The Facts

The Knowns

The Unknowns

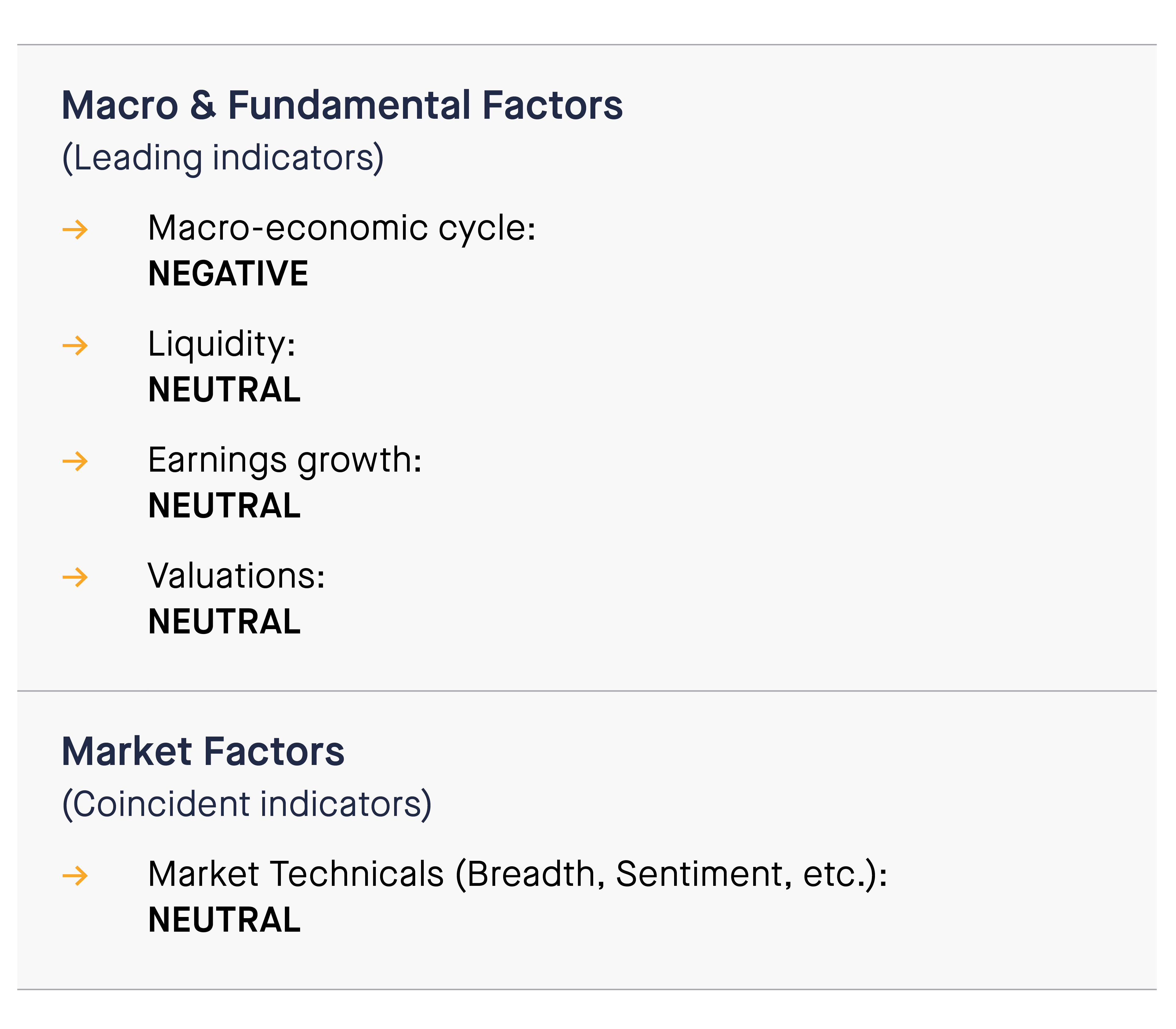

Indicator #1

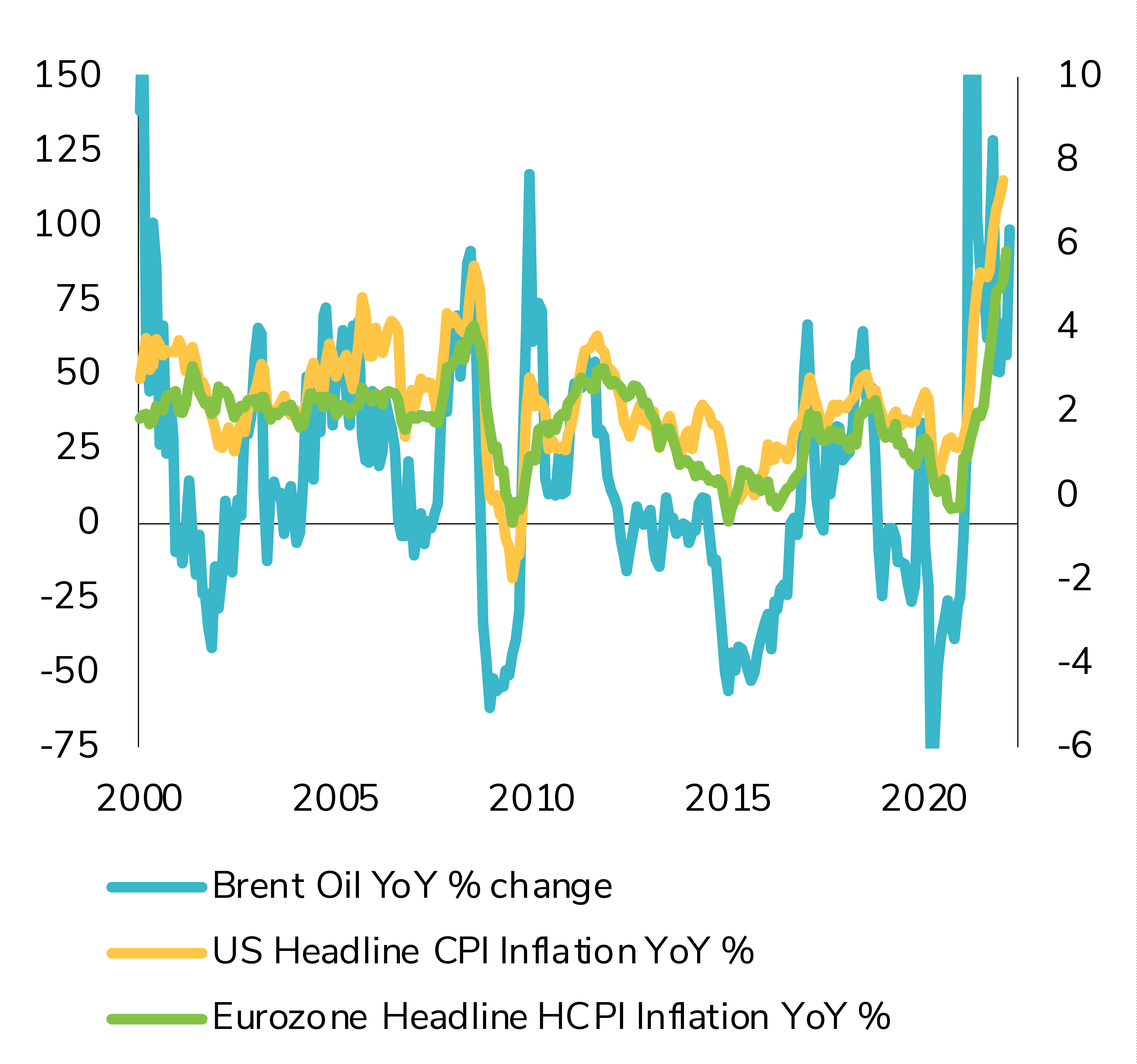

We believe that the macro perspective has deteriorated. Our “core” scenario for 2022 is adjusted toward slower growth and higher inflation. Global growth was expected to be above trend before the conflict. As of now, global growth remains firmly positive and the Omicron variant’s impact on the US and Europe has dissipated. However, the Ukraine/ Russia war is likely to decrease global real GDP growth by at least 1% due to rising energy prices, negative impact on global trade, deteriorating consumer and corporate sentiment and the risk of worsening financial and liquidity conditions. Meanwhile, inflation keeps rising in the US and in Europe and exceeds expectations. The Russia-Ukraine war is creating a supply shock with moderate to severe effects – depending on the sanctions. This should lead to higher inflation than expected. As such, our macro indicator has turned NEGATIVE (vs. positive previously).

