.png)

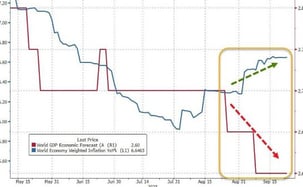

Global GDP growth forecasts (red line) vs. weighted 12-month rolling global inflation (blue line)

source: Bloomberg, www.zerohedge.com

Charles-Henry Monchau

Chief Investment Officer

Global GDP growth forecasts (red line) vs. weighted 12-month rolling global inflation (blue line)

source: Bloomberg, www.zerohedge.com

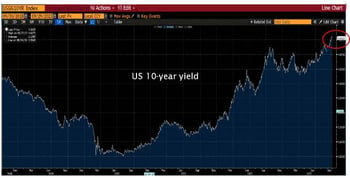

In addition, strong bond issuance by the US Treasury at a time when the Federal Reserve is accelerating the reduction in the size of its balance sheet through Quantitative Tightening (QT) is creating unfavourable supply/demand conditions for long-dated bonds. This upward movement in bond yields is contributing to the rise in the dollar and weighing on equity valuations, particularly those of so-called growth stocks (e.g. Technology).

Yield to maturity on 10-year US Treasury bonds (last 5 years)

Source: Bloomberg

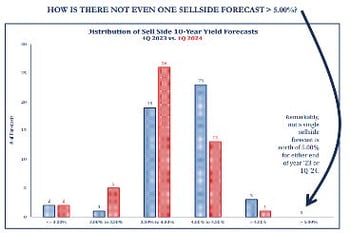

Analysts' forecasts for the yield on 10-year US Treasury notes - Q4 2023 vs. Q1 2024

Source: Strategas

Prices (red line) versus assets under management (white line)

Source: Bloomberg, Crescat Capital

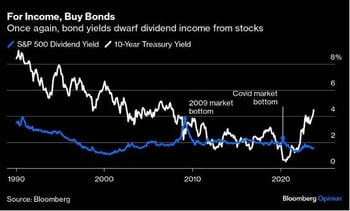

Bond yields are now well above the S&P 500 dividend yield

Source: Bloomberg

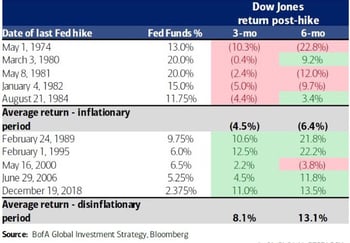

How will the Dow Jones perform after the Fed's latest rate hike?

Source: BofA Global Investment Strategy, Bloomberg

Share of Payments via SWIFT in EUR (%)

Source: Bloomberg