.png)

Executive summary

While inflation seems to have peaked in the US, central banks need to keep tightening for a while in order to bring it closer to their long-term target. This would probably imply a recession, with a negative impact on earnings growth. Equity valuations are more attractive than at the start of the year but they are not cheap enough to trump negative earnings revisions. While market factors (coincidental indicators) have turned positive, our leading indicators

(macro, liquidity, earnings, valuations) are still not supportive enough to change our cautious stance on equity markets. We maintain our preference for credit (positive) and also keep a cautious stance on rates. We remain positive on the dollar against all currencies but upgrade the euro from unattractive to cautious on the back of a more hawkish ECB and lower risk of a deep recession in the eurozone.

The big picture

This week was an important one for monetary policy with major central banks (Fed, BoE, ECB, SNB, etc.) reporting their last decision of the year. The tone remains hawkish, as central bankers hiked rates by another 50 basis points while reiterating their intent to keep tightening until inflation comes closer to their long-term target.

High inflation and rising rates are weighting on global growth, with Europe being the most at risk of an energy crisis. China reopening is hampered by Covid and geopolitical tensions. As such, global growth is expected to slow down significantly in 2023 with some negative consequences on earnings growth.

There are some silver linings though. First, central banks may no longer have to be as aggressive as in 2022. Second, fiscal intervention tries to cushion the blow from rising energy prices. Last but not least, markets historically trough before earnings cycle turn around.

Still, the fact that central banks will continue to tighten in the upcoming months despite an economic and earnings recession means that equity volatility is likely to stay high. Finally, valuations are cheaper than they were at the start of 2022, but they are still not cheap enough.