Indicator #2

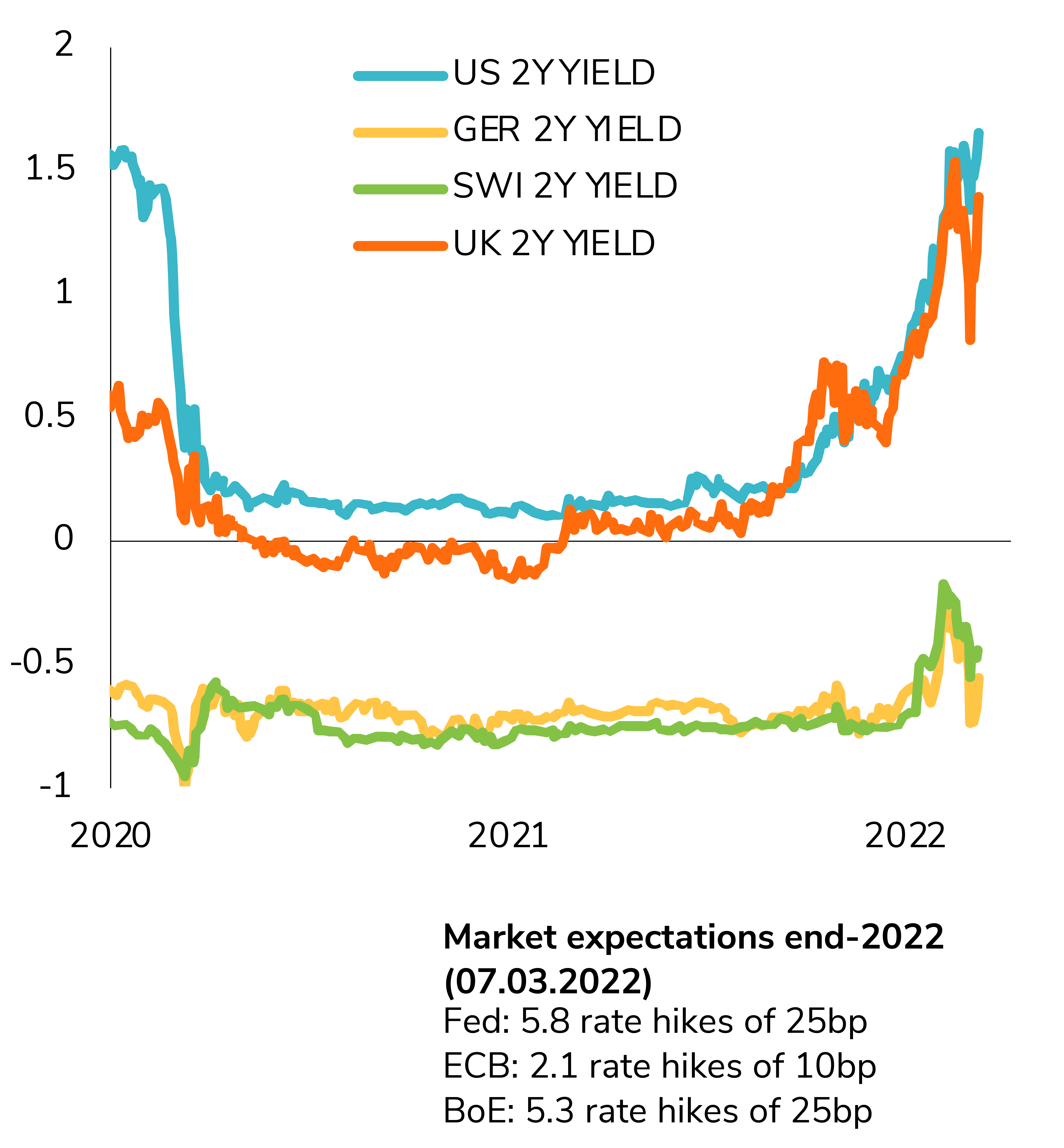

In the US, Monetary policy is unlikely to provide much support to the economy and financial markets. On the back of a strong job market and the highest inflation number over the last 40 years, the Fed will stick to its plan to hike rates and tighten liquidity despite the conflict. On the other hand, the European Central bank may be more cautious than expected regarding rate hikes and QE tapering. Should the geopolitical and financial crisis deepen, fiscal and/or monetary policy should come as a support not only in Europe but also in the US. For the time being, we view the liquidity conditions as NEUTRAL.

