.png)

Executive summary

- Despite challenging headlines (Ukraine invasion by Russia, roaring inflation, Fed hiking rates, etc.), US stocks performance has been diverging from bonds since the second half of March. With real rates still in deep negative territory, the US consumer being in a strong shape, growth expectations remain fairly strong and earnings growth estimates showing signs of resilience, the overall impact of persistent inflationary pressures and rising interest rates on risk assets has been relatively mild.

- However, there are still some reasons to lean on the cautious side. Global financial conditions are starting to tighten significantly. Inflationary pressures are likely to rise further on the back of the commodity supply shock we are currently experiencing. Although stagflation is not our core scenario, a macroeconomic context characterized by lower economic growth and higher inflation often results in poor real returns for risk assets. While equity valuations look more attractive, there is an elevated risk for earnings growth estimates being revised downward in the near-term. Indeed, top-line growth should benefit from higher nominal GDP but in the current context of higher inflation, profit margins are likely to suffer in some specific sectors. Overall, our leading indicators (macro & fundamental) continue to point towards challenges for equity markets. Our coincident indicators (market factors) are not positive enough to change this view. On the contrary, the long-term equity bull market trend is being challenged while market breadth is not showing much signs of improvement.

- The weight of the evidence (i.e the aggregation of our fundamental and market indicators) remains negative. As such, we maintain a disinclination view on equity markets in general while we remain positive on US and Japanese equities. Our least favored market remains Eurozone equities (strong disinclination) and we maintain a cautious view on UK and Swiss markets.

- In Fixed Income, we remain cautious on rates and keep a disinclination stance on credit spreads. In Forex, we keep a disinclination stance on the EUR. We remain cautious on the Sterling and are downgrading the Japanese Yen to cautious. We remain positive on the Swiss Franc. We are upgrading Commodities from cautious to positive. We keep our preference stance on Gold.

