We are sorry that for legal reasons we are not able to help US citizens or Canadian residents other than in Ontario, Quebec, or Alberta. Best wishes for the future…

Restricted access

We are sorry that for legal reasons we are not able to help US citizens or Canadian residents other than in Ontario, Quebec, or Alberta. Best wishes for the future…

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material.

This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor.

This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

Below are answers to our client’s most frequently asked questions on recession risk, French elections, Chinese equities, the cryptocurrencies crash and our asset allocation preferences.

Prominent Wall Street banks and high profile corporate leaders recently said that recession risk is on the rise in the US. What is your take on this?

This cycle is different as it is a supply shock and not a demand shock. Monetary policy makers need to bring down inflation by tempering demand and this inevitably leads to negative economic surprises and higher odds of recession.

That being said, we keep the view that the US economy still benefits from some “shock absorbers”. The US consumer remains in good shape, thanks in part to a strong job market (unemployment rate near record low, job openings remain well above the number of unemployed people). Wage growth partly offset the rise of inflation and households can still tap into their savings. It is true, however, that consumer sentiment has been sharply declining recently as rising prices in goods & services, the stock market rout, the surge in monthly mortgage payments (US mortgage rates have increased from 3.2% to 5.7% in 2 years) and unaffordable housing prices (+30% over the last 2 years) are weighing on the morale of US households. Still, we continue to believe that the US consumer –a key pillar of the economy – is in better shape than in 2008/2009 or 2001/2002.

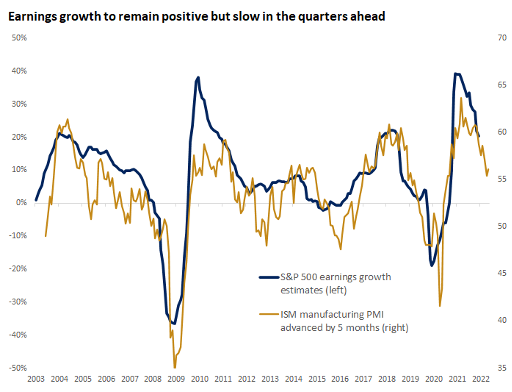

Corporate America is another shock absorber. Corporate balance sheets are in decent shape and S&P 500 earnings growth has been revised upward since the start of the month. 2023 earnings growth prospects look much more challenging but so far, the current equity bear market has been driven by a liquidity squeeze (i.e Fed tightening weighing on valuations) rather than a profit recession.

From a macroeconomic point of view, the Citigroup economic surprise index has been declining sharply over the last few months. Quarter-on-quarter annualized US GDP growth was -1.3% in the first quarter and based on the Atlanta Fed GDPNow forecast, the U.S. economy has either stagnated or contracted again in the second quarter.

If so, the economy already fits the technical definition of a recession. However, we note that the Philadelphia Fed survey of professional forecasters suggests that only 20% of them think there will be a real GDP contraction this year. PMIs remain in expansion territory. As we stated previously, we also believe that the current monetary policy tightening cycle can be partly offset by some fiscal support.

Finally yet importantly, nowadays recessions are better predicted by the state of financial markets than by the analysis of economic activity. The inversion of part of the US yield curve, defensive stocks leadership and the fact that the S&P 500 is already down by 24% from its January 2022 peak (perfectly in-line with the median drawdown observed during a recession) seem to already price in this risk to some extent. However, other market indicators are NOT pointing towards an economic recession: Two such indicators are the 10-year US Treasury bond which continues to rise, and the credit spreads which have widened but remain well below the levels observed during previous recessions.

While a prolonged, deep recession is not our central scenario, some downside risks could materialize it:

1. A financial market accident

The true risk for the economy is a financial market accident triggered by the current liquidity squeeze. Nowadays, financial markets lead the economy and not the other way around. As it already happened in the past, monetary policy tightening could also lead to a financial market accident with deep and lasting consequences on both economic activity and risk appetite. This can happen outside the US as well. It can take the form of an emerging markets crisis (Turkey, Argentina, etc.), or the end of Yield Curve Control in Japan triggering a brutal and massive end of carry trades, a deepening political crisis in Europe, etc. Dysfunctional markets, massive liquidation or deleveraging could lead to important market damages which could ultimately affect the cost of capital and push the economy into a negative feedback loop;

2. A sharp decline in housing market prices and activity

As mentioned earlier, the US consumer is a key pillar of the US economy (70-80% of GDP) and could be hit by a triple whammy effect (in addition to soaring inflation): i) a potential reversal in the job market from currently tight conditions; ii) financial markets losses; iii) higher mortgage rate hitting the housing market. Regarding the later, the rise in mortgage rates from 3.2% to 5.7% over the last 2 years at a time house prices are expensive (+30% in 2 years) could lead to a severe slowdown in housing market. This is by the way a looming risk in many countries outside the US;

3. Negative revision to earnings

In Q1, earnings and corporate margins have been surprisingly resilient, but are starting to see some negative revisions due to the slowing economic activity. A strong dollar does not help US earnings either.