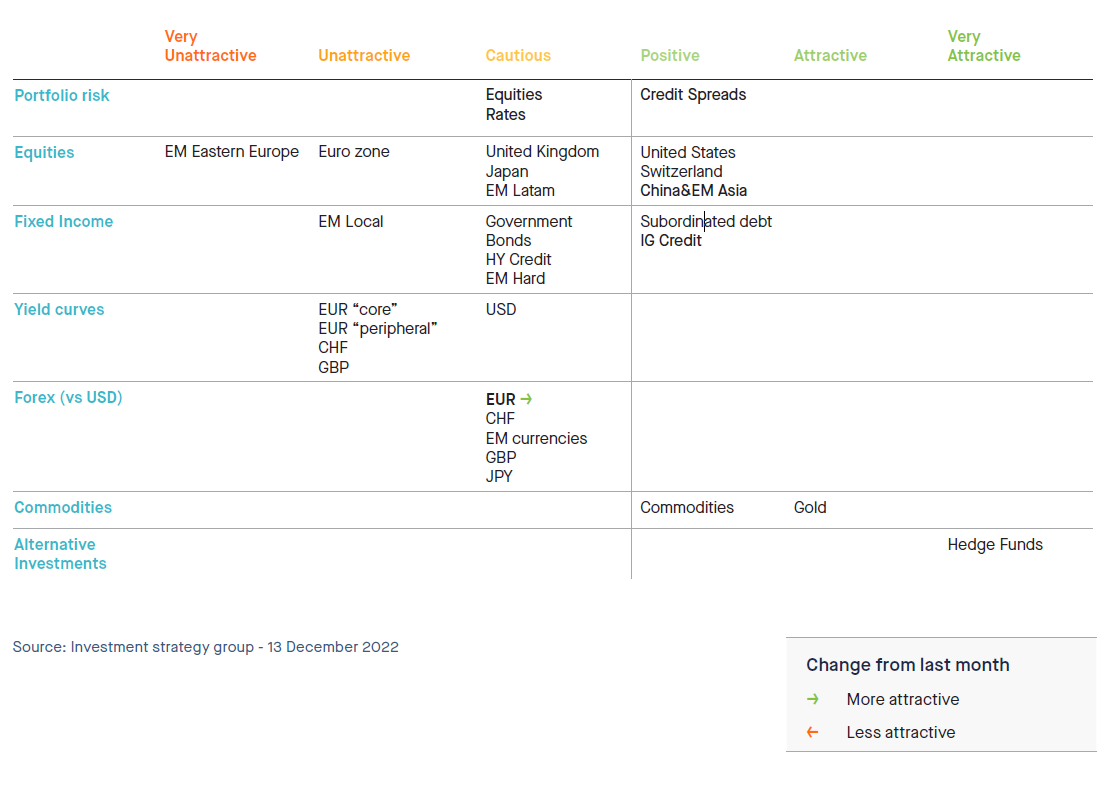

Our 1-month view: we keep a cautious view on global equities

- Based on the weight of the evidence (i.e. the aggregation of our fundamental and market indicators –see next section), we are keeping our cautious view on equity markets.

- From a regional standpoint, we maintain a “positive” stance on US equities. We are cautious on UK, Japan, and EM Latam. We are positive on EM Asia equities.

- We keep an “unattractive” stance on Eurozone equities. Our least favored market remains EM Eastern Europe equities (very unattractive).

- Within Fixed Income, we have kept a “cautious” stance on rates while being positive on credit. The double effect of spreads widening and rising yields have considerably improved the risk-reward of short to mid-duration credit portfolios – including Investment Grade.

- We keep a positive view on Commodities (with a “preference” stance on Gold) as well as a very attractive view on hedge funds.

- In Forex, we are positive on the dollar against all currencies. We are upgrading the euro from “unattractive” to “cautious” as deep recession risks in the eurozone have decreased recently.

Indicator #1

Macro-economic cycle: Negative

Global economic growth continues to slow down as we prepare to enter 2023. However, we note that economic surprises are no longer negative in key economic areas, as the consensus already expects a significant economic slowdown.

European economies (UK included) are hit by the energy crisis and the global growth slowdown. The energy-driven surge in inflation and the prospect of energy supply cuts or restrictions through the winter already heavily weigh on consumer and business sentiment, as well as on spending and investment. However, the recession could prove to be milder than feared. Winter weather is the wild card. Switzerland stands out for the moment but will not be spared by Europe’s woes.

Meanwhile, the US economy continues to show signs of resilience, led by consumption spending in services. Higher rates and tighter credit conditions are headwinds for growth in 2023. Investment keeps growing overall, even if some sectors are already losing steam (e.g Residential Real Estate is slowing).

China is struggling with Covid resurgences and turbulences on the real estate market. Authorities aim to stabilize economic growth in 2023 (but not more than that).

Slowing global growth and a rising US dollar weigh on most Emerging Market economies’ growth prospects, even if some (Brazil, India, commodity exporters) show signs of resilience.

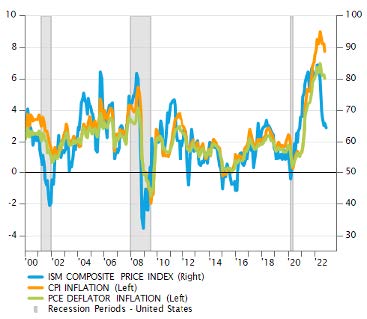

With regards to inflation, pressures remain across all developed economies, even if the underlying sources may be different.

The increase in prices hits double-digit figures in Europe due to the energy crisis. Peak inflation is (probably) behind in the US while in Europe, inflation is dependent on the evolution of energy prices. Inflation surprises are still generally positive, but much less than earlier in the year both for Europe and the US. This supports the “Peak inflation” view.

Going forward, we expect inflation to stay above central bank’s target in the US and Europe but to come down materially from peak level. The question is how fast. Wage dynamics remain in the US and Europe and central banks need to see some inflexion here to be able to consider a “pivot”. Asia is facing a milder inflation environment.

Overall, medium-term expectations are declining on global growth slowdown and determined central banks. Nevertheless, we still view the mix of declining growth and still elevated inflation as being negative for risk assets.

