We are sorry that for legal reasons we are not able to help US citizens or Canadian residents other than in Ontario, Quebec, or Alberta. Best wishes for the future…

Restricted access

We are sorry that for legal reasons we are not able to help US citizens or Canadian residents other than in Ontario, Quebec, or Alberta. Best wishes for the future…

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material.

This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor.

This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

Today, the European Central Bank held its monetary policy meeting. This session was highly anticipated in the current context of high uncertainties due to the situation in Ukraine, and already high and rising inflation even before the war started.

Here are three questions answered to help shed light on today’s ECB meeting.

The ECB did not alter its key interest rates today, with cash rates remaining in negative territory. But the central bank provided interesting indications on the path of its monetary policy for the coming months. The uncertainties caused by the war in Ukraine warrant cautiousness for the time being, but the ECB is setting the scene for being able to hike rates and tighten its monetary policy in the second half of the year if inflationary pressures persist.

Here are three questions answered to help shed light on today’s ECB meeting.

Do you think the decisions taken by the ECB were the right ones? Why?

The ECB is acknowledging the two main challenges that it will have to face in the coming months:

Continuously rising inflationary pressures that directly threaten its mandate,

Downside risks to growth resulting from the war in Ukraine.

Today’s announcements, namely accelerating the winding down of the Pandemic Emergency Purchase Programme and linking potential rate hikes to the evolution of the macroeconomic environment, are a way to create as much flexibility as possible for the ECB’s monetary policy in the months ahead.

With such flexibility, the ECB will be able to maintain very accommodative conditions if the impact of the war in Ukraine requires it, and to tighten financing conditions if made necessary by inflation developments. Forward guidance has to be scaled back in such an uncertain environment.

What consequences will this decision have on the economy?

In the short run, those decisions ensure that financing conditions remain extremely accommodative for the Euro area, thus continuing to support economic growth, especially in the current uncertain context.

Prospects of possibly higher short-term rates by the end of 2022 would not be overly negative for economic growth, as they would occur only if economic growth remains positive in Europe.

In such context, they would merely be an adjustment to an environment that would no longer warrant the kind of ultra-low interest rates implemented to fight deflationary pressures.

The consequences might be more visible on financial markets, where corporate bonds and even equities have benefitted from the lack of alternative caused by negative rates on cash and government bonds. Should cash and government bonds offer positive rates again, investors may reconsider the riskier portion of their portfolios and ask for higher premium on corporate bonds and equities.

How worried are you with inflation numbers?

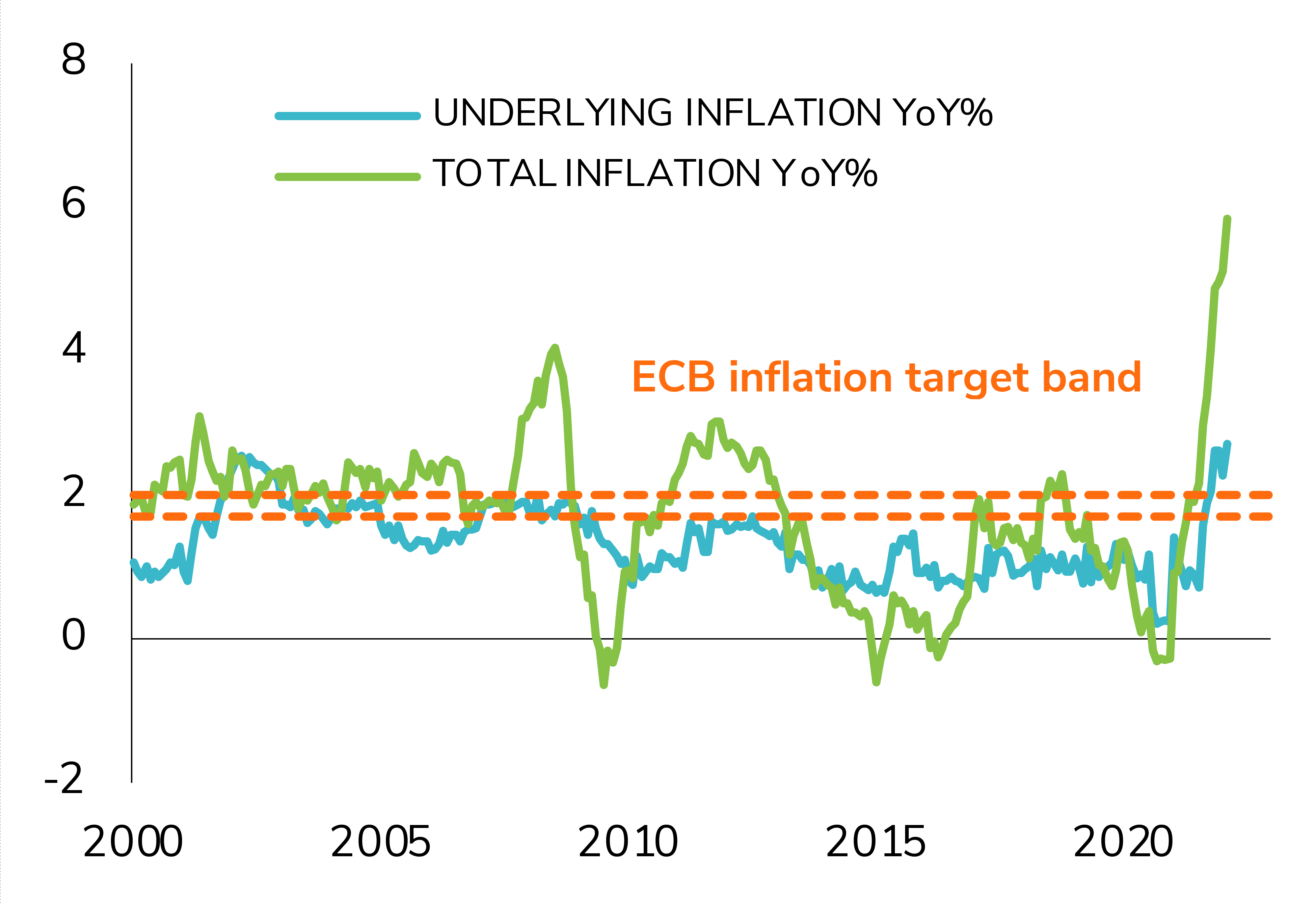

Inflation has been trending up in Europe due to higher energy prices, but also due to strong underlying demand. The “energy” component of inflation is obviously very sensitive to the developments in Ukraine and the ensuing sanctions against Russia, and will likely remain elevated in the months ahead.

Underlying and total inflation vs ECB Target

Source: Banque Syz, Factset

The underlying inflation, on the other hand, is driven by the strength in economic activity. At this stage, given the low level of unemployment across the Euro area, upward pressures on wages are becoming visible and could fuel an acceleration of this underlying inflation, which is one reason for the ECB to have the flexibility to be able to raise interest rates relatively rapidly if warranted. But an economic slowdown would probably tame the underlying inflationary trend and ease the pressure on the ECB to act.

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

.png)