.png)

In a nutshell:

- The macroeconomic landscape of still very elevated inflation projections and declining growth is weighing on risk assets. Markets trade as if recession is imminent. While the US might indeed face a technical recession in the first half of the year, economic indicators and several shock absorbers lead us to think that Uncle Sam can still avoid a full-blown recession. The landscape is different in Europe and will be dependent on Russian gas imports as we exit the summer.

- Liquidity / monetary conditions remain negative as well. For central banks, there is a real risk for inflation to remain high even if growth slows down, forcing them to remain in a tightening mode. Earnings growth has been a tailwind for markets through the first semester but current earnings growth expectations do not reflect the global economic slowdown. We believe that the risk of earnings downgrade is not yet priced in. Valuations were further de-rated but are still not cheap enough.

- Our coincident indicators (market dynamics) are currently positive but can swiftly turn negative, as market instability is high. Trend indicators and market breadth give negative signals while sentiment is oversold but not to the point of triggering a contrarian call.

- Overall, the weight of the evidence (i.e. the aggregation of our fundamental and market indicators) remains negative. As such, we maintain an “unattractive” view on equity markets in general. We do a have a positive stance on US, Swiss and China / EM Asia equities. Our least favored markets remains the Eurozone and EM Eastern Europe equities (very unattractive). We maintain a cautious view on the UK, Japan and EM LatAm.

- In Fixed Income, we are upgrading rates from "unattractive" to "cautious" in order to reflect the deteriorating global growth outlook. We keep a "cautious" stance on credit spreads.

- In Forex, we are positive on the dollar against all currencies. We are downgrading the euro one notch further from "cautious" to "unattractive" as the Eurozone is facing a major energy crisis, which is deteriorating the fundamentals of the common currency.

- We keep a positive view on Commodities (with a "preference" stance on Gold) as well as a very attractive view on hedge funds.

Indicators review summary

Indicator #1

Macro-economic cycle: Negative

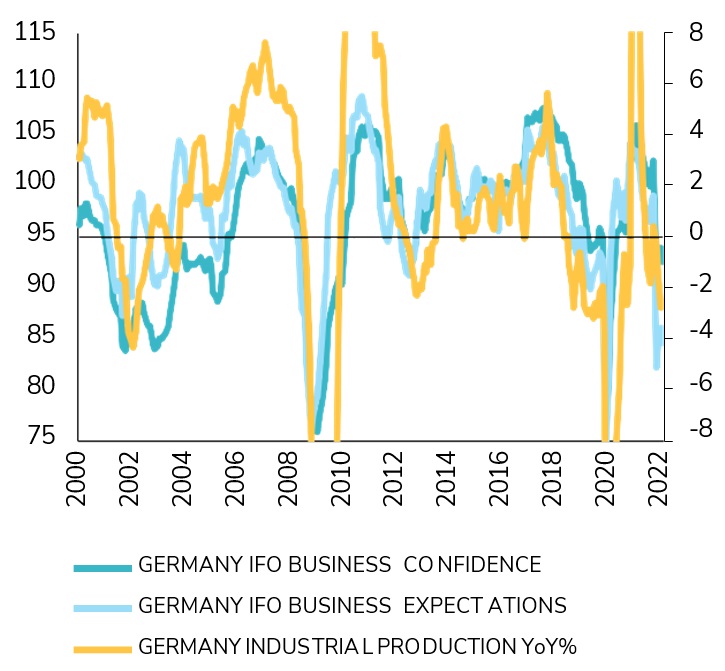

Economic activity has been slowing more than expected in developed economies. Real-time estimates of GDP growth are now negative in the US for the second quarter. Real consumption hampered by rising inflation. Higher interest rates are weighing on interest-rate sensitive sectors such as real estate. Households and business sentiment is severely affected by the consequences of surging inflation, resulting in lower purchasing power and declining margins. Energy and commodity scarcity is an increasingly important factor of uncertainty.

