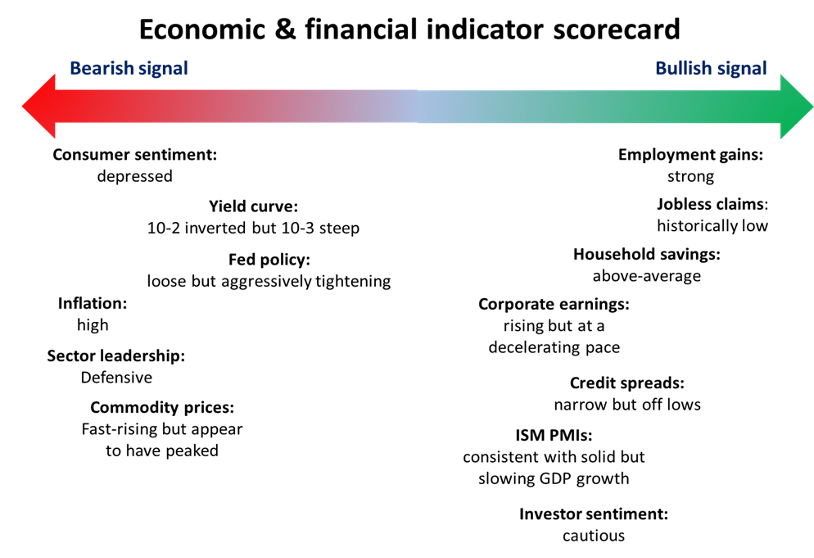

Many indicators suggest that the US economy is strong enough to avoid a collapse in demand. As mentioned above, inflation could remain high for a long time but growth seems to be strong enough to avoid the stagflation trap.

The most encouraging signals about the sustainability of this expansion come from the labour market. Historically, recessions have always been preceded by rising unemployment. But the figures point in the opposite direction. The number of job vacancies exceeds the number of unemployed by several millions. Claims for unemployment benefits are at their lowest level since 1968. There is therefore sufficient reason to believe that consumer incomes will continue to be buoyant for the rest of the year. And it seems unlikely that the tightness in the labour market will reverse any time soon. This is good news for the US consumer - who makes up 70% to 80% of US GDP. Moreover, the savings rate remains high and household debt is low, two other positive factors for the US economy.

Other reasons to be cheerful for America: companies are in good shape. Indeed, S&P 500 profits should grow by almost 10% this year, credit spreads remain relatively tight and leading indicators testify to the optimism of companies.

But there are also reasons to turn cautious. High energy prices and other inflationary pressures have already dented consumer confidence and pose a credible threat to economic growth. US household sentiment surveys have been depressed for several months now.

On the business side, the Purchasing Managers' Index (PMI) for March fell to its lowest level since September 2020 as new orders and production slowed significantly, indicating weakening demand. The withdrawal of Fed support and rising borrowing costs will likely lead to a slowdown of the economy in the coming months. And this will certainly be reflected in corporate earnings growth.

Finally, the market is also sending some very clear signals of caution. Let's start withMixe the US Treasury yield curve. As mentioned before, this may be a misinterpretation by the markets of the upcoming rate cycle. But in the past, the yield curve has often been a good early indicator (15 to 18 months) of a coming recession. Another signal of caution is the outperformance of defensive sectors (utilities, health care, etc.) relative to cyclical sectors.

Economic & financial indicator scorecard

Source: Edward Jones

In summary, the latest macroeconomic data indicates that growth is about to slow down, but also that the probability of a recession seems low for the time being. In our last investment committee meeting, we dismissed the "stagflation" scenario as the one with the highest probability of occurring. While we expect inflation to remain well above the Fed's targets, we also believe that growth should remain above the long-term trend.

However, we remain extremely vigilant. First because the current context is unprecedented; this means that a monetary policy accident (central bank staying too far behind the curve or panicking) remains a real risk.

Second because the current state of the economy - record levels of debt, high leverage, demanding valuations and high concentration of wealth - means that it is the financial markets that impact the real economy - not the other way around. Can the Fed reasonably expect inflation to slow when equity markets are near all-time highs and credit spreads are relatively tight? On the other hand, wouldn't a 20% to 30% drop in equity markets and a sharp widening of credit spreads send the US economy into recession?

As we know, the landing a plane is the most dangerous time for a pilot. For the Fed as well...

{kind=link}