Indicators review summary

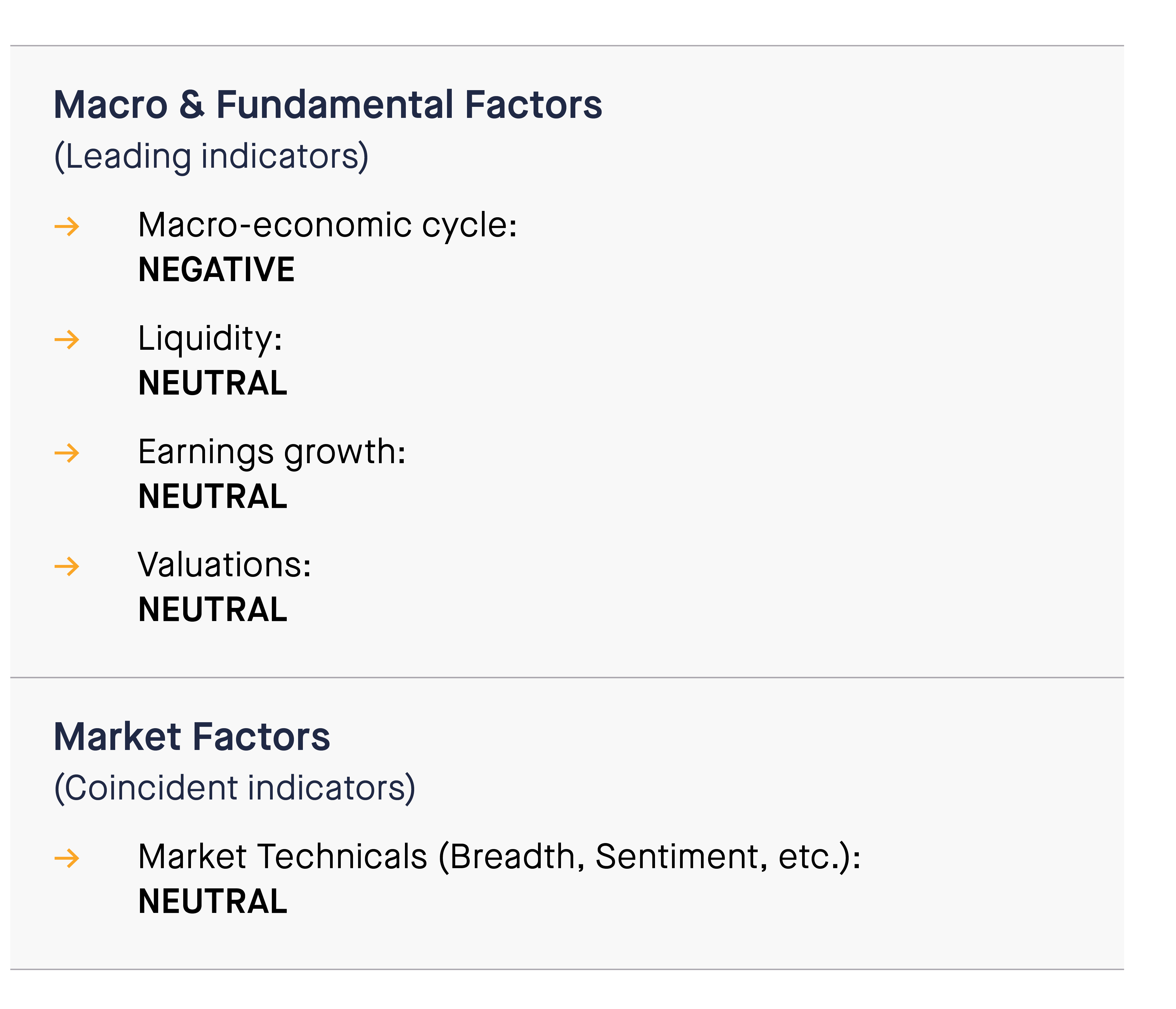

On an aggregated basis, our indicators are pointing towards a DISINCLINATION on risk assets.

