.png)

CPI: broad-based moderation in underlying inflation

The June CPI report delivered broad relief after the energy-driven acceleration of previous months. Headline consumer prices fell 0.4% month-on-month, the largest decline since April 2020, reducing annual inflation from 4.2% to 3.5%. The reversal was driven mainly by energy: the energy index dropped 5.7% on a monthly basis, including a 9.7% fall in gasoline prices. Food prices nevertheless increased 0.2%.

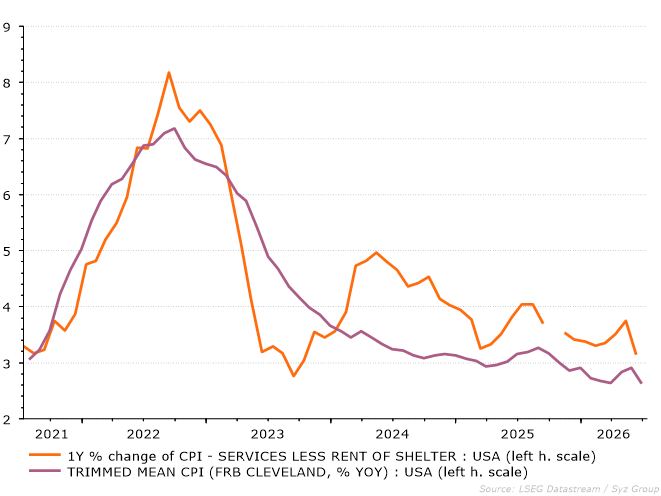

More importantly for the underlying trend, core CPI (excluding energy and food prices) was unchanged during the month and slowed from 2.9% to 2.6% year-on-year. The softness was broad-based. Motor-vehicle insurance declined 2.0% month-over-month, communication prices fell 1.5%, apparel dropped 0.6%, and medical care prices edged lower. Shelter inflation eased to 0.1%, its smallest monthly increase since January 2021, reinforcing the gradual disinflation visible in rents. Some volatility should not be overinterpreted: hotel prices were likely corrected after an earlier World Cup boost, while software prices remained firm.

Overall, June suggests that the spring inflation surge was beginning to fade rather than becoming entrenched. The details point to a moderate June core PCE reading. However, renewed oil-price pressure in July and inflation readings that remain largely above the Fed's 2% year-on-year target mean the Fed will want further evidence before declaring the inflation shock transitory.

Energy prices recorded a strong drop in June, but also core measures trended lower

Source: LSEG, Syz Bank

Source: LSEG, Syz Bank

Underlying inflation – new Chair Warsh’s favoured measure – is abating again

Source: LSEG, Syz Bank

PPI: pipeline pressures ease, but remain elevated

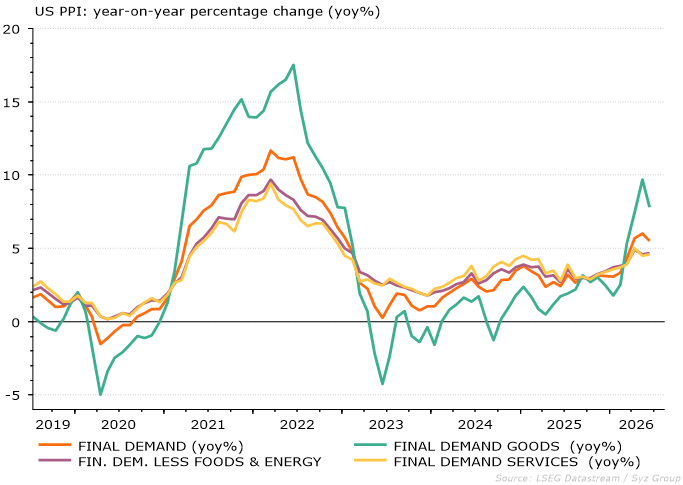

Producer-price data reinforced the CPI’s reassuring message. Headline PPI fell 0.3% month-on-month in June, below expectations, after increasing 0.6% in May. The decline was concentrated in final-demand goods, which dropped 1.4%. Energy prices fell 6.4%, led by a 12.0% decrease in gasoline, while food prices declined 0.6%. By contrast, final-demand services rose 0.2%, reflecting higher trade margins.