Full employment and fiscal intervention support domestic consumption in developed markets. Employment is strong across Europe and the US, with unemployment rates around so-called «full employment». European governments, and even some US states, are taking various steps to contain the impact of rising energy prices on households’ purchasing power. Tight job markets are driving ongoing upward pressures on wages. Government subsidies are fueling inflationary dynamics, in direct opposition to central banks’ actions of tightening monetary policies to curb inflation.

Employment dynamics, which are usually lagging indicators of activity, will therefore also be a key determinant of the H2 economic growth outlook.

The energy crisis has overtaken rate hike fears in Europe. The main risk for Europe is not monetary policy tightening, it is the growing scarcity of essential oil and gas. Germany is the weakest link when it comes to the negative impact of short supplies and high prices of energy, but Italy and the entire Euro area are exposed. Asia is currently going through a different dynamic than the Western world. Economic activity in China is rebounding as Covid-related restrictions are being lifted. Inflation is lower and therefore doesn’t impact consumer spending as negatively as in the Western world. Currency depreciation is supporting exports. Asia would not be insulated from a recession in the US or Europe, but the comparatively better domestic dynamic can remain supportive for the months ahead.

Inflation is at risk of remaining high even if growth slows down. Inflation rates keep climbing to new multi-decade highs across developed economies. Upward price pressures are coming from the entire goods & services spectrum.

Commodity and energy prices are not the only culprits (even if big contributors). The succession of supply and demand shocks since 2020 has broken the «low inflation equilibrium» of the past 25 years. Higher inflation is feeding into households and business expectations, creating «second round effects» and a dynamic of rising wages in the US and Europe. Inflation may finally peak in H2 (if anything, due to base effects), but it will remain elevated in the months ahead and may prove to be stickier than expected.

Overall, we believe that the macroeconomic landscape of still very elevated inflation perspective and declining growth is NEGATIVE for risk assets.

Source: Banque Syz, FactSet

Indicator #2

Liquidity: Negative (downgrade)

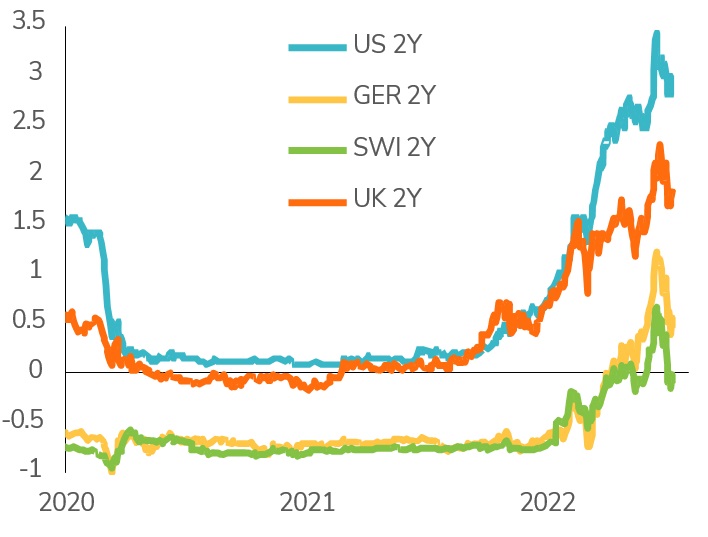

The current environment is a difficult one for central banks, especially the ECB. Exiting Quantitative Easing and zero or negative rate policies was never going to be easy, but could it have been worse? The Fed is still a long way from “neutral” but has already moved away from its “crisis policies”. Most Developed Markets central banks (including the SNB) and even several EM central banks have also started to adjust.

For them, the trade-off between inflation and growth may shift in H2 toward a less hawkish stance. Meanwhile, the ECB is in an extremely uncomfortable position. The European central bank is facing high and running inflation fueled by a combination of rising energy prices, rising

wages and a depreciating euro, which means the must deal with significant downside risks on growth. Last but not least, risks of resurgence in sovereign spread tensions are looming.

Overall, global liquidity is no longer growing, which is a NEGATIVE for risk assets.

