At Syz, we like to sail a course between exaggerations, and take advantage of them whenever possible. As we have laid out previously in our Japanification thesis, we believe the world will remain in a low growth, low rate environment. But there will be periods where inflation increases, due to an evolving and volatile macroeconomic picture. We are now experiencing such a reflationary spike, and this may accelerate and continue for some months to come.

We believe this scenario will provide a constructive platform for equities – particularly in cyclical sectors and among classic value plays, such as industrials, materials and financials. In parallel, we are cautious on global fixed income assets, given renewed momentum in long-term interest rates.

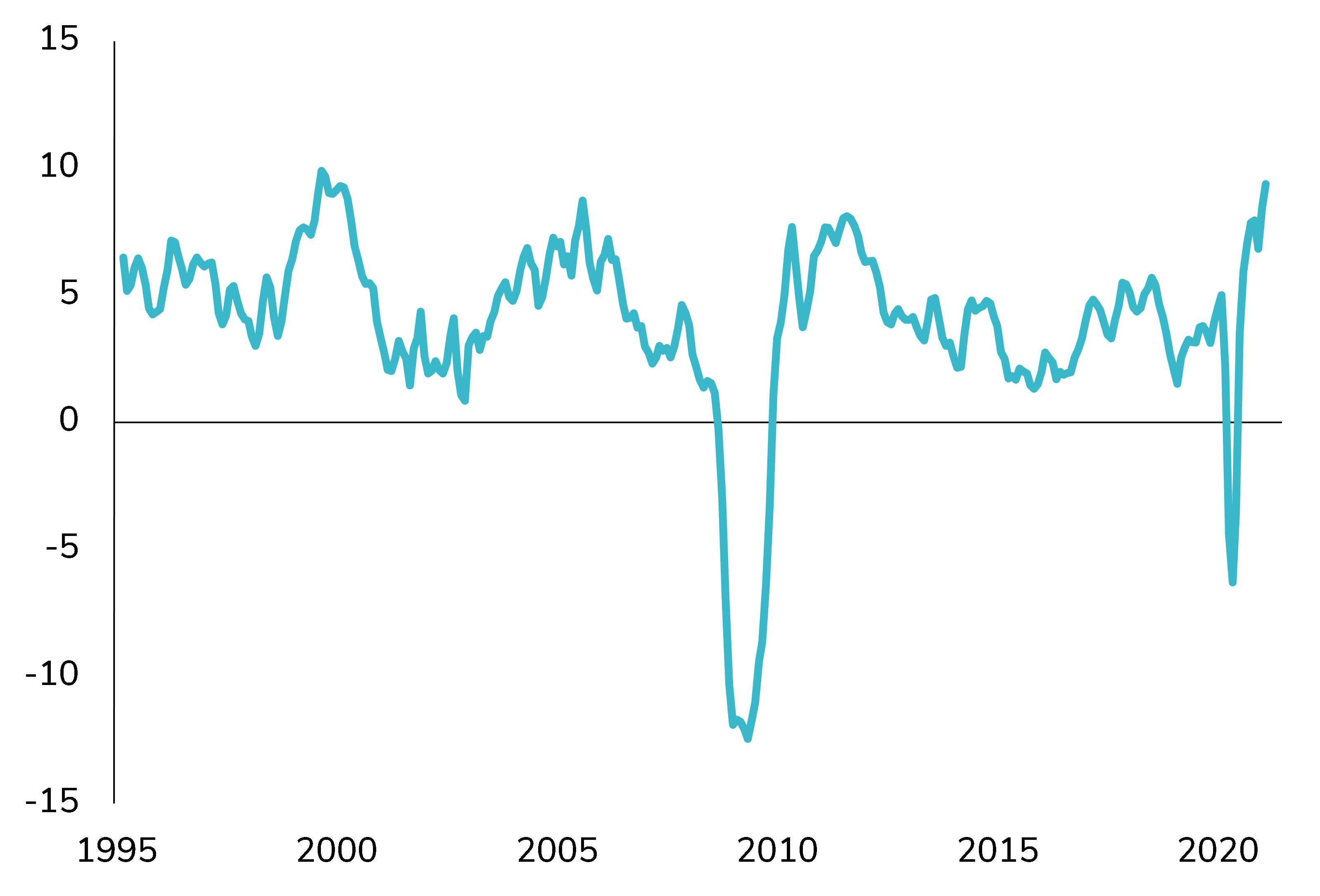

While business activity in the eurozone contracted again in February, as lockdown measures restricted the bloc’s dominant service industry, key surveys indicate factories had their busiest month in three years. This is a positive development underlining that while overall business activity may be subdued or even deteriorating, it is not collapsing as was the case in the first lockdown, when the world’s economies fell into the abyss.

This means the dynamics for the reflation scenario remain in place, both in terms of growth and inflation. Indeed, a firm bounce-back is now arguably the consensual trade. A boost to this narrative is the introduction of strengthening economic data coming from the US in terms of household consumption. The fiscal stimulus checks now arriving through the door will further strengthen purchasing power and should lead to an acceleration in demand during the spring.

Eventually, in the reflationary scenario, central bankers will have to act. This will be first by words, through forward guidance, and later through deeds, by slowing asset purchases and hiking rates. It is possible this could happen more quickly than anticipated, and markets are now starting to price such possibility as growth and inflation rise.

The prospect of an exit from the Covid crisis has finally created a sweet spot for value, while growth begins to stutter. We expect the vast chasm between the two styles to further close as the reflationary trade continues to play out. This mean tech and quality names will continue to be buffeted, while further gains are on the table for cyclicals.

With this backdrop in mind, we have continued what we started last November – repositioning the portfolios towards more cyclicality, reducing technology stocks and adding to financials, materials and industrials. This has allowed us to take profits and reduce our tech exposure, some of which was adversely impacted by the rise in long term interest rates.

