.png)

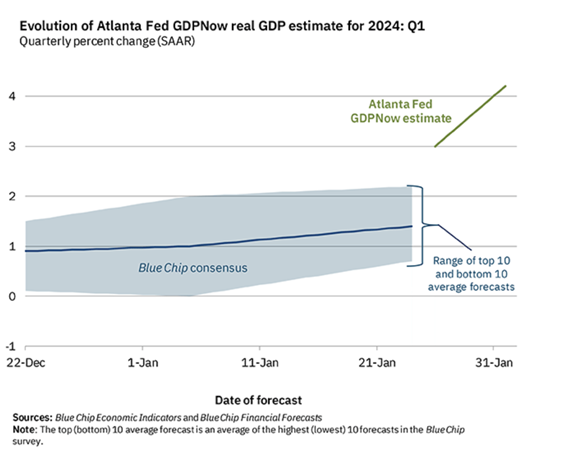

Source: Blue Chip Economic Indicators and Blue Chip Financial Forecasts

We are sorry that for legal reasons we are not able to help US citizens or Canadian residents other than in Ontario, Quebec, or Alberta. Best wishes for the future…

We are sorry that for legal reasons we are not able to help US citizens or Canadian residents other than in Ontario, Quebec, or Alberta. Best wishes for the future…

You chose the following profile. If you made a mistake, please change here USA

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material.

This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor.

This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other

Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

Charles-Henry Monchau

Chief Investment Officer

US economic surprises keep surprising on the upside, following a series of data releases last month highlighting the continued resilience of the US economy. Firstly, there was a solid employment report, with 216k jobs adding to the economy in December, as well as steadier wage growth and an unemployment rate holding firm at 3.7%.

Further into the month, fourth-quarter GDP of 3.3% annualized was significantly ahead of consensus expectations. The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2024 is 4.2 percent

Source: Blue Chip Economic Indicators and Blue Chip Financial Forecasts

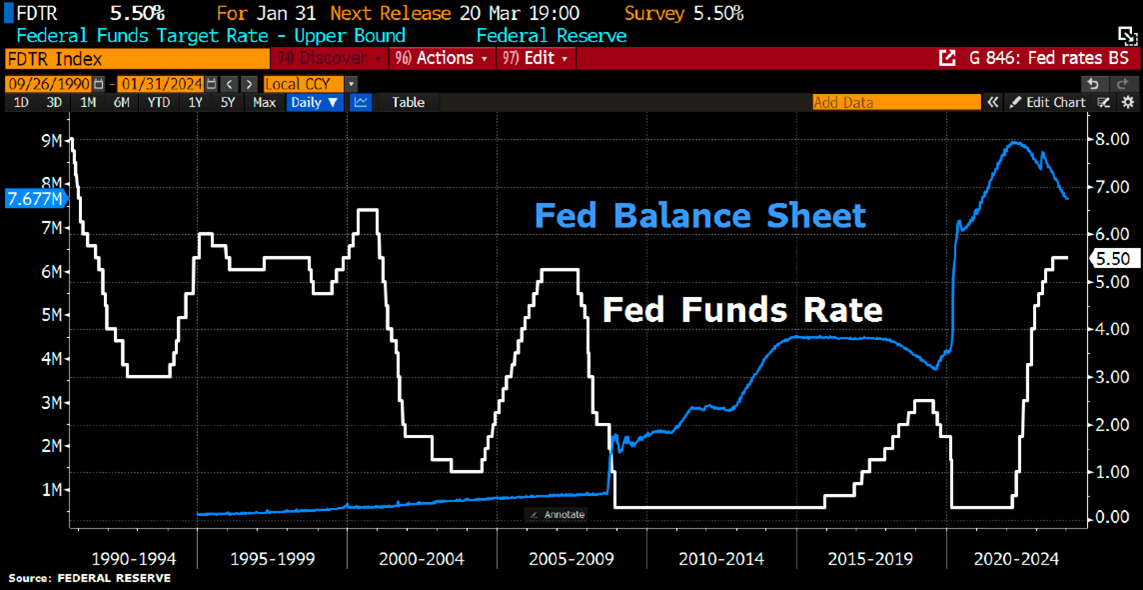

As expected, the Fed kept its policy rate unchanged in January, but the market's focus was mainly centered on future meetings, seeking any signals around when a rate cut may come (markets have been pricing in a cut as early as March).

The Fed did NOT give the market what it was hoping for, instead emphasising that it plans to wait a while longer to build greater confidence that inflation will remain on its current, descending path.

This was the right move, in our opinion. Cutting prematurely runs the risk of having to backtrack if inflation were to perk up again, an outcome that would be far more detrimental to the markets than staying on hold a little longer.

The Fed said that a March rate cut is "unlikely," yet futures are still pricing in a 36% chance it happens. Even as the Fed said they cannot cut rates until inflation is comfortably moving to 2%, markets still see 6 cuts in 2024. There's even a growing 23% chance of 7 interest rate cuts this year. Markets are pricing in a rate cut at EVERY remaining Fed meeting this year.

Source: Bloomberg

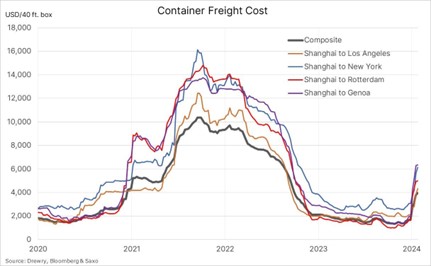

Another important story for January 2024 was geopolitics, as the strikes from the Houthi rebels on commercial shipping in the Red Sea implied significant supply-chain disruption.