Indicator #3

Earnings growth: Neutral

To the surprise of many, analysts have been revising earnings upwards for 2022E throughout the first half of 2022. Consensus expects MSCI World earnings to grow 11.5% in 2022e and 7.6% in 2023e which seem too optimistic – in our opinion. While top-down analysts are now starting to downgrade earnings estimates bottom-up analysts have only mildly downgraded their forecasts. We thus believe that the risk of downgrades in earnings not priced yet. On the positive side, we note that corporate margins currently stand at a record high, which means that companies have so far been able to pass input cost increases onto consumers. Balance sheets remain solid as well and companies have room for more share buybacks. As such, we continue to see earnings growth as being a mild tailwind for equities but still believe that some downward earnings growth revisions could happen later this year.

Indicator #4

Valuations: Neutral

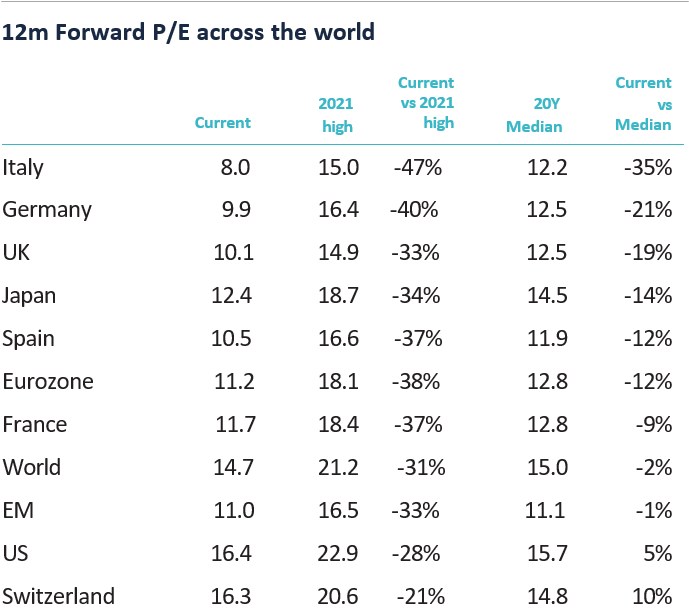

Global equity valuations were further de-rated. With the exception of the US and Switzerland, 12-month forward P/Es are all below the 20 year median. Indeed, the current equity market drawdown has been driven by valuation multiples compression rather than earnings revision.

On a relative basis, we note that the S&P 500 equity risk premium is roughly in-line with the last 5-year average but is more expensive than the 15 year average. While P/Es have declined, the equity risk premium is not attractive enough due to the rise in bond yields. European markets’ relative valuations have been improving but are likely becoming cheap for a reason. Valuations are improving in the UK and, to a lesser extent, in Switzerland.

Overall, this indicator remains NEUTRAL.

Source: IBES

Indicator #5

Market Dynamics : Positive (upgrade)

Our coincident indicators (market dynamics) are currently positive but they can quickly turn negative, as market instability is high. The low frequency / long-term indicators show that the long-term bull trend (price above 200 days moving average) has been broken and is starting to exhibit the characteristics of a bear market (lower lows and lower highs). We also note that market breadth remains deteriorated. Indicators such as MACD and Mean Reversion show that the market is oversold but without hitting extreme levels. They can move from overbought to oversold conditions quickly and are thus currently very unreliable indicators. The put-to-call ratio reached an elevated level but is not extreme. The Hi-Low indicator continues to flash red. On the other hand, the volume indicator is in the “green” as sell-offs are not always confirmed by rising volumes.

From a geographic point of view, indicators are more favorable for US equities than for European equities.

