.png)

Source: Bloomberg

We are sorry that for legal reasons we are not able to help US citizens or Canadian residents other than in Ontario, Quebec, or Alberta. Best wishes for the future…

We are sorry that for legal reasons we are not able to help US citizens or Canadian residents other than in Ontario, Quebec, or Alberta. Best wishes for the future…

You chose the following profile. If you made a mistake, please change here USA

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material.

This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor.

This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other

Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

Charles-Henry Monchau

Chief Investment Officer

Charlie Munger, Warren Buffett's loyal partner, died last week. He was 99 years old. Munger helped Buffett, seven years his junior, develop the famous investment philosophy applied by the Berkshire Hathaway holding company. Under their leadership, Berkshire shares recorded an average annual gain of 20.1% between 1965 and 2021, almost twice the annualized performance of the S&P 500 index.

Source: Bloomberg

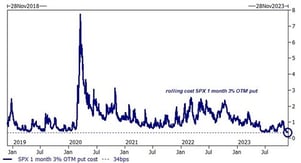

The S&P 500 index gained 8.9% in November, the 18th-highest monthly gain since 1950. At the same time, the VIX (the "fear index") fell sharply to 12, an all-time low.

As a result, the amount of insurance premiums to be paid to cover against a possible market downturn plummeted. As the chart below shows, the cost of a put option on the S&P 500 with a 1-month maturity and a 3% strike outside the currency is now 34 basis points, the cheapest in 5 years.

Source: Goldman Sachs

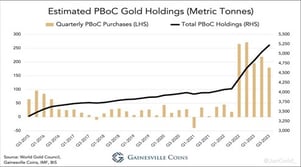

Are China's massive purchases the main reason for gold's current rise? The fact that the precious metal is trading above $2,000 an ounce, despite real interest rates being above 2% and a strong dollar, is one of the major surprises of 2023. Some analyses point to China's "massive accumulation of gold" as the reason for gold's strong performance this year. Indeed, according to unofficial accounts - such as that maintained by Gainesville Coins - total gold purchases by China's central bank (declared and undeclared) are far greater than officially disclosed. According to these studies, in the third quarter alone, China purchased 179 tonnes of physical gold. This brings the Chinese Central Bank's (PBoC) year-to-date gold purchases to 593 tonnes, or 80% more than it bought in the first three quarters of last year. Still according to these studies, China's gold holdings are estimated at 5,220 tonnes, more than double the 2,192 tonnes officially disclosed...

Source: Gainsville Coins

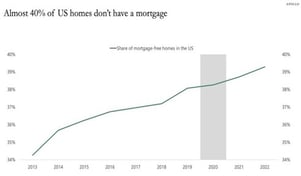

As The Kobeissi Letter points out, around 40% of American homes are currently mortgage-free. On the face of it, this sounds like good news, but it only serves to underline just how unaffordable the US housing market has become. Currently, a record 35% of transactions in the housing market are cash purchases. In other words, this market is only becoming affordable for those with the available cash. With interest rates at their highest level in 20 years, and house prices having risen by over 30% since 2020, the difficulty of accessing housing has only worsened in recent months. How much longer will US real estate prices hold up?

Source: the Kobeissi Letter

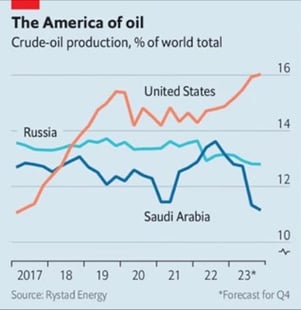

Washington is in political crisis, but that hasn't stopped the United States from continuing to increase its oil production (13 million barrels per day vs. 6 million in 2008). Natural gas production has never been so high, and natural gas prices in the USA are around 25% of those in Europe. The USA is now energy self-sufficient, and all it has to do is reindustrialize, which it is doing thanks to the CHIPS Act (to increase the rate of semiconductor production on American soil) and the IRA ("Inflation Reduction Act", which subsidizes investment in so-called responsible industrial and infrastructure projects). This subsidy for the reindustrialization of the United States has led European companies to set up factories in the United States and Mexico. The Americans are also receiving huge investments from companies in Taiwan, South Korea, Japan and elsewhere. The US is also ready to bring in talent from all over the world to rebuild its industrial base. Within a few years, Uncle Sam will have a solid industrial base powered by cheap, reliable energy. Meanwhile, Europe's de-industrialization process has been underway for many years. The Old Continent must react. And quickly.

Source: The Economist, Pinetree Macro

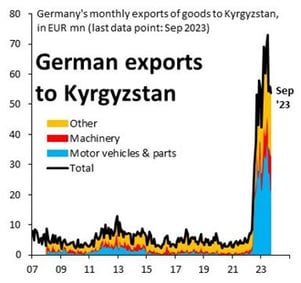

German exports of cars and spare parts (in blue) to Kyrgyzstan have risen by 5,500% since Russia invaded Ukraine. Is Kyrgyzstan suddenly experiencing a massive boom, or are these vehicles and spare parts simply transiting through Kyrgyzstan?

Kyrgyzstan is a country in Central Asia. Extremely mountainous and originally populated by nomadic peoples, this former USSR republic gained its independence when the USSR collapsed in 1991. Kyrgyzstan has less than 7 million inhabitants and a per capita GDP of $2,260 a year.

Source: : Robin Brooks

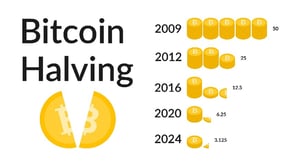

Halving is an event that occurs on the Bitcoin blockchain. It involves a halving of the reward for block mining. This event occurs approximately every four years and is a form of artificial inflation control, similar to a central bank printing less money. The last halving took place on May 11, 2020, resulting in a reward of 6.25 bitcoins (BTC) for each block successfully mined. The next halving is scheduled for early-mid 2024, when the reward for each block will be reduced to 3.125 BTC. The total number of bitcoins in circulation will reach the theoretical maximum of 21 million after the last halving, scheduled for around 2140.

By April 2024, 97% of all bitcoins will have been created. Halving the rewards every four years ensures that the total supply of bitcoins is capped, making it a deflationary asset. In other words, the more time passes, the fewer bitcoins are created. All other existing fiat currencies are inflationary by nature. The more time passes, the more central banks print, making the currency you hold less valuable. This is what differentiates bitcoin from all other currencies, and why many believe it to be a digital store of value (like gold, which has a finite supply).

Source: Deltec Bank & Trust

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

Meanwhile, Wall Street's long-term earnings expectations for the S&P 500 are now at record levels. Each week, the Syz investment team takes you through the last seven days in seven charts.

Meanwhile, corporate leadership is evolving rapidly: only 135 of the S&P 500 constituents from 1996 are still in the index today, while the EU goods trade deficit with China is close to a record €376bn. Each week, the Syz investment team takes you through the last seven days in seven charts.

Meanwhile, Trump’s personal crypto earnings in 2025 topped the combined profits of every publicly listed US crypto company. Each week, the Syz investment team takes you through the last seven days in seven charts.

Live feeds, charts, breaking stories, all day long.

Our latest research, commentary and market outlooks