.png)

Indicators review summary

Indicator #1

MACRO ECONOMIC CYCLE: Positive (unchanged)

Global growth remains firmly positive even if the «Covid recovery effect» gradually fades away. The expansion in manufacturing and service sectors is broad-based, even if the momentum is softer compared to H1 2021. A positive development over the last few weeks stems from the fact that economic surprises are no longer deteriorating and are even turning positive in the US and the UK (see chart below). On the more worrying side, China growth has slowed down in 2021 on the back of the normalization in credit conditions and supply constraints. In the near-term, we do not see any appetite on behalf of Chinese authorities to accelerate the credit impulse. As such, weak growth momentum is likely to persist in the months ahead – at least until March 2022. The sub- par growth outlook in China is somewhat offset by strong growth momentum in the US. After a “soft patch” in the 3rd quarter, real GDP growth is re-accelerating meaningfully. While price and wage inflation are at a decade high, we believe that we have reached peak bottleneck and this should soon lead to peak inflation. Indeed, our view remains that higher Developed Markets inflation in 2021 is mostly due to transitory factors. While inflation is likely to stay high in the medium-term, we expect it will progressively converge towards central banks’ target throughout 2022.

Indicator #2

LIQUIDITY: Neutral (unchanged)

Monetary and fiscal stimulus have been identified as major drivers of the ongoing global economic recovery. On the monetary policy side, we note that G3 central bank balance sheets continue to expand but at a much slower pace than 12 months ago. Global talks of monetary policy normalization, asset purchase tapering and rate hikes have started in many economies. However, we note that Central Banks are going in different directions on interest rates. In many countries, consumer prices are rising significantly. Central banks would have the ability to counteract this via monetary policy means - by raising interest rates, thereby restricting access to credit and slowing down value creation. The rate hike cycle has already started in emerging markets and some developed markets central banks are now tempted to follow. But not all central banks are of the opinion that timely countermeasures are necessary. Given the high level of leverage in the system (economies and markets), we believe that cautiousness is warranted as higher real rates would put the economic recovery at risk. The fact that of positive inflation data surprises may have been reached in developed markets (see chart below) might give G3 central banks some respite. While China maintains its current restrictive monetary policy stance for the moment, most of the large economies still benefit from ultra- loose conditions. On the fiscal side, the impact of fiscal policy on GDP is turning negative especially in developed countries. The US, for instance, will face a fiscal cliff in 2022.

Indicator #3

EARNINGS GROWTH: Positive (unchanged)

Earnings season in the third quarter was rather strong although less impressive than in the second quarter due to less favorable comparison effect. In the US, more than 80% of companies beat estimates but the market was a bit more condescending – companies who beat estimates posted modest returns while those who missed were more severely punished than in previous quarters. Going forward, we expect earnings growth to normalize with momentum staying positive and acting as a tailwind for equity markets.