Indicator #1

Macro-economic cycle: Negative

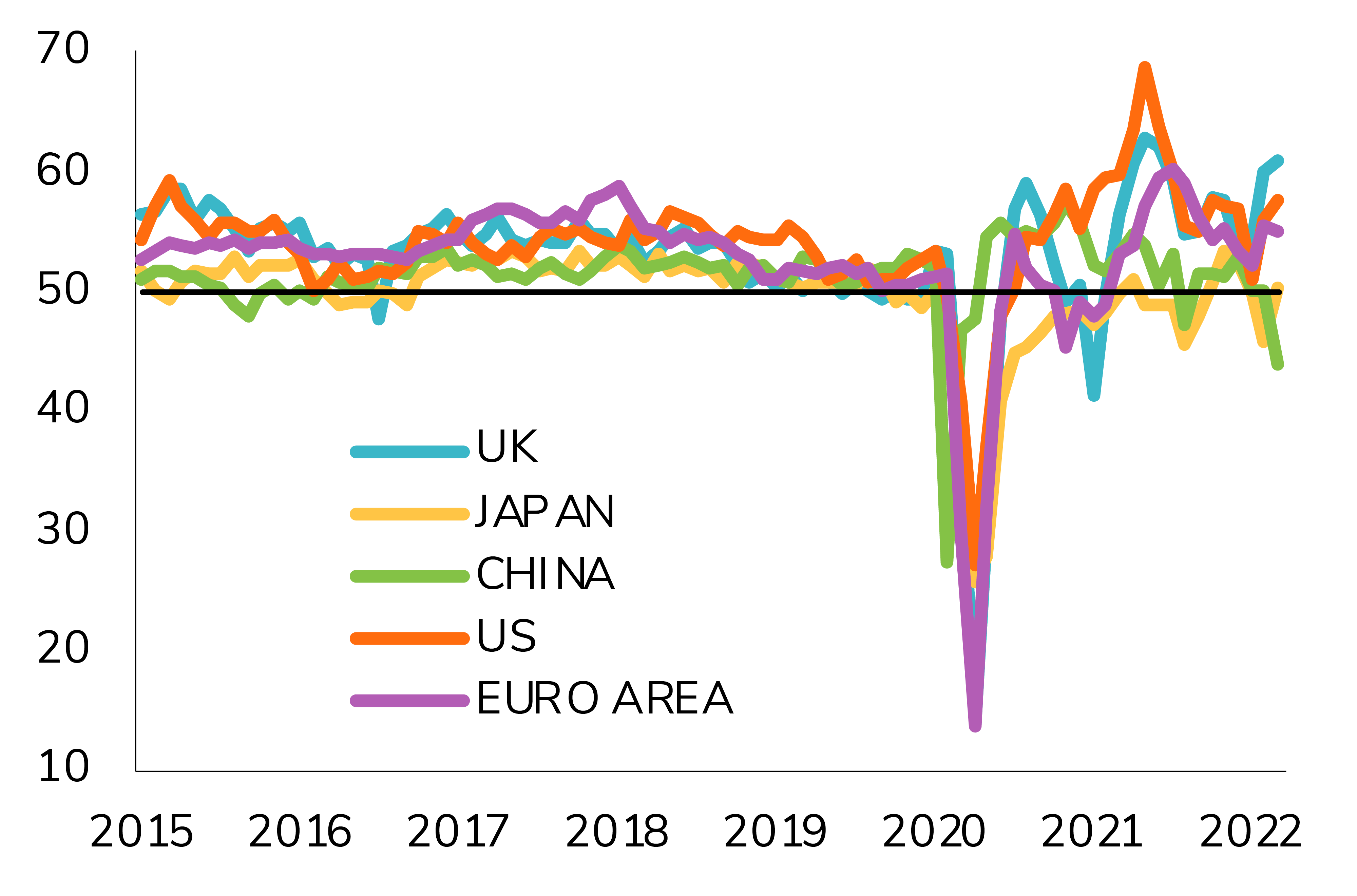

We believe that the macro perspective has deteriorated compared to last year. Our “core” scenario for 2022 is adjusted towards weaker growth and higher inflation. Global growth was expected to be above trend before the conflict. Currently, global growth remains firmly positive and the impact of Omicron on the US and Europe has dissipated. However, the Ukraine/Russia war is likely to decrease global real GDP growth by at least 1 per cent due to rising energy prices, negative impact on global trade, deteriorating consumer and corporate sentiment and the risk of worsening financial and liquidity conditions. Meanwhile, inflation keeps rising in the US and in Europe and exceeds expectations. The Russia-Ukraine war is creating a supply shock with moderate to severe effects – depending on the extent and length of the sanctions. This should lead to higher inflation than expected. As such, our macro indicator is NEGATIVE. However, stagflation is not our core scenario as global growth in developed countries remains above trend – see PMI composites below.

