.png)

The effect of these factors might have been exacerbated by the fact that liquidity is currently fairly low due to summer holidays but also Quantitative Tightening.

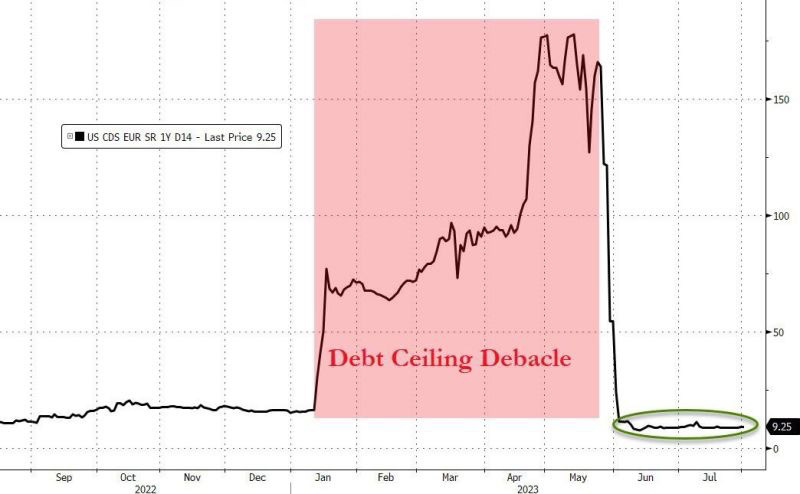

We note that US Sovereign risk (aka CDS on 1-year US Treasury) was completely unmoved by the Fitch downgrade (see chart below).

US CDS 1 year

Source: Bloomberg, www.zerohedge.com

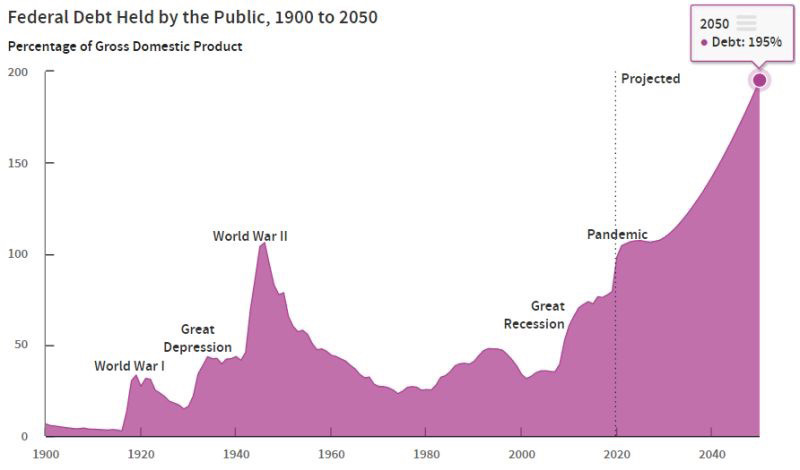

US interest expenses have surged by about 50% in the past year, to nearly $1 trillion on an annualized basis. The net interest costs is currently 3% of GDP and 14% of tax revenues (source: Strategas), a level where markets might start to anticipate a shift back to budget austerity by US policymakers.

Since the debt ceiling deal announcement, the US Treasury has been issuing more than $2 Trillion of US T-bills at a 5%+ rate to finance government operations. The Fitch rating downgrade took place a day after the US Treasury said new debt issuance would rise to US$1,007bn in 3Q23, up from US$733bn, with another US$852bn to come in 4Q23...

Could the Fed be soon forced to cut rates to help Treasury, despite the fact that inflation remains above the Fed’s target? This could lead to a crisis of confidence for the Fed by investors and trigger fears of renewed inflation.

The Fitch decision might also be used as a pressure point in the upcoming budget negotiations. Last but not least, the probability of a government shutdown this Fall is now increasing.

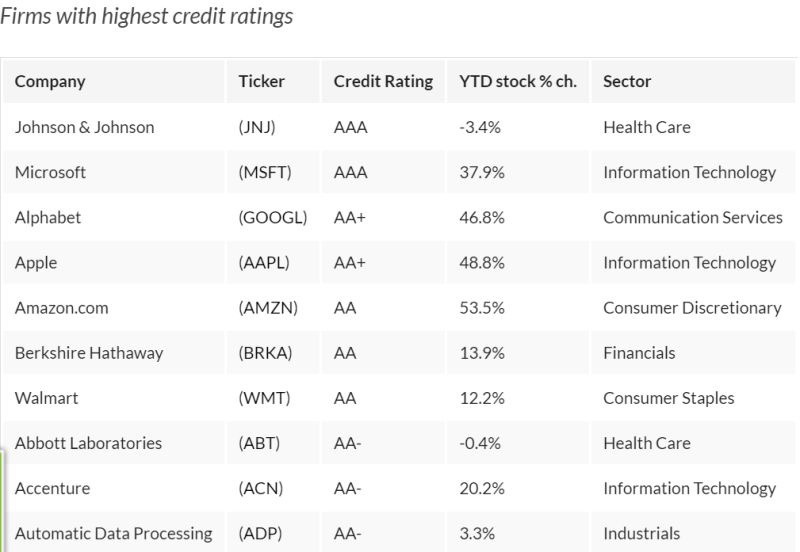

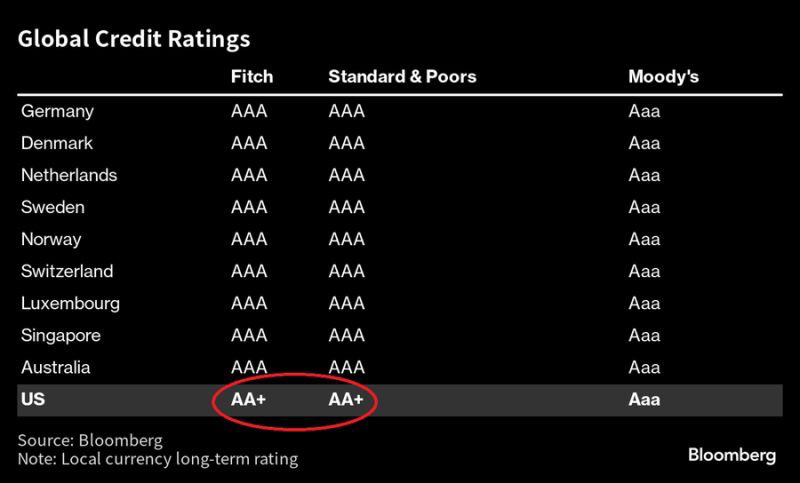

For investors willing to be invested in the AAA club (as the US is now split-rated AA+), the table below (courtesy of Jim Bianco and Bloomberg) shows the 9 sovereign issuers with Credit Ratings being triple A with the three agencies.

Within US corporate issues, just two AAA-rated companies remain in the S&P 500: Johnson & Johnson and Microsoft (see table below – source: investors). This is a startling decline in the number of AAA companies from past years.

More than 60 U.S. companies carried the coveted AAA credit rating from S&P Global Market Intelligence in 1980. And that dropped to just six in 2008. Since then,

ExxonMobil, General Electric, drugmaker Pfizer, and Automatic Data Processing have all been downgraded.