Underlying pipeline pressures also moderated. PPI excluding food and energy increased 0.2% month-over-month, while the measure excluding food, energy, and trade services rose by just 0.1%; both came in below expectations. Nevertheless, annual producer inflation remained elevated, with headline PPI standing at 5.5% year-on-year, and the latter core measure at 5.1%. Some intermediate-price measures remain firm, showing that pipeline pressure has eased, not disappeared.

Together with the CPI details, the release points to core PCE inflation of below 0.2% in June (month-on-month) and a small decline in headline PCE. This would support a wait-and-see Fed stance, although policymakers must monitor whether cost shocks will reach through to consumers.

PPI figures for June mostly reconfirmed the CPIs message, but core demand goods and services still to be monitored

Warsh: preventing isolated price shocks from spreading

In his congressional testimony, Fed Chair Kevin Warsh acknowledged the softer CPI report but cautioned that it was only “one data point” and should not be cherry-picked. He reiterated that the FOMC has “no tolerance for persistently elevated inflation” and gave no indication that a policy move was imminent. Warsh’s main point was that policy cannot prevent every tariff- or oil-related price increase. Instead, the Fed must ensure that temporary changes in individual prices do not spread across the economy or become a generalised rise in the price level. This supports patience after June’s encouraging data, but not complacency. The July meeting is therefore likely to feature a discussion of tightening, even if rates remain unchanged, which is currently our base case. Warsh also argued that the size and duration of the Fed’s balance sheet deserve review. Outside crises, he believes monetary policy should be conducted primarily through interest rates.

An important next step to lower inflation but more colling is needed to keep the Fed in its “wait and see” position

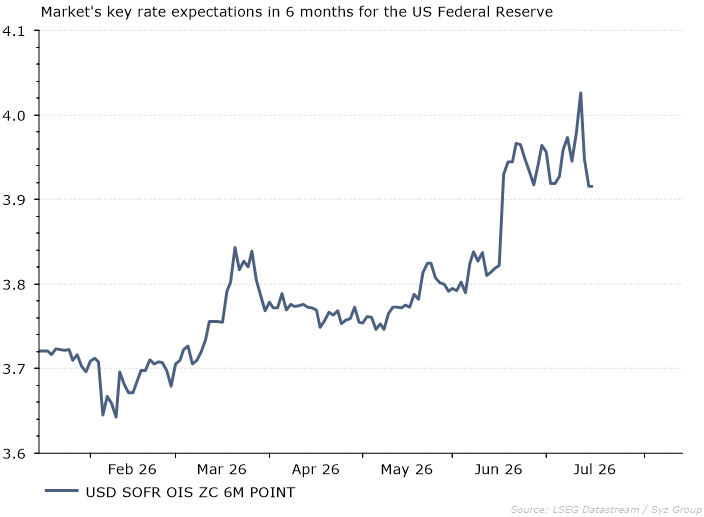

The CPI and PPI releases came in significantly below expectations, prompting markets to scale back the probability of further Fed rate hikes. This brings market pricing closer to our view that inflationary pressures will gradually ease and that the Fed will keep interest rates unchanged until year-end.

Nevertheless, Kevin Warsh’s comments remained cautious and firm on inflation. While the FOMC can afford to remain patient for now, policymakers will need further evidence that US inflation is cooling sustainably. Without such confirmation, our call for no rate hikes through year-end could quickly come under further pressure.

The renewed escalation of tensions in the Middle East and the possibility of stronger US demand are important upside risks to inflation and, hence, to our Fed call. We will continue to monitor both developments closely.

Key rate hike expectation for the next 6 months dropped significantly with the June CPI and PPI prints