.png)

source: Barchart

Charles-Henry Monchau

Chief Investment Officer

source: Barchart

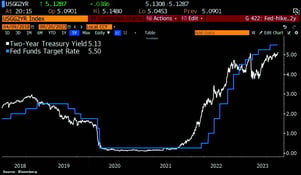

The market has de facto revised the path of interest rates upwards: the Fed's futures contracts no longer point to rate cuts before September 2024. To put things in perspective, three months ago, the futures contracts were forecasting 4 rate cuts in 2023. Today, the market expects interest rates to pause for at least a year.

Source: Bloomberg

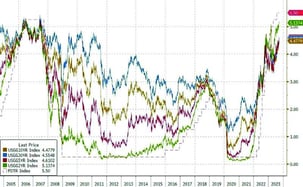

Source: www.zerohedge.com, Bloomberg

Source: Charlie Bilello

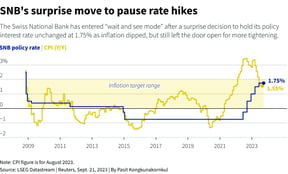

It is also interesting to compare the SNB's decision and body language with those of the Fed and the ECB. Indeed, Mrs. Lagarde and Mr. Powell left an impression of great confusion. On the one hand, they were obliged to acknowledge that the battle against inflation was not yet won. On the other, they shared their fears about the impact of higher rates on the economic cycle. In the case of the SNB, things are much clearer. Inflation is already within the SNB's target range. Activity is slowing down. These two factors allow the SNB to come up with a clear and unambiguous decision: the end of rate hikes for this cycle. And if economic activity were to accelerate or slow too much, the SNB has several options available.

Source: Bloomberg

Source: Charles Schwab, Bloomberg

Source: App Economy Insights