.png)

Charles-Henry Monchau

Chief Investment Officer

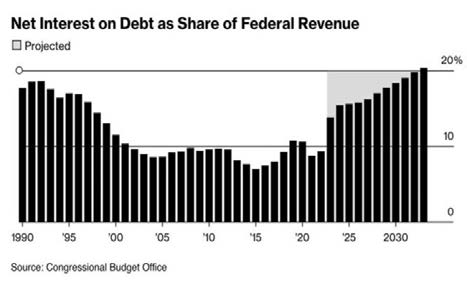

For nearly 20 years, it was effectively free for the US to issue debt as debt service costs were ~1.5%. Now, debt service costs have doubled to 3% and will rise toward 5% as rates skyrocket.

To put this in perspective, 5% on $33 trillion is ~$1.7 trillion per year on interest expense. As deficit spending rises, so are rates, as the US issues trillions in bonds to cover the deficit. It's a never-ending cycle of borrowing to spend which is driving rates higher and leading to interest expense being 20% of US revenue.

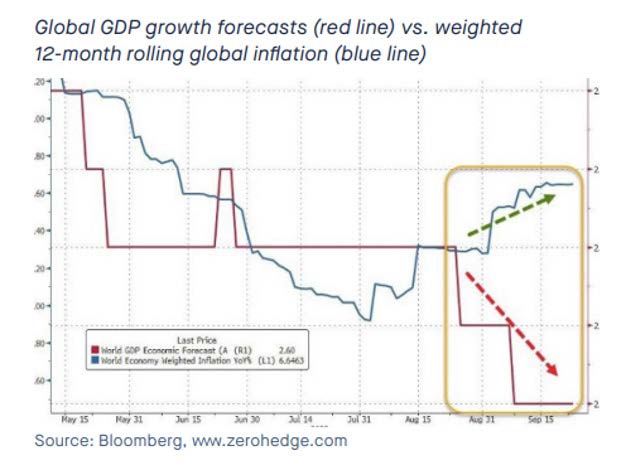

The market has de facto revised the path of interest rates upwards: the Fed's futures contracts no longer point to rate cuts before September 2024. To put things in perspective, three months ago, the futures contracts were forecasting 4 rate cuts in 2023. Today, the market expects interest rates to pause for at least a year.

Source: The New York Times

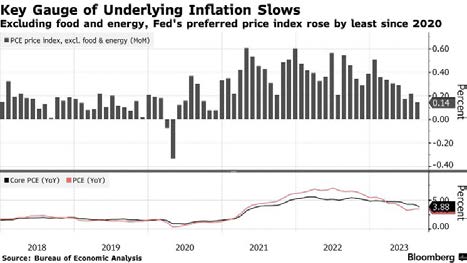

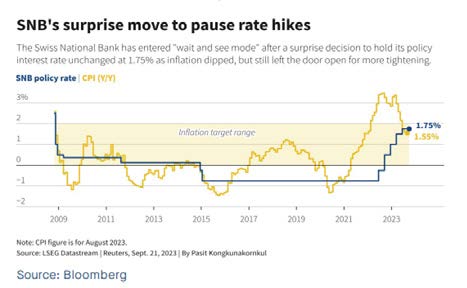

Indeed, Mrs. Lagarde and Mr. Powell left an impression of great confusion. On the one hand, they were obliged to acknowledge that the battle against inflation was not yet won. On the other, they shared their fears about the impact of higher rates on the economic cycle. In the case of the SNB, things are much clearer. Inflation is already within the SNB's target range. Activity is slowing down. These two factors allow the SNB to come up with a clear and unambiguous decision: the end of rate hikes for this cycle. And if economic activity were to accelerate or slow too much, the SNB has several options available.

A sell-off in global bond markets was partly to blame for the pressure on risk assets, with the global aggregate bond benchmark falling by -3.6% in the third quarter. The US Treasury market was a notable laggard, while in credit, the lower interest rate sensitivity of high yield bond benchmarks helped both the US and European high yield bond markets to eke out positive returns, returning 0.5% and 1.5% respectively. On a year-to-date basis, the global aggregate bond index is down -2.2%.

We note that correlation between bonds and stocks spiked in the 3rd quarter, echoing the market dynamics of 2022.

Source: Bloomberg

Source: FT