Source: Bloomberg

Q&A #2 —

Has your market outlook/strategy changed recently?

As outlined in our H2 2022 market outlook, we believe that volatility, uncertainty, complexity, and ambiguity in the financial markets will continue to dominate the environment for some time. So how should we manage our client portfolios in this VUCA world?

We believe that the key to success will be in keeping to our investment philosophy and principles, namely:

Encourage our clients to stick to their financial goals and risk profile

Follow our investment process thoroughly

Favour a agile and dynamic asset allocation managed with precise quantifiable criteria

Invest asymmetrically to avoid major equity and market drawdowns

Be selective in our stock and credit picking

Think out of the box to identify contrarian, less favoured investment opportunities.

We believe that a combination of these principles is vital to managing our clients’ assets through the current VUCA environment.

With regards to tactical asset allocation, our stance on risks assets hasn’t changed since our last monthly investment strategy committee. Overall, the weight of the evidence (i.e the aggregation of our fundamental and market indicators) remains negative for equity markets. As such, we maintain an “unattractive” view on stocks. Our least favored market remains the Eurozone (very unattractive). We do a have a positive stance on US and Swiss equities, however. We are cautious on Japan and Emerging Markets Latam was downgraded from positive to cautious.

From a sector and style preferences perspective, we favor a diversified approach mixing defensive growth, high quality tech names and some value names (e.g some late cyclical stocks trade on very attractive free cash flow yields). We keep a quality and large-caps bias in our portfolios.

In Fixed Income, we have a cautious view on credit spreads and see rates as being unattractive. The bright spot in fixed income seems to be the 0-2 year investment grade & high yield segment.

In Forex, we are cautious on all currencies against the dollar.

We maintain a positive view on Commodities and a “preference” stance on Gold.

In the current market context, alternative investments, including equity market neutral, volatility arbitrage and macro offer a means of building value and resilience into portfolios. We have a positive view on liquid hedge funds strategies.

Q&A #3 —

What could trigger a rebound of the S&P 500?

1. A sharp decline in commodity prices?

Rising energy, industrial metals and food prices are major contributors to the current crisis, with uncomfortably high inflation forcing central banks to turn off the liquidity tap. The sanctions imposed on Russia for its invasion of Ukraine are having a major impact on global supply. In terms of energy, and oil in particular, few initiatives have been put on the table by the OPEC to increase production. In the US and Europe, climate priorities continue to take precedence over new exploration and production projects. Europe seems to be running out of solutions as the Russian threat to gas supplies becomes clearer. Finally, no progress seems to have been made in the negotiations with Iran and Venezuela. Only a major destruction of demand following a sharp recession seems likely to restore the balance between energy supply and demand, a scenario that is not the most favorable for risky assets.

2. Peak inflation?

There are many indications that we are close to what is known as peak inflation. In other words, inflation figures should soon start to fall, even if commodity prices remain at current levels. There are several reasons for this. Firstly, "base effects" (i.e. a fall in inflation due to more favourable comparison levels) should soon materialise. Another phenomenon that should allow the inflation rate to fall is a slowdown in final demand. In our "soft landing" scenario, final demand should continue to grow in the coming months but will still remain below 2021 levels. This means that demand pressures on consumer prices will no longer increase, leading to a gradual smoothing of inflationary pressures. On the supply side, even a gradual reopening of the Chinese economy should help to ease the pressure on supply chains, although normalisation may take time, as we saw in 2021. There could therefore be some encouraging developments on the inflation front in the second half of the year, but with one caveat - and a big one. If inflation slows down only gradually, it will still be well above central bank targets for the current year. Against this backdrop, it seems difficult to envisage a U-turn by the Fed, for whom it has become essential to remain credible with investors, consumers and businesses.

