.png)

Despite heightened geopolitical instability, January was characterised by a notable increase in investor risk appetite. While global bond markets remained largely stagnant, global equities advanced by 3%, supported by a "goldilocks" economic backdrop of resilient growth data and moderating inflation. This combination has bolstered expectations for real income gains, fuelling market optimism.

Fixed income and monetary policy

Global bonds faced headwinds from improved economic activity and shifting central bank expectations. In the United States, front-end rates sold off as markets recalibrated, pushing the anticipated timing of the next Federal Reserve rate cut further into the future. Concurrently, Japanese long-term bonds experienced their most significant January decline since 1994, driven by intensifying fiscal concerns.

Credit posted modest gains while US Treasuries are slightly down.

Geopolitical volatility

Geopolitical tensions escalated following the US intervention in Venezuela and administrative threats of tariffs against European nations over the Greenland sovereignty dispute. While the World Economic Forum at Davos facilitated a temporary easing of these frictions, the impact on specific asset classes was pronounced:

• Gold: appreciated by 13% as a primary safe-haven play.

• European defence: the sector saw an 18% surge.

• Volatility indices: curiously, the VIX and EUR/CHF movements remained relatively muted despite the underlying friction.

Equity market dynamics: the "broadening" trend

January marked a significant shift in equity leadership, defined by a broadening of market participation away from US mega-cap technology.

• Global equity markets gained +3.0%.

• US markets: small-cap stocks outperformed, rising 5%, while the "Magnificent Seven" lagged with a loss of -0.3%.

• Regional performance: emerging markets led global returns with a 9% increase, followed by Japan’s Topix at 5%. UK (+5.2%), China (+4.7%) and Euro area (+4.1%) outperformed the US as well.

Commodities and energy

The commodities sector delivered robust returns, with the Bloomberg Commodity Index rising 10%. Energy was a primary driver; WTI Crude climbed 14.3%, while natural gas prices in both Europe and the US surged in response to unseasonably cold winter weather. Silver is up +11.65% and gold +8.8%

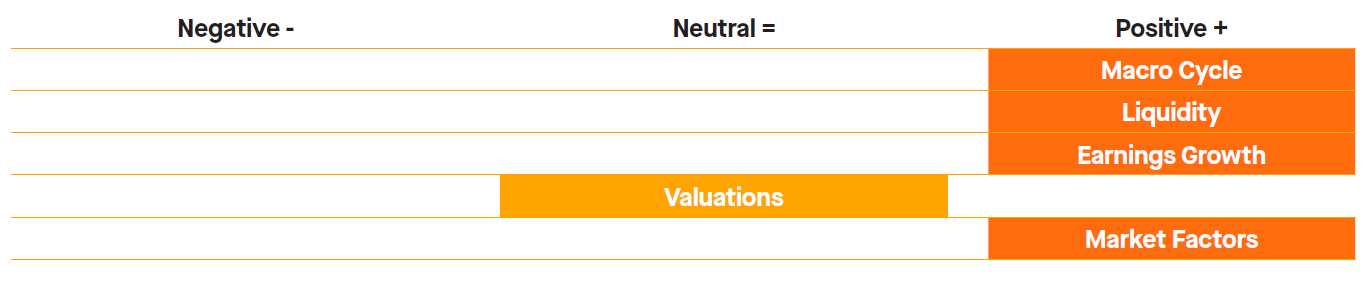

With 4 pillars (macro, liquidity, earnings and market factors) signalling an overweight and 1 in neutral (valuations), the weight of evidence is positive for equities.

• Macro cycle (POSITIVE): domestic fiscal stimulus keeps providing support in US, China, and the Eurozone while trade uncertainties remain lower. We keep our positive macro assessment despite trade disputes, geopolitical risks, and central banks’ rate cutting cycle that will likely slow down.

• Liquidity (POSITIVE): liquidity conditions for financial markets remain positive overall. The Fed has ended quantitative tightening and will purchase Treasury bills to ease short-term funding conditions. Continuing global M2 growth and the weak US dollar contribute to maintaining a supportive liquidity environment.

• Earnings (POSITIVE): earnings remain a tailwind for equities with more sectors to show earnings growth improvement. Technology stocks will continue to benefit from the adoption of AI, while the “old economy” is set to recover from a low base.

• Valuations (NEUTRAL): US large capitalisation stocks remain expensive while international equities are more reasonably valued. However, equity risk premiums remain low by historical standard in both the US and Europe.

• Market Factors (POSITIVE): symphony indicators are positive at 75% allocation to equities (50% US / 25% EU).

• Liquidity (POSITIVE): liquidity conditions for financial markets remain positive overall. The Fed has ended quantitative tightening and will purchase Treasury bills to ease short-term funding conditions. Continuing global M2 growth and the weak US dollar contribute to maintaining a supportive liquidity environment.

• Earnings (POSITIVE): earnings remain a tailwind for equities with more sectors to show earnings growth improvement. Technology stocks will continue to benefit from the adoption of AI, while the “old economy” is set to recover from a low base.

• Valuations (NEUTRAL): US large capitalisation stocks remain expensive while international equities are more reasonably valued. However, equity risk premiums remain low by historical standard in both the US and Europe.

• Market Factors (POSITIVE): symphony indicators are positive at 75% allocation to equities (50% US / 25% EU).