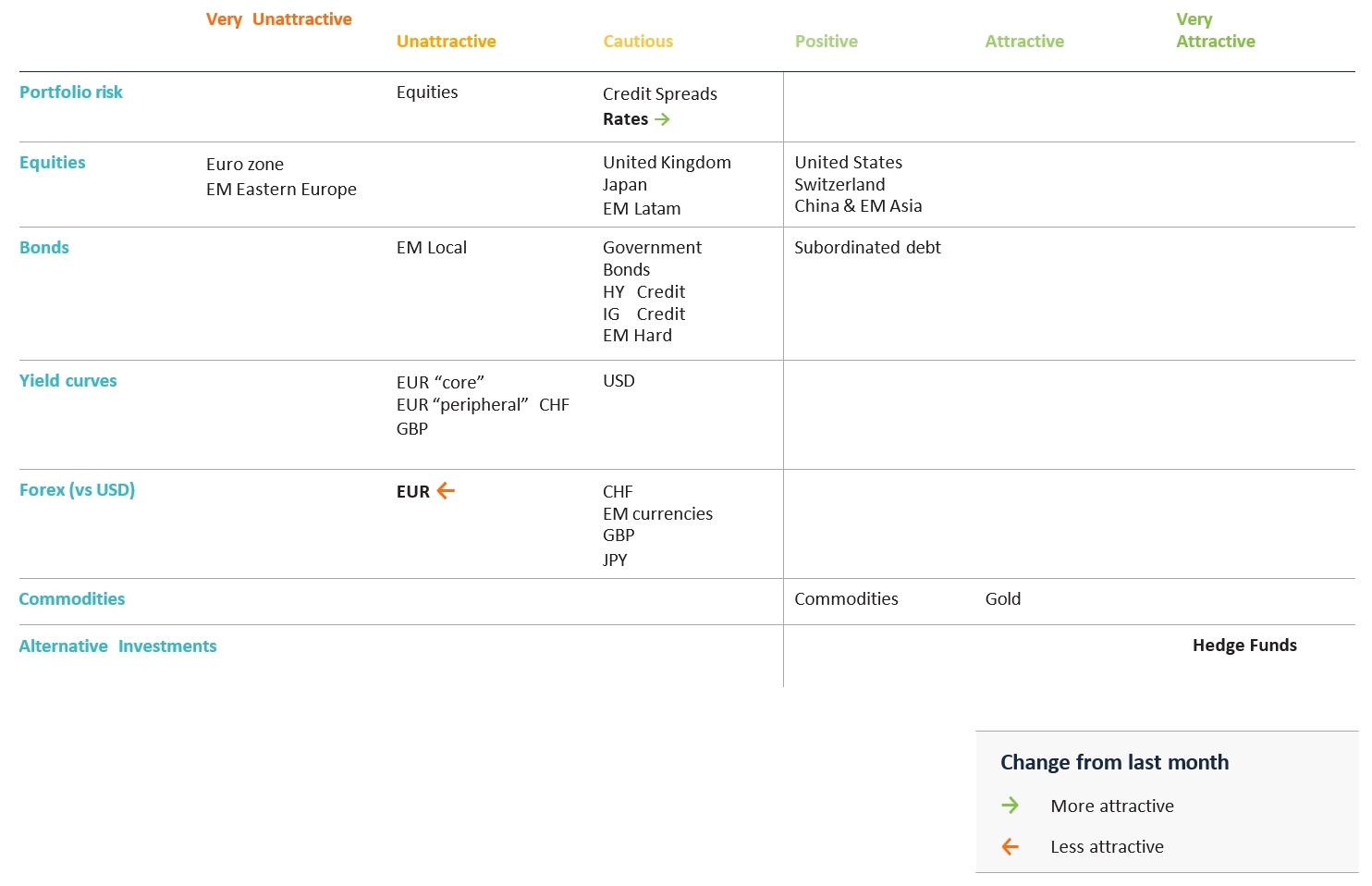

Asset Class Preferences

Equity Allocation

Unattractive

Based on the weight of the evidence, we keep an unattractive stance on equities. The U.S. economy has moved into the late cycle ‘slowdown’ phase, after spending the last 18 Months in Mid-Cycle ‘Expansion’. Late-cycle ‘slowdown’ is consistent with below-average equity market performance, owing to slower earnings growth and multiple compression. Earnings growth remains a tailwind but we expect downgrades later this year. In the meantime, macro uncertainty and volatility to weigh on valuation multiples.