Indicator #3

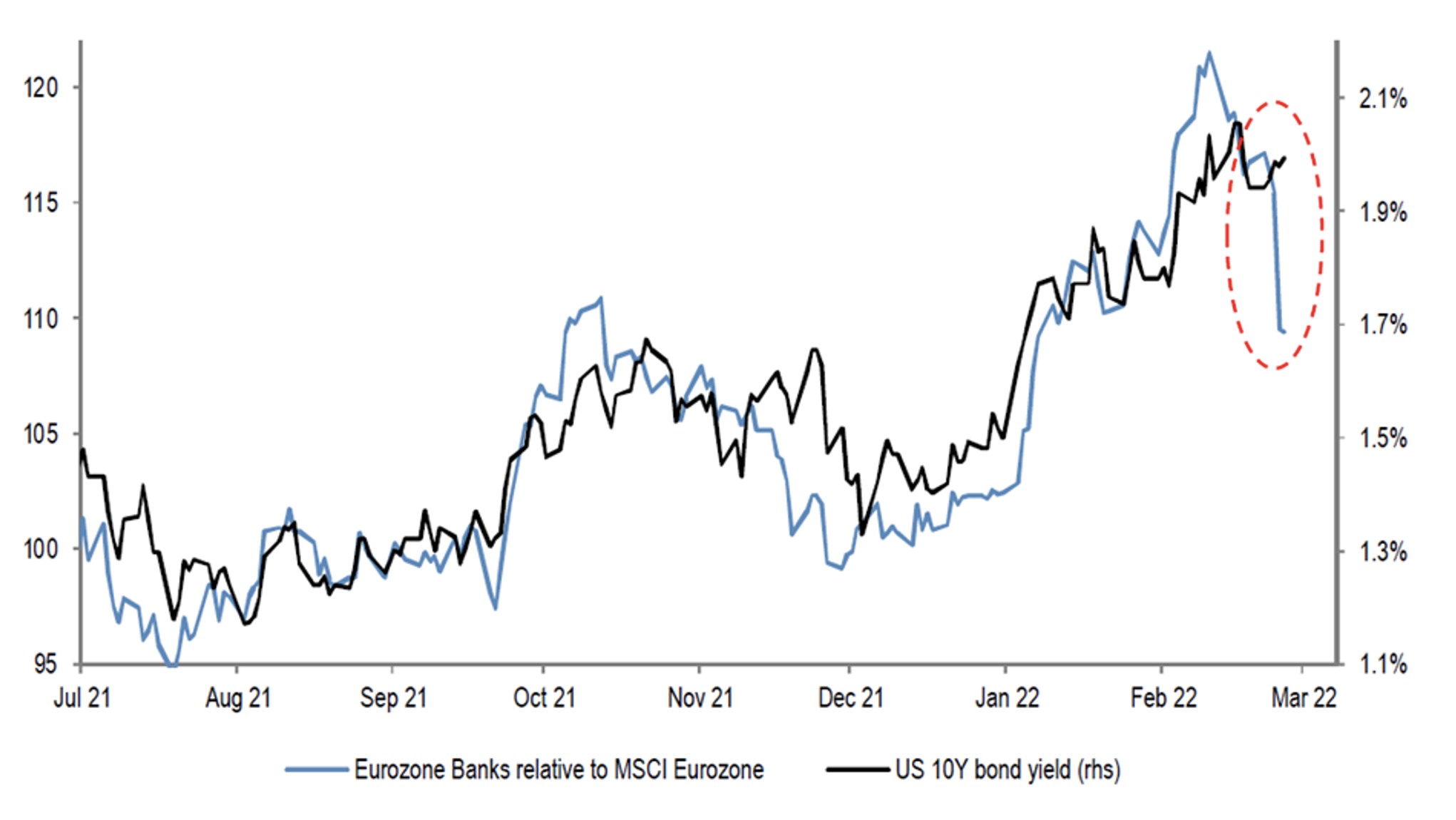

Earnings momentum remains positive but is likely to be revised downwards by sell-side consensus. As such, we are downgrading this indicator from positive to neutral. That being said, we still expect high single digit earnings growth in the US despite the downgrade. Share buybacks provide strong support, while value / cyclicals sectors benefit from rising commodity prices. In Europe, banks are suffering from Russian exposure and a flattening yield curve. We expect low to no growth for European earnings this year.