3. A negotiated deal between Russia and Ukraine?

Although no one seems to be making a move towards a peace agreement, it would appear that negotiations between Russia and Ukraine are continuing behind the scenes. At this stage, a successful outcome would of course have a very positive effect on the markets.

4. A weakening of the dollar?

The sharp rise in the dollar since the beginning of the year could weigh on the growth of US companies' profits, but above all, it is a real headache for the rest of the world. The strength of the greenback makes raw materials valued in dollars (crude oil, copper, aluminum, etc.) more expensive to import. It also forces central banks (ECB, SNB, emerging markets) to pursue a more restrictive monetary policy in order to fight imported inflation. The strong dollar also increases the cost of servicing the rest of the world's debt as many countries have denominated a large part of their borrowing in dollars. Finally, the difficulties faced by many countries with the appreciation of the dollar could tip us into a new international liquidity crisis. Indeed, the rise in commodity prices is forcing many countries to draw on their dollar reserves to finance their purchases. Therefore, a weakening of the dollar would be seen as good news by the markets as it would imply an increase in liquidity and a decrease in insolvency risks. The end of restrictions in China and a start of monetary policy tightening by the ECB could help weaken the dollar.

5. Investors on the hunt for bargains?

A review of the price/earnings (P/E) ratios of the various equity markets shows that most of the decline in equity indices is due to a compression of valuation multiples and not to a downward revision of earnings growth expectations. The fact that equities have become cheaper than they were a few months ago must, however, be qualified by the following elements. Firstly, multiples as a whole have returned to the median levels of their 20-year history. We are therefore not (yet) at an undervalued level. Secondly, a downward revision of earnings can still occur in the second half of the year. Finally, equity markets are now competing with other asset classes: for example, bonds have seen their yields rise in recent months and are now considered as an attractive investment again by some asset allocators.

6. The bar for a hawkish surprise is high.

The market expects the Fed to hike rates by another +175bps by the end of the year. Should inflation surprises on the downside occur and/or if something “breaks” in the markets, we might see actual rate hikes being less than expected, which could also be a trigger for a rebound.

There are thus several elements that could lead the market to rebound before the Fed is done with monetary policy tightening. But most of the triggers are macro-driven and imply that the peak of inflation being behind us.

Q&A #4 —

What’s your take on the French “élections legislatives” results last week-end?

Only 8 weeks after having been re-elected as President of the French Republic, Mr Emmanuel Macron has suffered a significant political setback over the weekend. The coalition of parties defending the President’s political agenda has failed to reach an absolute majority in the Parliament, unlike during Mr Macron’s first term.

This election was characterized by a very low turnout by voters who are frustrated of being trapped in a binary and nuanceless choice during the second round of the Presidential election (Macron or the Far Right).

The composition of the new French Assembly creates an unprecedented situation in France’s modern political history, in which a freshly elected president will not have a majority in Parliament to push his political agenda forward (a political dynamic that is much more prominent in the US bi-partisan political system).

The prospects for a coalition with one of the three other main blocs, the leftist coalition, the far right party or the moderate right party, are virtually nonexistent, as all of them have campaigned on their differences and opposition to the President’s agenda.

And a heteroclite coalition of minority parties to form a majority is not possible either, as it would have to cover the entire political spectrum except for the center, from the

far-left to the far-right. This is an unusual situation of political gridlock in France that raises a number of questions and uncertainties.

This situation seriously jeopardizes the domestic agenda of Mr Macron and the reforms that he presented during the presidential campaign. While punctual agreements may be found with opposition parties on specific topics, especially international or regalian matters, it seems unlikely at this stage that the Presidential party will manage to gather a majority for emblematic reforms such as pushing back the age of retirement which is currently a hotly debated topic.

As such, the reform-minded President will find himself constrained by the Parliament’s composition. France’s long-term growth prospects could therefore be negatively impacted as gridlock and inaction will only postpone and possibly compound some of the existing flaws in the economy.

However, such a gridlock scenario is not necessarily negative for the economy and financial markets in the short- run.

Parties that could have raised significant uncertainty around France’s implication in the European project are not in a position to alter the current course. They are in a position to oppose and block the President’s proposals, but unable to pass politically-tainted legislations of their own.

Indeed, the reaction on financial markets does not reflect any shock from this election for global investors. It rather reflects a justified slight increase in the risk premium attached to French assets, likely due to the uncertainty triggered by this unusual situation: CAC 40 slightly underperforming EU peers, French sovereign rates are up along with other Eurozone peers and the Euro is gaining some ground vs the US dollar.

