.png)

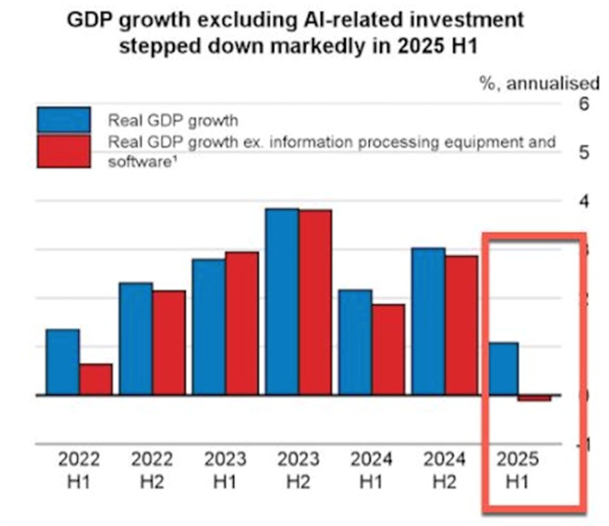

AI investments remain a major driver of GDP growth

What happened last week?

Global markets

A good week for equity markets while waiting for a rate cut

Last week, global equity markets continued to move higher as investors are waiting for an interest cut by the Fed this week. In USD, the MSCI All Country World Index rose 0.6%. The S&P 500 was up 0.4% during the week, the Nasdaq 100 climbed 1.0% while Europe was up 0.8% and Emerging Market was up 1.4%. Semiconductors and software stocks were strongly up last week at +4.3% and +5.2% respectively. Within Emerging Markets, Taiwan and South Korea shined being up +1.7% and +5.0% helped by the sentiment towards semiconductors and AI.

US

Last week in U.S. equities climbed higher, with leadership coming primarily from growth and cyclical-oriented sectors. Worth noting is the outperformance of smaller caps with the Russell 200 up 0.9% helped by the strong performance of US regional banks (up +3.5% over the week)

The standout sectors were Communication Services, which posted the strongest weekly gain, closely followed by Consumer Discretionary and Information Technology. These sectors were powered by a rebound in mega-cap and semiconductor names, which regained momentum after recent softness. Software that had a difficult year so far did rebound following the good results of Salesforces.

In contrast, more defensive and rate-sensitive sectors lagged behind. Real Estate, Consumer Staples and Energy posted the smallest gains for the week, reflecting investors’ preference for cyclicals and growth over safety despite the uncertainties.

Overall, the market’s breadth was wide with all 11 of the S&P-500 sectors ended the week in the green, but it was the pro-growth areas and small-cap stocks that really drove the rally.

Europe

Last week European equity markets delivered a good performance being up 0.4% in EUR but 0.8% in USD, with cyclicals such as autos, industrials and financials emerging as the primary drivers of strength.

In particular, the autos & parts sector stood out, rising around 5–6 % as investors cheered stronger global vehicle demand and favorable sector momentum.

Technology shares posted moderate gains, helped by demand for semiconductor and chip-equipment names like in other regions.

Overall, the tone was constructive yet selective: investors rotated away from defensive and stable-yielding sectors toward industries more sensitive to economic cycles.

Rest of the world

In China’s third-quarter earnings season, topline growth improved, though sector margins diverged. MSCI China companies posted 3Q25 revenue growth of 2% YoY, with earnings growth sustained at 4% YoY. Following earnings releases, consensus profit forecasts were revised upward, most notably for non-bank financials. Sector-wise, non-bank financials and technology delivered robust earnings growth of 81% and 42% respectively, while renewables also showed a strong 74% YoY rebound, partly due to a low base. The property sector remained the main drag on overall earnings.

Company guidance was mixed: consumer sectors stayed lukewarm, while tech remained upbeat. Most companies continue to focus on cost control and product differentiation to support profitability.

Our view on equity

Equity asset class

POSITIVE in the current environment

We shift to a Negative stance on government bonds. Positive global growth dynamics, price pressures in the US and profligate fiscal policies reduce the attractiveness of long-term government bonds as a potential hedge for economic downturn and increase the risk of higher long-term yields. Limited prospects of further central banks’ rate cuts and unattractive yield curve slopes at the front-end also reduce the attractiveness of government bonds on short-to-medium term maturities.

Earnings

POSITIVE as breath to increase

Earnings remain a tailwind for equities, supported by a strong third-quarter earnings season and expectations that growth will accelerate and broaden in 2026. Technology stocks should continue to deliver robust performance, while the “old economy” is set to recover.

Valuation

NEUTRAL as US large caps remain expensive

US technology stocks remain expensive, although growth and profitability provide some support while international equities are more reasonably valued. Equity risk premia remains low in both the US and Europe.

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

Related Articles

Global equity markets performance between 26 June–3 July 2026 was marked by a partial unwind of an unprecedented Q2 chip rally, a softer US jobs report that eased near-term Fed tightening expectations, a European defence-and-industrials rally ahead of the NATO Ankara summit, and extreme volatility in South Korean chipmakers that dragged emerging markets sharply lower.

Global equity markets sold off sharply in the week to Friday 26 June 2026, as investors reassessed AI-related valuations against a backdrop of hawkish Federal Reserve signalling and sticky inflation. The MSCI ACWI fell 2.2%, with technology and semiconductors bearing the brunt of the decline — the Nasdaq 100 lost 4.2% and the iShares Semiconductor ETF shed 7.7%. The sell-off was sharpest in AI-exposed markets across North Asia, with the KOSPI and TAIEX both falling over 5%. Defensives and small-caps outperformed globally, with healthcare, insurance, and consumer staples all posting gains. Micron's record quarterly earnings provided a late-week counterpoint, but were insufficient to reverse the broader de-rating of growth assets.

A weekly review of global equity markets for the period ending 12 June 2026, covering the impact of renewed US-Iran tensions and the ECB's first rate hike since 2023 on regional equity performance, the rotation away from mega-cap technology into financials and cyclicals, and the significance of the SpaceX IPO as a landmark moment for the AI infrastructure investment cycle.