Indicator #2

Liquidity: Neutral

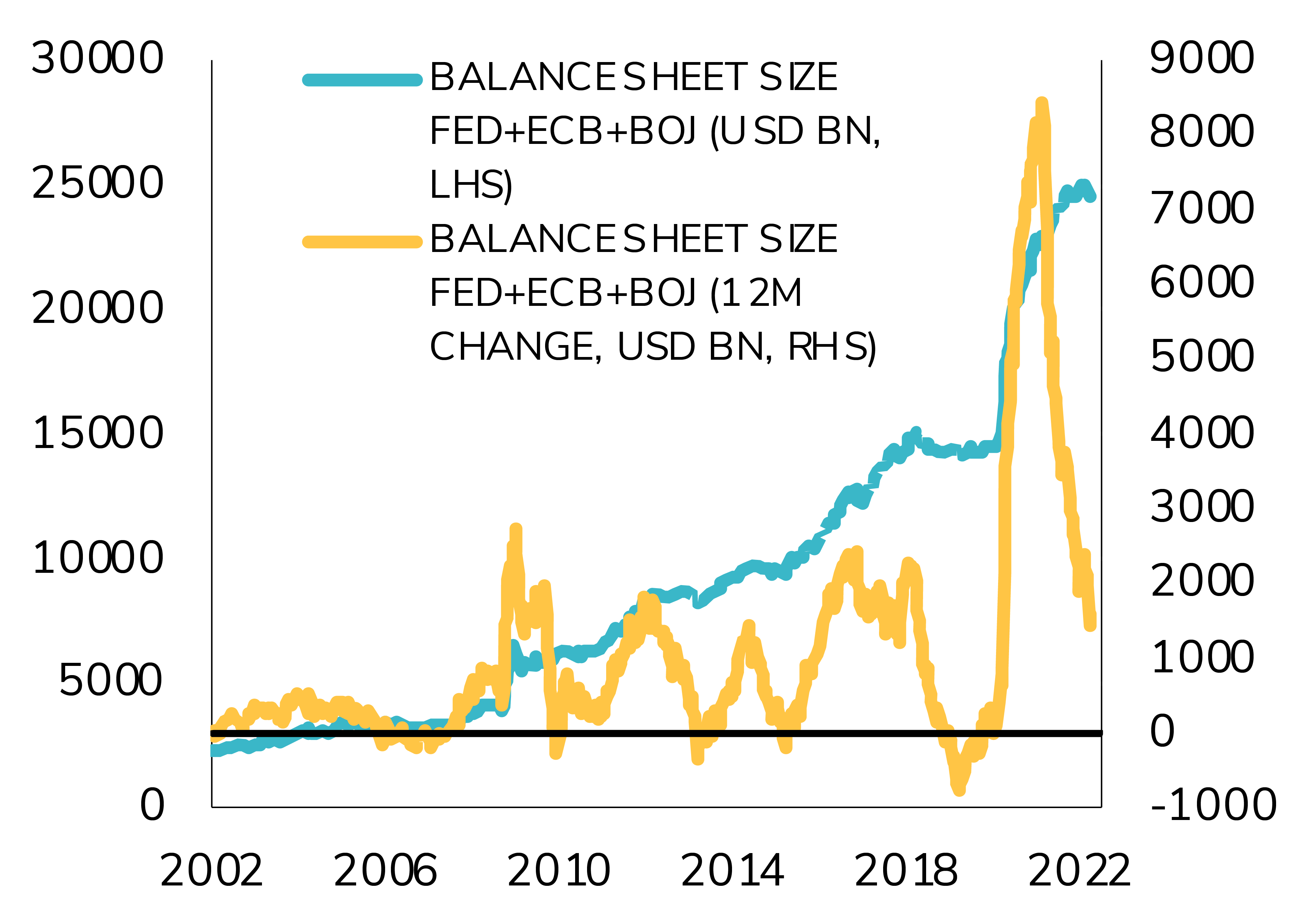

In the US, Monetary policy is unlikely to provide much support to the economy and financial markets. On the back of a strong job market and the highest inflation number over the last 40 years, the Fed will stick to its plan to hike rates and tighten liquidity despite the conflict. On the other hand, the European Central bank may be more cautious than expected regarding rate hikes and QE tapering. Should the geopolitical and financial crisis deepen, fiscal and/or monetary policy should come as a support not only in Europe but also in the US. For the time being, we view the liquidity conditions as NEUTRAL.