Inflation – Likely to have peaked, slowdown ahead in 2023. The question is: how fast?

Source: Banque Syz, FactSet

Source: Banque Syz, FactSet

Indicator #2

Liquidity: Negative

Central banks remain firmly on the path of rate hiking. To regain control on inflation, and preserve its credibility, the Fed has no choice but to tighten monetary policy until there are clear and tangible signs of a reversal in inflation dynamics. During the December FOMC meeting, Mr Powell reiterated the Fed’s hawkish stance. The US Federal Reserve hiked rates by 50 basis points for the last meeting of the year, as it was widely expected. They increased key rate to 4.5%, the highest since 2007. Projected rates would end next year at 5.1% (+50bps beyond prior median of 4.6%), according to the Fed median forecast, before being cut to 4.1% in 2024 - higher level than previously indicated (see FOMC dots below). Prior to the decision, markets were expecting rates would reach ~4.8% in May.

If there is to be a pivot, it could rather be in Europe, given the looming recession. Indeed, a recession (and corresponding fall in domestic demand) would dampen underlying inflationary trends. It seems imminent in Europe, not yet in the United States, although the magnitude and the length of a recession will be key for the rate outlook in Europe. Still, for the moment, the ECB has no other choice but to hike. Indeed, wage dynamics are also on the rise in Europe, indirectly supported by fiscal intervention. And monetary policy normalization has barely started yet as the ECB is behind the curve. This stance was confirmed by Mrs Lagarde during the ECB’s December meeting, as she signaled more rate hikes ahead and the beginning of Quantitative Tightening in 2023.

Central banks are, at the same time, fighting existing inflationary trends and trying to offset the impact of fiscal interventions. Monetary policy is getting tighter across all economies, with higher rates and withdrawn liquidity. As seen in the UK during this autumn, the more the government intends to support its economy with fiscal spending, the more the central bank has to hike rates to offset inflationary pressures.

Overall, the liquidity environment remains negative for risk assets as most developed markets are facing more rate hikes, quantitative tightening, and global liquidity reduction.

Fed dots (December meeting)Source: Bloomberg

Source: Bloomberg

Indicator #3

Earnings growth: Negative (downgraded from Neutral)

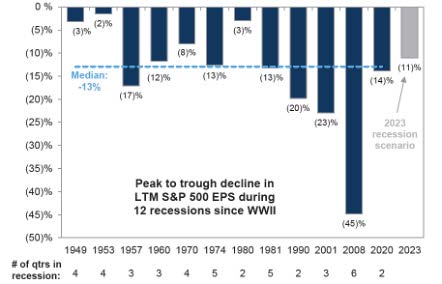

The blended MSCI USA earnings growth rate is +6.1% for 2022e and 4.7% for 2023e. We believe that expectations for next year are too optimistic as companies might face negative operative leverage: they will not be able to pass on more costs to the customers (lower nominal sales growth) while they will have to absorb higher wage and input costs. Historically, EPS have declined meaningfully during recessions (see chart below).

In Europe, there is still some room for downward revisions as well (despite favorable forex effect). Indeed, after a 18.4% earnings growth expected in 2022e, MSCI Europe earnings are expected to grow by 2.4% in 2023e. This also looks too optimistic in light of recent PMI data and based on the recessionary prospects for the European economy next year. While earnings growth has been a tailwind for equity markets in 2022, we believe that this will no longer be the case in 2023. As such, we are downgrading our stance on the earnings growth indicator from positive to negative.