Not all tech names are suffering equally. Outliers such as Tesla have experienced a correction, while quality names in our portfolio have performed strongly. For example, Alphabet has posted a 14%return year-to-date. Indeed, Alphabet is more of a communications company than pure tech, while Amazon principally resides in the world of discretionary consumption.

There is a lot of nuance in the sector, and we will be retaining names such as Mastercard and Visa, which we believe are far more than tech names, as they tap into deep long-term consumer trends.

We have recently added to our financials position. We are not making a specific play on Europe versus the US, but rather getting global exposure to banks that will benefit from rising interest rates. Their massive underperformance in the last decade will probably never be fully recouped, but we are at a tactical inflection point, and a reflationary mini-cycle will be a big tailwind for the sector.

We do not believe central banks will rush into normalising rate policy, save for some demonstrative moves to ward off bond vigilantes. Rather, they will attempt to contain any change in the current economic and financial market paradigm. This will likely translate into some incremental rear-guard action.

Our tactical positioning on more value-style cyclicals has paid off as the yield curve has steepened, but there could be more in store for inflation. Those expecting a hyper-inflation type of scenario seem to be wedded to a bygone scenario that suggests we are living in 1980s equity market boom conditions and ignores the seismic impact of demographic & technological changes, the Great Financial Crisis and its debt aftermath.

Our thesis absorbs the impact of an unprecedented monetary experiment, a characteristic of the potentially multi-decade Japanified environment we are in. Dynamic asset allocators will capitalise on reflationary spikes during this period, both on the upside and the downside, and avoid getting taper tantrums on the fixed income side.

While equities and the return of inflation look well supported in the coming months, we always keep an eye on anything that could threaten this scenario. This also means keeping our protections in the market, so if the market experiences acute drawdown, our losses will be capped. In the scenario where rates move far faster than the market expects, we could see some strong market gyrations, and it pays to have the appropriate market protections in place. We also maintain a gold position. A safe course means never sailing too close to the wind.

{kind=link}