Indicator #3

Earnings growth: Neutral

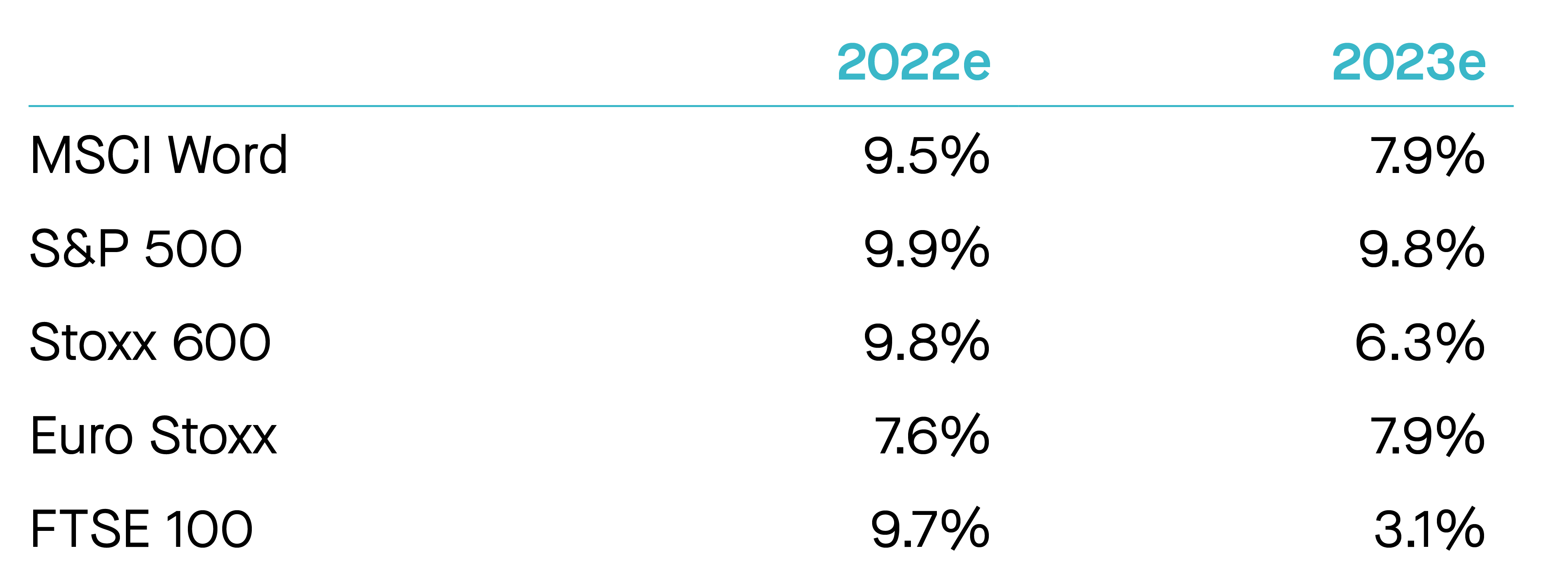

To the surprise of many, we continue to see analysts revising earnings upwards for 2022. Expectations for S&P 500 earnings growth are now at 9.1%, up from 7.0% at the end of December 2021. The historical norm has analysts lowering annual earnings estimates on average during this period. Balance sheets remain solid as well and companies have room for more share buybacks. As such, we continue to see earnings growth as being a tailwind for equities but still believe that some downward earnings growth revision could happen later this year. Indeed, after a very strong earnings rebound in 2021, base effects are no longer very favorable. While profit margins have been resilient until now, high input cost pressures can hurt individual companies and some specific sectors. That being said, we still expect high single digit earnings growth. Share buybacks provide strong support while value / cyclicals sectors benefit from rising commodities prices. In Europe, banks are suffering from Russian exposure and flattening yield curve. We expect low single digit growth for European earnings this year.

Source: IBES

Indicator #4

Valuations: Neutral

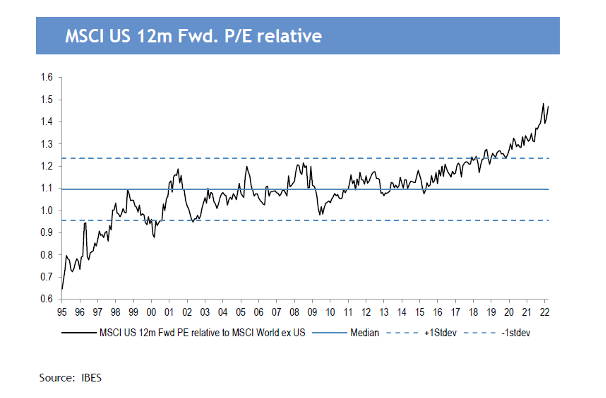

Global equity valuations have eased but are still above historical average in the US. Relative valuations of the US versus the rest of the world are a clear challenge as the region is trading extremely expensive versus peers, on most measures. One rational explanation is the fact that strong US earnings delivery supported this outperformance. Compared to bonds, equity markets remain attractive as real bond yields remain in deep negative territory. That means that investors are incentivized to keep investing into risk assets. We also note that with the return of inflation, investors consider stocks as being a much better hedge against inflation than bonds. As such, asset allocators are rotating from fixed income funds into equity funds. This can push equity valuations higher. On a more cautious note, we feel that increased geopolitical risk, growing economic sanctions to Russia and downgrades in earnings are not fully priced yet. As such, this indicator remains NEUTRAL.