Indicator #4

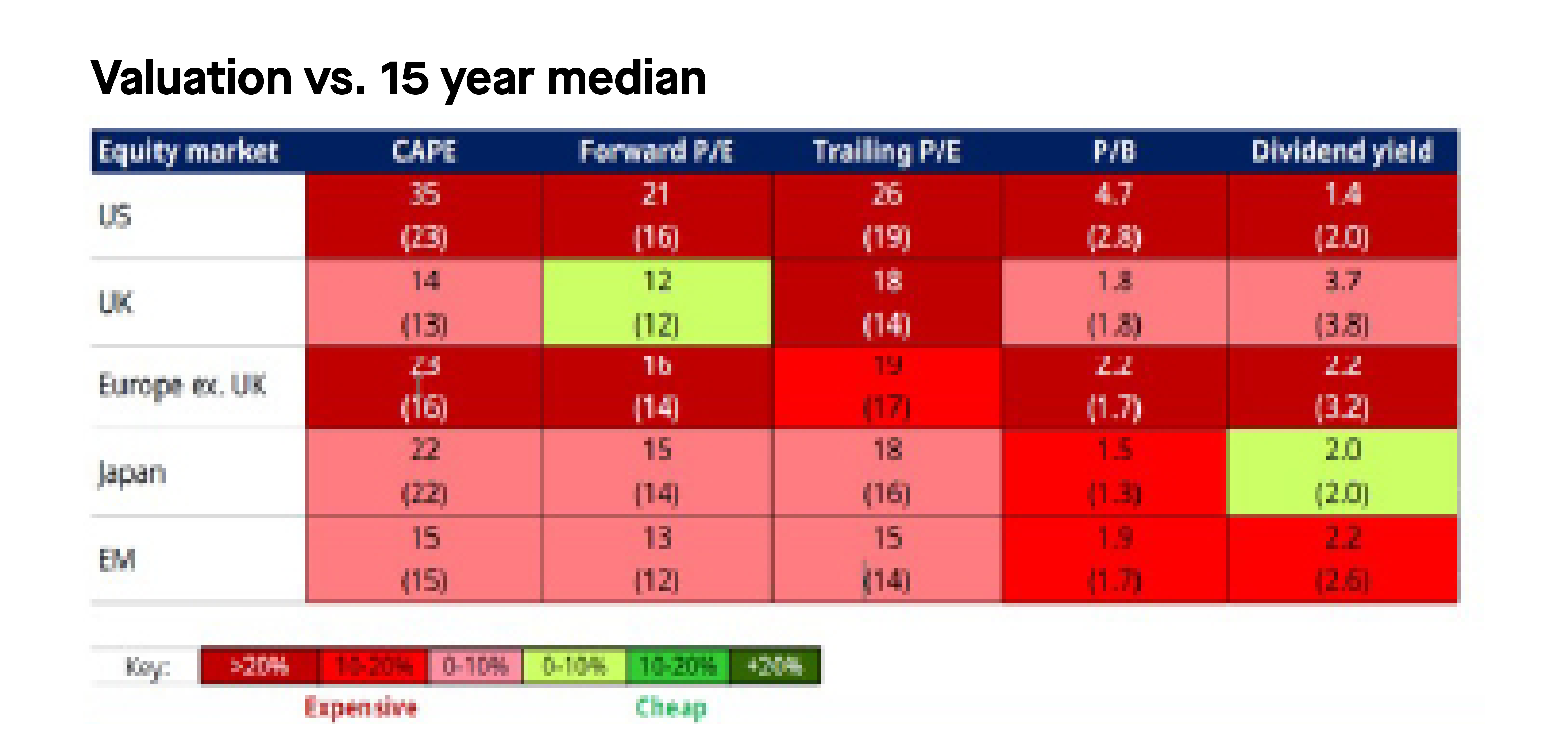

VALUATIONS: Neutral (unchanged)

From an absolute valuations (P/E), US equity valuations have become slightly less attractive over the last few weeks. On a relative basis (compared to bonds), we haven’t seen much improvement as government bond yields have been rising. That said, equity valuations relative to bonds remain attractive. The picture is similar in Europe, the UK and Japan.

Indicator #5

MARKET TECHNICALS: Neutral (unchanged)

Technical indicators are stretched after this year strong rally. We note that high frequency signals (volume and technical indicators such as RSI and MACD) are sharply overbought and thus plead for a pause in the bull market. However, both trend and market breadth indicators remain positive and thus signal a continuation of the S&P 500 advance. Sentiment indicators offer a mixed picture. However, the put/call ratio is the only one showing signs of “irrational exuberance”. The VIX and Bull/bear ratio do not show signs of extreme complacency at this stage. On an aggregated basis, our technical indicators are thus neutral.

Asset class preferences

EQUITY ALLOCATION: Positive

For the coming month, we are maintaining a positive bias toward equity allocation. In the current environment of positive economic growth and low interest rates, equities remain clearly the most attractive asset class. Still, the risk of a correction is increasing with central banks becoming less dovish, downside risks to the economic growth outlook and earnings expectations that have been significantly raised. We believe that our agile tactical asset allocation process will help us navigate through a more volatile and uncertain market environment.

From a sector standpoint, we continue to maintain a long-term preference for secular growth story. But in the short-term, some tactical allocation to cyclical themes (e.g energy and financials) is warranted given the strong reacceleration of GDP growth in the U.S. From a regional point of view, we continue to maintain a preference for Eurozone equities (strong earnings growth and valuations in-line with historical average) and US equities (expensive valuations but superior RoE). We are upgrading Japan from “Positive” to “Preference” on the basis of 1) Strong operational leverage (high sensitivity to growth); 2) Weakening yen; 3) Improving macroeconomic growth and; 4) New political leadership. We are also upgrading UK equities from “Cautious to “Positive” as macro- economic surprises are turning positive while valuations are compelling. Meanwhile, we are downgrading China equities from “Positive to “Cautious” as we believe that slowing growth and regulatory crackdown will continue to weigh on sentiment.

Fixed income allocation: Still cautious on duration, yield curve and spreads

We remain cautious on government bonds on the back of rising inflationary pressure (at least in the short-term) and monetary policy normalization. We note however that the short-end of the curve is becoming more attractive after recent bear flattening moves in the US and core Eurozone. From a regional perspective, we still have a preference for EUR Core curve over USD Curve due to lower growth in the Eurozone, more support from ECB and unfavorable technical in US (although it has been softening recently). We remain cautious on the whole credit spectrum due to valuation (very tight spreads). We would consider a sell-off in US High Yield as a buying opportunity. We remain positive on subordinated debt. The segment looks mature and resilient and continue to offer some premiums while the current environment is still favorable to banks.. We remain positive on Emerging Markets debt as the sell-off is offering more attractive valuation. We continue to like Asian High Yield as opportunities abound during the current sell-off.

COMMODITIES: Still cautious and keep exposure to Gold

We remain cautious on commodities. While the asset class is enjoying its best year since the oil crash in 1973, we believe the recent bull run is overbought and being be somewhat driven by panic rather than pure fundamentals. We start to see some commodities segments (e.g industrial segments) being impacted by lower growth prospects in China. We keep an exposure to Gold. The upside of the yellow metal still depends on how much lower US real rates can go. But it was encouraging to finally see some firming recently as investors are looking for some diversifiers in their multi-asset portfolios.

FOREX: Bullish dollar

Real rates and macroeconomic momentum continue to weight on the EUR/USD dynamics. Fundamental drivers still plead for a firm CHF over the medium term but the USD benefits from the current environment. UK stagflation risk weights on GBP short term prospects.

Tactical positioning: our asset allocation matrix