The recent elections’ results are certainly a blow for Mr Macron and his coalition of supporters. They question the positive dynamic of the French economy’s medium and long term prospects as economic reforms, environmental policy and the social agenda are at risk of stalling. It will also be a test of the ability to compromise and build consensus for French political parties little used to the exercise.

If they rise to the challenge, the outcome could be a rejuvenation of the political life in France and possibly the basis for a more lively and solid democracy. If they fail to do so, the country might soon become ungovernable and the President might be tempted to call for new legislative elections in the hope of managing to gather a majority.

With no guarantee and the risk of an even less favorable outcome…

Q&A #5 —

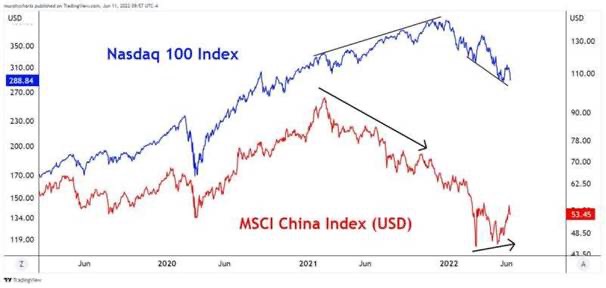

The Chinese stock market was one of the few to advance recently. What are the reasons? Is it the start of a long-term trend?

As shown on the chart below, China stock index has been diverging from the Nasdaq trend. Among the triggers for the recent outperformance:

Hopes that a pickup in fixed asset investments would put the country’s economy back on track. China’s state planner approved 10 fixed asset investments worth CNY 121 billion (USD 18.1 billion) in May, a more than six-fold jump from April.

Sentiment also received a boost after data showed surprising growth in industrial production in May and from hopes of increased policy support following weak housing market data;

News of relatively relaxed Covid-related restrictions in Beijing also lifted investors’ optimism

To our opinion, China’s landscape might remain challenging in the short term due to a confluence of risks: particularly concerns about food and energy security as the war in Ukraine lingers. Fears of a wider world war and potential issues with Taiwan are also creating concerns over investing in that region.

Nevertheless, Chinese stocks’ valuations are at their most attractive levels in a long time. Investors are encouraged by the Chinese authorities, which have recently announced concrete measures to reverse the stock market’s bearish trend and boost economic growth. They are trying to shift away from structural reforms to a genuine support of their economic growth by announcing that they will ease the “punishing” regulatory crackdowns which is a very positive sign for the tech and internet sectors. Also, interestingly, monetary policy is being eased in China this year in a context of low inflation, in stark contrast with the tightening trend at play in developed economies.

We were encouraged by all these concrete and reassuring policies which are likely to attract foreign investors back to the Chinese market, particularly through consumer-facing internet companies.

The Chinese stock market was one of the few to advance recently. What are the reasons? Is it the start of a long-term trend?

Source: Bloomberg

Q&A #6 —

Bitcoin / cryptocurrencies have been crashing this year.

We are among those who believe that there are real innovations within cryptocurrencies and blockchain. Bitcoin and other decentralized applications are among them.

However, the world of crypto-currencies is full of pitfalls as the prospects of quick gains bring out all kinds of ridiculous: from speculators of course, but also from entrepreneurs whose intention is to raise capital as quickly as possible without any real vision, technological innovation or any underlying value at all. While extraordinary profits can be made during a bull market, unimaginable losses can be made when markets turn.

The Fed’s monetary tightening has squeezed liquidity and dramatically reduced risk appetite. Cryptocurrencies is a hyper-growth segment that attracted a lot of “hot money”. Many unregulated entities took advantage of the regulatory void to build unsecure platforms and unsustainable business models. With the monetary tightening, the weakest links of financial markets are blowing up and this has been triggering massive liquidations in cryptocurrencies.

Like it is often the case in technology we will go through a Darwinian process where only the fittest will survive. More regulation is likely to come.

In the meantime, the space is likely to stay very volatile with more casualties down the road. Retail losses on cryptos might weigh on the savings of US households who left the workforce. They might now decide to reverse course and apply for jobs…

In the short-term, a bounce is likely as Bitcoin has never been this oversold.

Bitcoin / cryptocurrencies have been crashing this year.

Source: Bloomberg

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

.png)