From a regional perspective, we do a have a positive stance on US, Swiss and China / EM Asia equities. Our least favored markets remain the Eurozone and EM Eastern Europe equities (very unattractive). We maintain a cautious view on the UK, Japan and EM Latam. From a sector perspective, Cyclicals and Value have been leading over the last few months but Defensives have been doing better more recently, which is consistent with where we stand in terms of the macroeconomic cycle. We are downgrading Financials to Neutral and upgrading Healthcare to Overweight.

Fixed income allocation

Cautious

On the fixed income side, we are upgrading rates from “unattractive” to “cautious”. Long term rates have pulled back with the decline in inflation expectations due to rising concerns around the global growth outlook. EUR rates have decreased because of mounting concerns around the growth outlook. The ECB has convinced markets it will cap sovereign spreads for now. The stabilization of long-term inflation is priced in by markets that are now focused on the recession. This could benefit rates, particularly in the US. Within government bonds, we do have a preference for USD over EUR as the ECB needs to catch-up with the Fed on the rate cycle.

In credit, EUR spreads widened much more aggressively than USD spreads, reflecting investor nervousness about European assets. U.S. high-yield bond spreads have finally broken out, as evidenced by U.S. high-yield bonds rated CCC now exceeding 1,000 basis points. The recent re- pricing of credit spreads has added value to the segment, especially on the short end. High yield is now becoming attractive from a valuation perspective, with credit spreads implying a 9% default rate over the next 12 months, but technical factors such as low liquidity and the withdrawal of Central Bank support still drive our cautious stance on credit spreads. The bright spot remains the 0-2 year in the credit segment.

Emerging Markets debt recorded its worst start to a year ever (-16%) and is down -20% since its peak in July 2021. Valuations are attractive overall but we need to see some stabilization in EM capital flows before turning positive. EM local debt has to be avoided as EM Central Banks tighten monetary policy aggressively, while EM CPI continues to surprise on the upside.

Commodities

Positive overall.

Keeping a preference stance on Gold Over the last few weeks, commodities have moved from being short-term overbought to oversold as fears of recession now dominate all markets. We remain positive on the asset class and see commodities as an attractive macro hedge. After years of capex underinvestment, many commodities are facing a supply shortage while demand is firm. The invasion of Ukraine by Russia and the sanctions are exacerbating the situation. Energy and commodities are needed for virtually everything, and Russia exports both massively. And unlike in 1973, it’s not just the price of oil, but the price of everything that is surging. Furthermore, the supply shock might be a long lasting one. Indeed, despite ongoing negotiations between Russia and Ukraine, a stalemate with prolonged economic impacts looks likely. We are thus positive on broad commodities. We keep our preference stance on Gold. The yellow metal is one of the few portfolio diversifier remaining. It benefits from lower real bond yields, geopolitical uncertainty and tight supply.

Hedge Funds

Very attractive

Alternative strategies grab their chance to deliver value. After the pandemic, economies are adapting to the changing cost of capital. Investors need a more selective and active approach to investing. As interest rates rise, hedge funds are providing positive returns. Alternative strategies are benefiting from lower liquidity and higher interest rates.

In terms of hedge fund strategies, we are positive on equity hedge with low net exposure and a trading approach. We are also positive on macro and CTA.

Forex

Positive on the dollar against all currencies

In Forex, we find all currencies unattractive against the dollar. We are downgrading the euro from “cautious” to “unattractive”. Indeed, the EUR/USD might face further downside due to the developing Energy crisis. The Ukrainian War and sanctions on Russia weigh on EUR prospects from several angles: macroeconomic growth prospects, inflation, interest rate differentials, external balance, flows of funds. The ECB is now trapped and may have lost control.

We remain cautious on the CHF/USD. Fundamental drivers plead for a firm CHF over the medium term and a flight to safety from European assets is a powerful support. But faster Fed rate hikes than the SNB are supporting the USD in the short-run.

We are also cautious ion the GBP/USD. The Ukrainian War weights on GBP prospects from several angles: macroeconomic growth prospects, interest rate differentials, flows of funds. A hesitant Bank of England is also weighing on the GBP.

With regards to the JPY/USD, growth momentum and monetary policy differentials are weighting on the yen but the peak «rate differential» may be near.

Tactical positioning: our asset allocation matrix