World ex-US

Indicator #5

Market technicals: Neutral

Our market indicators are NEUTRAL but have been deteriorating recently and show that the recent market rebound is weakening. The low frequency / long-term indicators show that the long-term bull trend (price above 200 days moving average) has been broken – albeit by a small margin. Volume signal is becoming a headwind, i.e market advance is not confirmed by rising volume while correction are confirmed by rising volume. We also note that market breadth keeps deteriorating. Unlike the US, our European indicators give a negative signal on an aggregated basis.

Asset Class Preferences

Equity allocation:

Disinclination

Based on the weight of the evidence, we keep a disinclination stance on equities. The U.S. economy has moved into the late cycle ‘slowdown’ phase, after spending the last 18 Months in Mid-Cycle ‘Expansion’. Late-cycle ‘slowdown’ is consistent with below-average equity market performance, owing to slower earnings growth and multiple compression. Earnings growth remains a tailwind but we expect macro uncertainty and volatility to weigh on valuation multiples. From a regional perspective, we do have a positive stance on US and Japan equities. Our least favored market remains Eurozone equities (strong disinclination). There is significant geopolitical risk and energy dependency. Moreover, the upcoming French elections could create some volatility as well. Outside Eurozone, we maintain a cautious view on UK and Switzerland.

Fixed income allocation:

Disinclination

On the fixed income side, we stay cautious on rates. A huge bear flattening of USD and EUR yield curves has been observed over the last few months as surging inflation increases the pressure on central banks. Medium and long-term inflation expectations rose to multi-year highs due to the surge of energy and commodity prices and rising wages. In the Eurozone, the rates curve acknowledges a coming exit of the ECB Negative Interest Rate Policy, with sovereign spreads amplifying the move. Overall, we see some divergence across government bonds markets. US short rates are now set on a very aggressive path while the EURs still have work to do. We thus find some value in the short-end of the US Government curve. We are however downgrading the EUR Peripheral curve to disinclination due to a potential PEPP (Pandemic emergency purchase program) /APP (Asset purchase program) early exit (July) and French election as possible headwinds. In credit, we keep a disinclination stance. The recent revaluation of credit spreads has added some value to the segment, especially in the short duration bucket. However, Investment Grade and High Yield are still not cheap compared to current volatility, poor liquidity and the lack of support stemming from central bank. A bright spot is the 0-2 year segment in Investment Grade / High Yield. Emerging markets debt recorded their worst start of the year ever (-10%). We remain cautious on this segment but believe the overall context is improving. First, valuations are attractive overall. Moreover, Chinesereal estate added positive color in recent days which underpinned our Asian High Yield attractive valuation thesis. Another positive is the sharp rebound of capital flows into Emerging Markets bonds in the last few weeks. We are thus carefully monitoring this segment. Last but not least, we are upgrading subordinated debt to positive from cautious. This matured and resilient asset class is still offering some attractive yield premiums and this despite solid capital position.

Commodities:

Positive overall (upgrade). Keep a preference stance on Gold

We believe that commodities might be short-term overbought but remain long-term under-owned. After years of capex underinvestment, many commodities are facing a supply shortage while demand is firm. The invasion of Ukraine by Russia and the sanctions are worsening the situation. Energy and commodities are needed for virtually everything, yet Russia exports everything, and unlike 1973, it’s not just the price of oil, but the price of everything that is surging. And the supply shock might be a long lasting one. Indeed, despite ongoing negotiations between Russia and Ukraine, a stalemate with prolonged economic impacts looks likely. We are thus upgrading our view from cautious to positive. We keep our preference stance on Gold. The yellow metal is one of the few portfolio diversifier remaining. It benefits from lower real bond yields, geopolitical uncertainty and tight supply.

Forex:

Positive on the dollar and the Swiss franc; disinclination stance on the euro; downgrading the yen

In Forex, we keep our disinclination stance on the euro. The Ukrainian War weights on EUR prospects from several angles: macroeconomic growth prospects, interest rate differentials and flows of funds. We stay cautious on the Sterling and positive on the Swiss Franc. Fundamental drivers plead for a strong CHF over the medium term. Flight to safety from European assets is a powerful support. We stay cautious on GBP/USD. We are downgrading the Japanese yen from positive to cautious. Growth momentum and monetary policy differentials are weighting on the yen.

