We are sorry that for legal reasons we are not able to help US citizens or Canadian residents other than in Ontario, Quebec, or Alberta. Best wishes for the future…

Restricted access

We are sorry that for legal reasons we are not able to help US citizens or Canadian residents other than in Ontario, Quebec, or Alberta. Best wishes for the future…

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material.

This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor.

This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

Are we headed towards an inevitable US debt ceiling crisis?

The possibility of a “technical default” by the US has been raised as the current debt limit for the US government, set by law, is expected to be hit sometime during the summer.

The possibility of a “technical default” by the US has been raised as the current debt limit for the US government (or debt ceiling), set by law, is expected to be hit sometime during the summer.

A new law must be adopted both by the House of Representative (controlled by Republicans) and by the Senate (controlled by Democrats) to raise the debt ceiling. This is necessary for the US Treasury to be able to issue additional debt and pay for its planned spendings. For the time being, there is no agreement between the two Chambers on a legislation to raise this limit.

Absent a new law, the US is at risk of defaulting on some debt payment later this year. Such default would be “technical” since it would be caused by an arbitrary legislation preventing new debt issuance, not by weak fundamentals preventing the US Treasury to raise cash. Once the ceiling is raised, all missed payment would be fully paid, even if with a delay.

This is not the first time such “gridlock situation” happens, and this would even not be the first time the US Treasury misses on some payments. In fact, a “technical default” of the US government has already happened once: in 1979.The US failed to make timely payments on USD 120mio T-Bills that were due in April and May on an aggregate amount of debt of USD 800bn. The Bills were paid later, but in full.

In our view, the current situation is eminently political, with the prospect of the 2024 US presidential election in sight. To agree to raise the debt ceiling, Republicans ask for spending cuts and various measures that are not acceptable to Democrats ahead of the presidential election. Republicans have no incentive to agree on a debt limit increase “to finance the Democrats’ programme”, as it would likely weaken their position ahead of the election.

As such, the political setup makes it highly likely in our view that no solution will be found until the ceiling is hit, and the US Treasury must start taking exceptional measures to fulfil its financial obligations (including shutting down parts of the US administrations as it happened in 2013 and 2018-19). Only when the crisis is effectively there, and it starts hurting US economic activity, will Republicans and Democrats have an incentive to take steps towards each other.

They will then be able to tell their electorate that they are “being reasonable to avoid inflicting undue pain to the US economy and its people”. Ultimately, the debt ceiling will have to be raised at some point, or the impact on the US economy would be hugely negative, for example: sudden halt in government spendings, social programmes, public servants’ wages, impact of a default on financial markets or a shock of confidence for US households and businesses. It is “only” a matter of time, and political negotiations, before the ceiling will be raised.

Our conclusions are that:

• The debt ceiling debate and concerns will likely grow in intensity as we get closer to the deadline, likely to be hit during the summer • Until then, and possibly beyond, concerns around a “technical” default of the United States may continue to rise. • As during previous episodes (especially summer 2011), this would likely cause volatility in financial markets, with downward pressures on US Treasury securities maturing in the summer, for which the reimbursement could be postponed till the debt limit is finally raised. • Importantly, the impact should be felt essentially by those short-term US Treasury bonds (at risk of delayed reimbursement), and by assets linked to US economic growth (typically equity markets). • Bonds issued by corporate, especially those with strong balance sheet/high investment grade ratings, should not be overly impacted by those potential developments. For the most solid companies, their bonds may even benefit temporarily from the situation as some investors are likely to see them as attractive alternatives to replace their customary holdings of short-term US Treasury Bills.

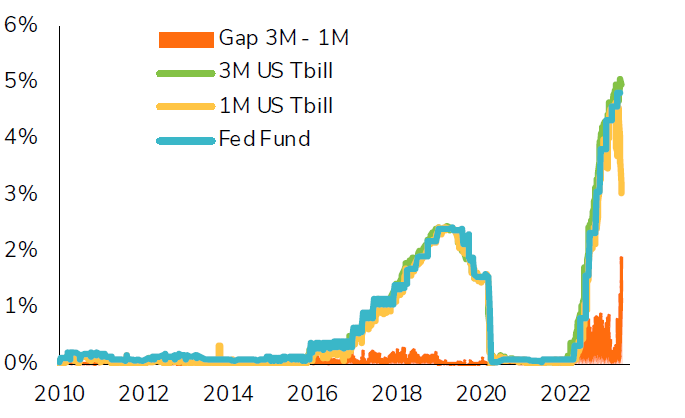

US short-term interest rates (Fed fund rate, 1-month & 3-month TBill rates) and 3m/1m differential

Source: Banque Syz, Bloomberg

As concerns of a US technical default rise, investors are ready to give up some yield to avoid being exposed to a missed payment by the US Treasury. 1-month rates incorporate a large premium for TBill maturing before the summer, yielding only 3% while 3-month rates and Fed Fund rates are close to 5%. The widest gap ever recorded, and a good illustration of rising concerns around this issue.

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

.png)

Source: Banque Syz, Bloomberg

Source: Banque Syz, Bloomberg