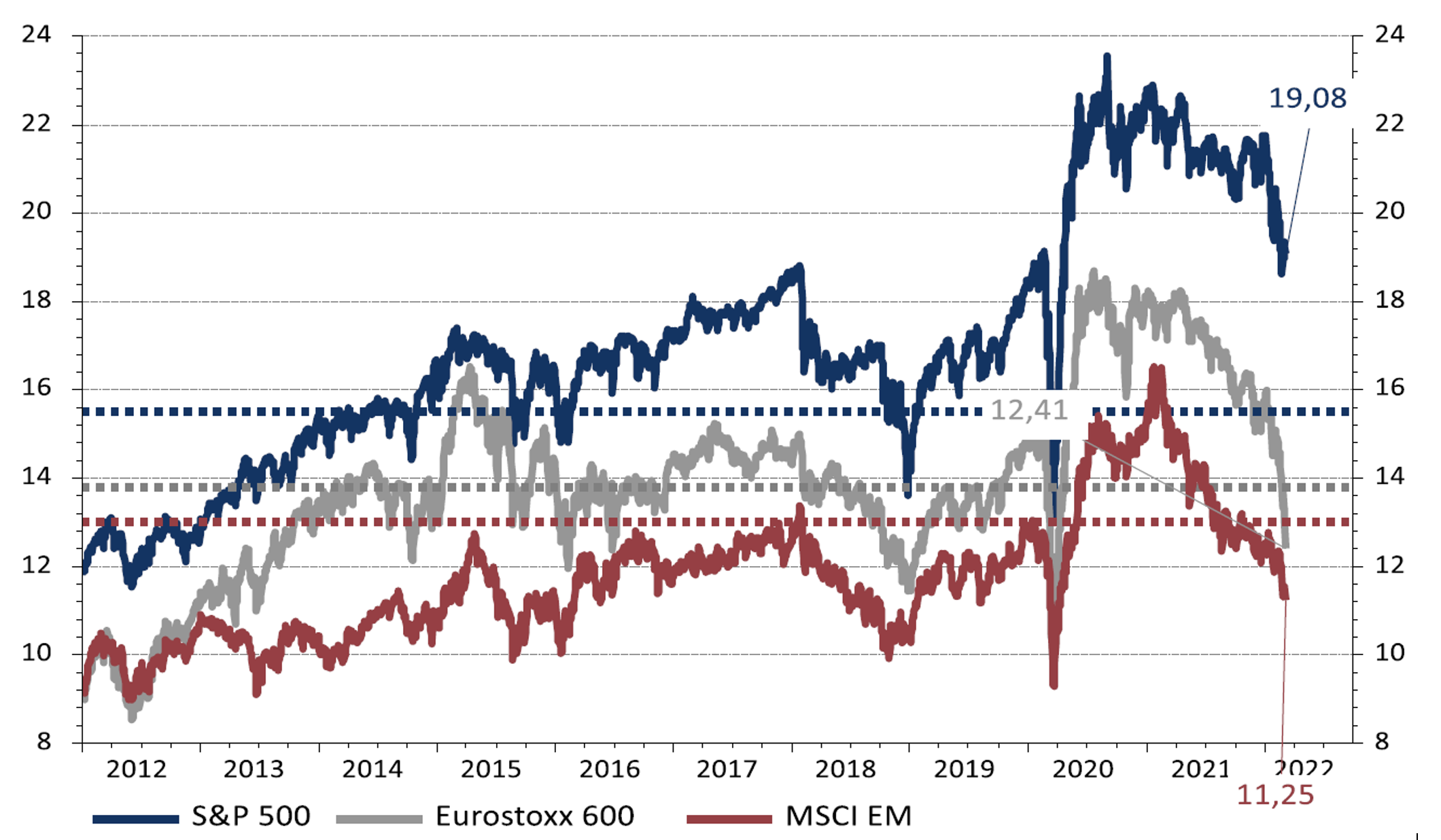

Indicator #4

Equity valuations have eased but are still above historical average in the US. We feel that increased geopolitical risk, growing economic sanctions against Russia and downgrades in earnings are not fully priced yet. As such, this indicator remains NEUTRAL.

Indicator #5

Our market indicators are NEUTRAL, which is a slight improvement vs. last month in the US but not in Europe. At the time of our writing, our proprietary technical indicators on the US market offer a rather positive picture on an aggregated basis. Some sentiment indicators are showing signs of stress and our market dynamic indicators show oversold conditions (which is a positive from a contrarian point of view). The US Bull-Bear gives a buy rating (over- pessimism) but the Put to Call ratio doesn’t show extreme stress at this stage. On the negative side, market breadth keeps deteriorating. The low frequency / long-term indicators show that the long-term bull trend (price above 200 days moving average) is at risk of being broken. We also note that the rate of change keeps deteriorating but hasn’t reached extreme negative levels. The volume signal gives a buy rating. Unlike the US, our European indicators give a negative signal on an aggregated basis, echoing the negative picture for Europe painted by macroeconomic and earnings growth prospects.

Based on the weight of the evidence, we are downgrading our equity view by another notch, from cautious to disinclination. Eurozone equities are moved from Positive to strong disinclination, UK and Switzerland from Positive to cautious and Japan from Preference to Positive.