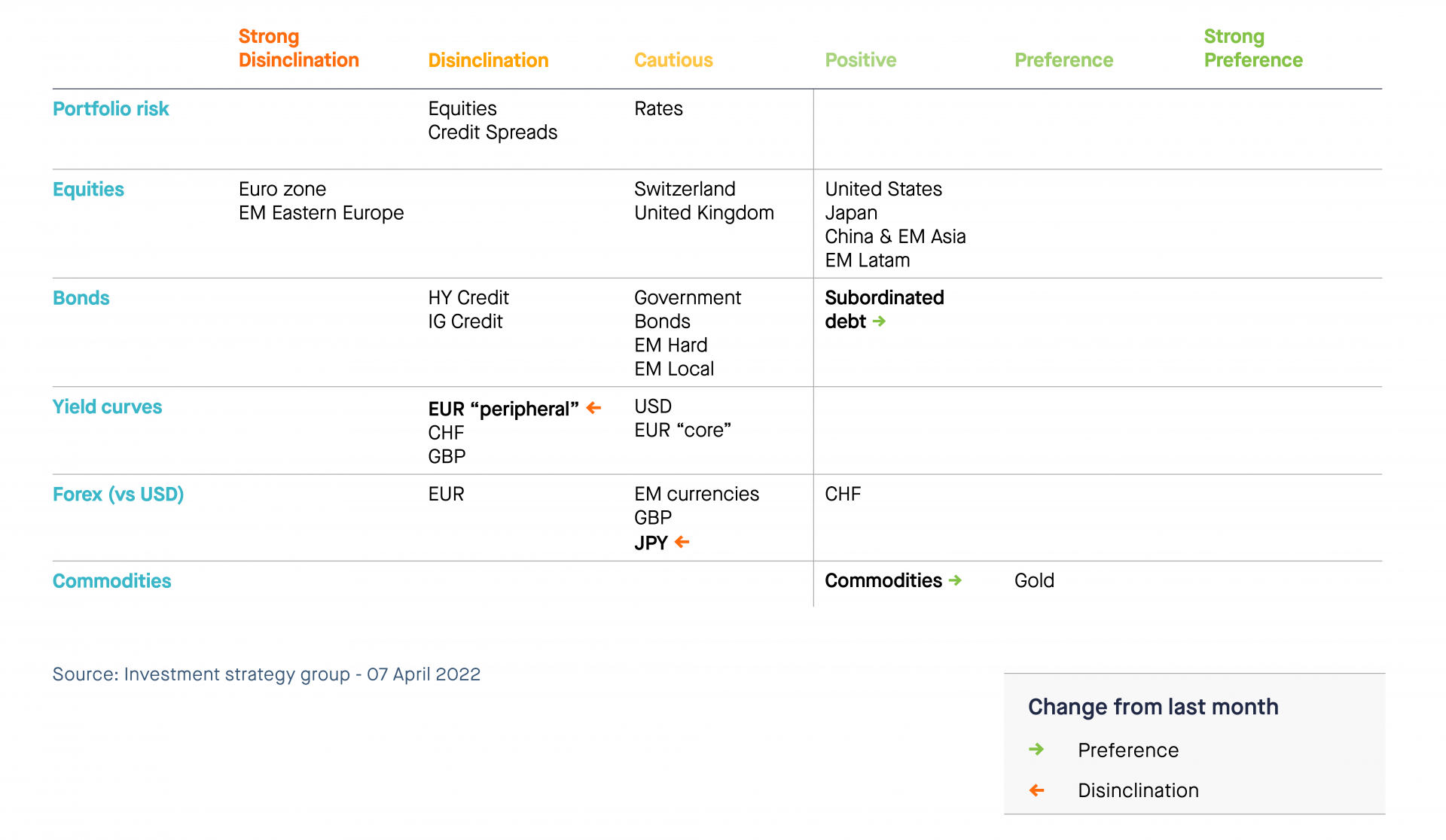

Tactical positioning: our asset allocation matrix