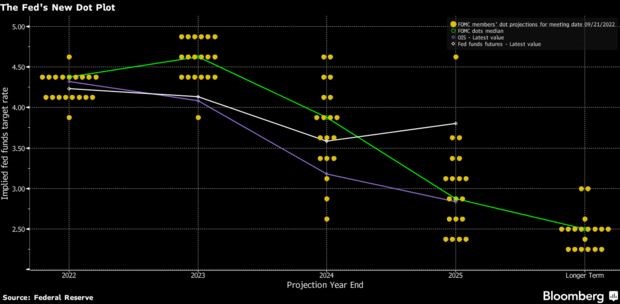

Dots higher than 4.5% for 2023 and Powell signaling recession might be the price to pay for crushing inflation were both badly interpreted by the markets.

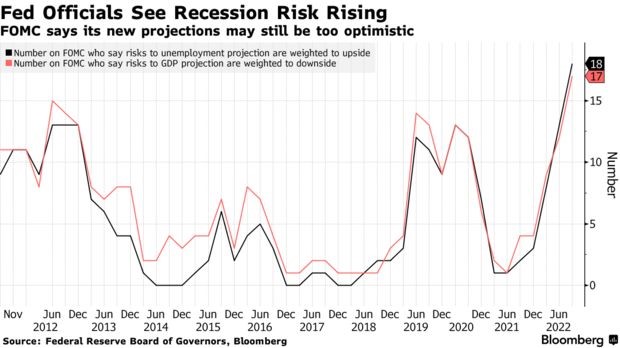

Yesterday’s sober assessment is in sharp contrast from six months ago, when Fed officials first started raising rates from near zero and pointed to the economy’s strength as a positive - something that would shield people from feeling the effects of a cooling economy. Via their more pessimistic unemployment projections, Fed officials implicitely acknowledge that demand will need to be curtailed at every level of the economy, as inflation has proved to be persistent and widespread.

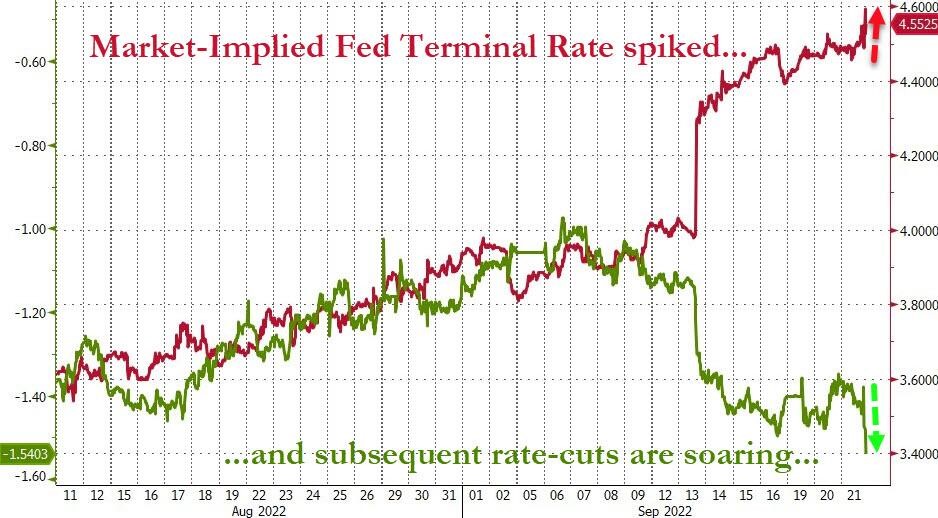

We believe that Mr Powell wants to make sure that markets take him more seriously than in July (his speech was seen as dovish and markets talked about a "Fed pivot"). He seems to be unhappy with markets pricing a rate cut next year – hence the need to push the market to re-assess the future direction of rates.

The Fed remains in a tightening mode with rates and inflation likely to stay higher for longer. The market has been complacent with the normalization of inflation and rates. Stagflation environment is characterized by inflation staying high despite the drop of output. Powell’s mission is to force the market to re-price this risk. They will hike until something breaks. In the meantime, real rates are expected to continue rising, which should weigh further on the valuation of risk assets. We keep our “unattractive” stance on equities and “cautious” stance on rates and credit spreads (see our August Asset Allocation insight “Not a time to be brave”).

{kind=link}

{kind=link}

{kind=link}

{kind=link}