On the fixed income side, we remain cautious on rates and keep a disinclination stance on Credit Spreads. Macro trends continue to support higher rates. Medium and long term inflation expectations spiked along with energy prices and amid fears of stagflation. EUR rates and sovereign spreads are capped by the pullback on ECB rate hikes expectations as uncertainty is high around Europe’s outlook. High yield and lower quality investment grade bonds should continue to suffer from declining liquidity, rising interest rates (investors will be less likely to seek lower ratings for high yields) and tight valuations. Investment grade spreads are back above 100 bps but are still below average in USD. We are downgrading Subordinated debt and Emerging Markets bonds (hard and local currencies) from Positive to cautious given uncertainties and likely downward revisions to the European and Global growth outlook.

We stay cautious on Commodities although the upside risk on energy prices remain high depending on the severity of the sanctions against Russia. The asset class remains very volatile and geopolitically driven. We thus favor gaining exposure to the asset class through commodities-sensitive stocks rather than pure plays. We are upgrading Gold from positive to preference. The yellow metal is one of the few portfolio diversifiers remaining. It benefits from lower real bond yields, geopolitical uncertainty and tight supply.

In Forex, we are downgrading our stance on EUR from positive to disinclination. The war in Ukraine weighs on EUR prospects from several angles: macroeconomic growth prospects, interest rate differentials and flows of funds.

We are also downgrading Sterling from positive to cautious while upgrading the Swiss franc from cautious to positive as Fundamental drivers plead for a firm CHF over the medium term. Flight to safety from European assets is a powerful support. Growth momentum differential has turned back negatively for the yen, which is still cheap from a valuation standpoint.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}