Historical EPS declines in the US

Source: Goldman Sachs

Indicator #4

Valuations: Neutral

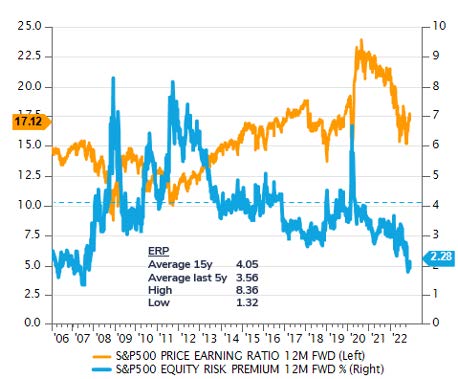

Global equity valuations have de-rated this year. In the US, the S&P500 multiple has de-rated by the same magnitude as seen in previous recessions. On a relative basis, Equity Risk Premium is a headwind now, as it has probably reached a bottom. We note that cash and bond yields are now competing with equities. In Europe, absolute and relative valuations are cheaper than in the US but for a reason (energy crisis and higher recession risk). Overall, this indicator remains NEUTRAL. Equity markets are less expensive than last year, but they are not cheap either.

Valuations are no longer expensive in absolute terms, but not cheap yet either

Source: Bank Syz

Indicator #5

Market Dynamics: Positive

Our market dynamic indicators are in deep positive territory – and this applies to both our US and European proprietary models. While the key equity benchmarks remain below their 200-day (falling) moving average, the trend indicator is positive as price is above the 100-day and 50-day moving average. Other indicators are in positive territory as well. An interesting signal is the gradual improvement of market participation (breadth); indeed, while tech mega-caps have been hit during the earnings season, small & mid-caps have been doing reasonably well, hence the positive signal for this indicator. We also note that this rally didn’t give overbought signals (RSI), which is another positive.

Asset Class Preferences

Equity allocation

Cautious

Risk assets are facing several headwinds; high inflation and rising rates which are weighing on global growth (with Europe already into an energy crisis), China reopening hampered by Covid and geopolitical tensions and high political uncertainty (US divided government, shockwaves in Europe from the war in Ukraine and sanctions on Russia). Meanwhile, fiscal intervention tries to cushion the blow from rising energy prices but given the high level of indebtedness of most developed countries, it seems that the market is less willing to finance fiscal deficits than in the past.

However, there are several short-term tailwinds for the market. Seasonality and the US 4-year presidential cycle are both becoming positive for the rest of the year. Sentiment is still too pessimistic (which is a positive from a contrarian point of view) and share buybacks are providing much needed support to equity markets.

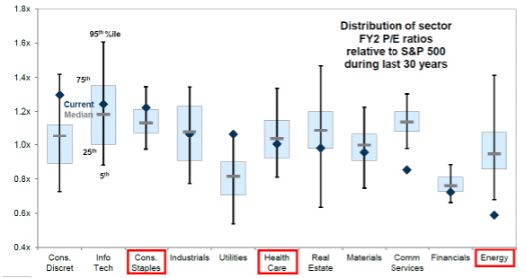

Meanwhile, earnings growth is now becoming a headwind for equity markets and valuations are not cheap enough. Overall, the weight of the evidence leads us to keep our “cautious” stance on equities. From a regional point of view, we are positive on the US, Switzerland, and China & EM Asia. We are keeping a cautious stance on the UK, Japan and EM Latam. We have an unattractive view on European equities as recession and the rebound of the euro will weigh at some point on 2023e European earnings growth expectations. In terms of sectors, we remain overweight in Energy and Healthcare and our underweight in Utilities and Real Estate. We are upgrading Consumer Staples from neutral to overweight. Finally, we are neutral on Information Technology.

Sector valuations

Source: Factset

Fixed income allocation

Cautious on Rates, Positive on Credit

We are keeping a “cautious” stance on rates. Recession fears weigh on rates. Long term rates have dropped significantly, driving the U.S. yield curve to the deepest inverted level ever recorded. German 10-year government bond yields are back to around 2%, following the movement of US yields. The spread between U.S. and German 5-year yields bottomed out in June, justifying the movement in the EURUSD currency. We continue to favor the front end as it offers a decent carry and low rate sensitivity, while the historical level of yield curve inversion argues for staying away from the long end. Within government bonds, we do have a preference for USD over EUR as ECB needs to catch-up vs. Fed. Peripheral yields should benefit from the ECB's new tool (IPT) and Italian yields have shown resilience after the Italian election results. The QT program should run smoothly and not affect peripheral yields too much.

We are positive on credit. We have seen some retracement in spreads already but yields in USD are still attractive. European Investment Grade spreads are back below 200bps but still trading with a premium vs. US peers. We favor Investment Grade short term bonds while the intermediate segment is becoming attractive due to the steepness of the credit spread curve. US High Yield credit spreads are now back below 500bps.

Our view on emerging market bonds remains unchanged ("cautious" stance) but is gradually improving as it strengthens on the back of solid earnings, good central bank performance, a weakening U.S. dollar, and the potential reopening of the Chinese economy. In addition, relative to other high-beta segments (i.e., U.S. high yield), emerging market bonds in hard currency look attractive.

In local currency terms, emerging market debt should not be far from attractive levels, especially if we have reached peak inflation in these countries. Emerging market central banks tightened monetary policy very quickly when inflation started to rise. Their aggressive strategy is starting to pay off (inflation in Brazil).

Commodities

Positive overall. Keeping a preference stance on Gold

Over the last few months, commodities have moved from being overbought to oversold as recession fears now dominate all markets. We remain positive on the asset class and sees commodities as an attractive macro hedge. After years of capex underinvestment, many commodities are facing a supply shortage while demand is firm. The invasion of Ukraine by Russia and the sanctions are worsening the situation. Energy and commodities are needed for virtually everything, and Russia exports both massively. And unlike in 1973, it’s not just the price of oil, but the price of everything that is surging. Furthermore, the supply shock might be a long lasting one. Indeed, despite ongoing negotiations between Russia and Ukraine, a stalemate with prolonged economic impacts looks likely. We are thus positive on broad commodities. We are keeping our preference stance on Gold. Rising USD real rates continue to weigh on Gold prospects, but it can remain a potential inflation hedge and a safe haven in a highly uncertain environment.

Hedge Funds

Very attractive

Alternative strategies grab their chance to deliver value. After the pandemic, economies are adapting to the changing cost of capital. Investors need a more selective and active approach to investing. As interest rates rise, hedge funds are providing positive returns. Alternative strategies are benefiting from lower liquidity and higher interest rates.

In terms of hedge fund strategies, we are positive on equity hedge with low net exposure and a trading approach. We are also positive on macro and CTA.

Forex

Becoming less negative on the EUR even if the US dollar remains supported by yield differentials

Peak inflation, relatively resilient economic growth and the prospect of a less aggressive Fed give room to the EUR for some upside, even if the consequences of the energy crisis and the ECB’s actions remain a potential sword of Damocles hanging above the European currency. We are upgrading the outlook on the euro from “unattractive” to “cautious”.

The Swiss franc is temporarily overwhelmed by the dollar’s strength, but the downside is nevertheless limited due to real rate differential and sound fundamentals. Fundamental drivers plead for a firm Swiss franc over the medium term. Flight to safety from European assets is a powerful support. But faster Fed rate hikes than the SNB are supporting the USD in the short-run.

The sterling faces continuing downside risk as inflation surges and fiscal policy gets wild. The surge in energy prices and concerns around winter supply weighs on GBP prospects from several angles: macroeconomic growth prospects, inflation, interest rate differentials, external balance, flow of funds. The BoE has relaxed somewhat its stance with the return of fiscal “orthodoxy” of the Sunak government

With regards to the yen, there is limited additional downside based on fundamentals, but the yen remains under pressure as long as the BoJ does not move. For now, the BoJ still does not move but hopes of a less aggressive Fed have spurred a rebound of the JPY.

Cross-asset correlations and volatility

Monetary policy expectations are the main driver of bonds and equities at the moment, and correlations are positive and elevated among asset classes. The bond/equity correlation is in positive territory, implying no diversification in multi-asset portfolios. Volatility has turned lower on the equity and bond side recently. Volatility remains high on the fixed income side.