Against that backdrop, freight costs have spiked again, Drewry’s World Container Index is up to $3,824 per 40ft container as of 01 February. That’s almost triple its levels from October 2023, when costs were at a post-pandemic low.

Source: Drewry

In January 2024, risk assets were well supported, given the economic data that encouraged optimism about a "soft landing". Global equities moved mostly higher in January 2024, with the S&P 500 (+1.7%) and the European STOXX 600 (+1.5%).

The geopolitical backdrop led to a rise in oil prices after three consecutive monthly declines, with Brent Crude (+6.1%) and WTI (+5.9%) both recording gains in January 2024.

The dollar index rallied by +1.9% in January, after falling behind in previous months, as the US dollar strengthened against all other G10 currencies. It was a disappointing month for EM assets, as the MSCI EM index falling by -4.6%.

When compared to the relatively dull performance of their value counterparts (+0.3%), Growth stocks are the strongest outperformers, delivering 2.1% over the month. Developed market equities rose by 1.2%, whereas emerging market equities fell by 4.6%, regardless of the latest stimulus measures announced by the People's Bank of China (PBOC).

Source: JP Morgan

In the US, the S&P 500 index was driven to record levels in early January, as bullish expectations of a soft-landing scenario carried on the "Magnificent Seven" rally. The 7-stock basket reached new highs, but the 7 is now 6... as the $TSLA heads in the opposite direction.

The TOPIX index was the best performing of the major stock markets in January, rising by 7.8% over the month, building on last year's strong performance. Unexpected weakness in wages, coupled with uncertainty over the economic impact of the New Year's earthquake, prompted markets to re-evaluate the likely removal of the negative interest rate policy (NIRP) in the short term.

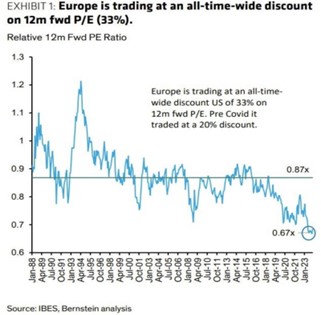

The MSCI Europe ex-UK index recorded a positive return (+2.1%) in January. The Euro Stoxx 50 index achieved its highest level in 20 years. It is worth noting that European equities are currently trading at their lowest valuation in history, relative to US equities.

Source: IBES, Bernstein analysis

The Chinese domestic economy continued to struggle, with disappointing retail sales and further deterioration in housing activity. Fourth-quarter GDP rose by 5.2% year-on-year, in line with predictions but remaining historically weak. Whilst the PBOC announced several stimulus measures, it was not the political "bazooka" the markets had hoped for to boost activity. Continued concerns about China's economic outlook probably contributed to the poor performance of the MSCI Asia ex-Japan Index and the MSCI Emerging Markets Index, which fell by 5.4% and 4.6% respectively over the month.

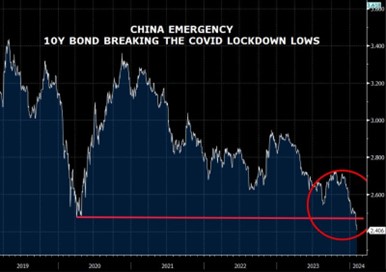

China 10Y yield moved below 2.47%, breaking Covid19 lockdown lows. With local equity market imploding and real estate in freefall, fears of a Japanese style deflationary spiral are growing. Should China devalue the renminbi?

Source: Bloomberg

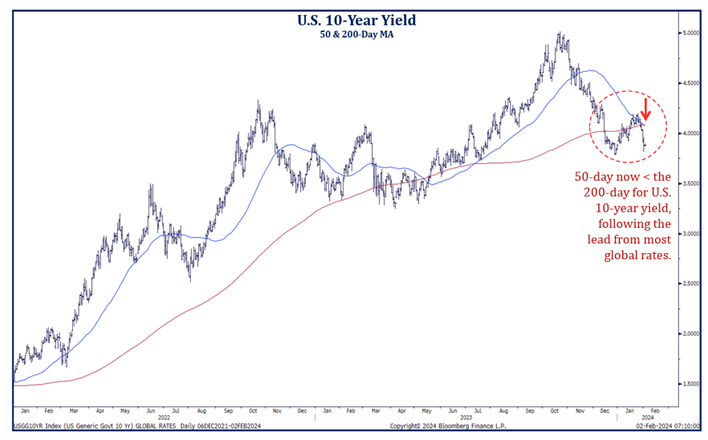

As investors grew less optimistic that central banks would cut rates in the first quarter, sovereign bonds lost ground. US Treasuries closed the month down -0.2%, and European sovereign bonds were down -0.6%. Still, despite the Fed being on hold and strong US economic data the trend seems to be for lower 10-year yield as the 50-day moving average is now below the 200-day.

In credit, the European high-yield bond market stood out with positive returns (0.9%), on the other hand, its US counterpart posted stagnant returns over the month. Global investment-grade credit, meanwhile, recorded negative returns in January, despite the tightening of spreads. The appreciation of the US dollar weighed on emerging market debt, which declined by 1.2% over the month.

Source: Strategas

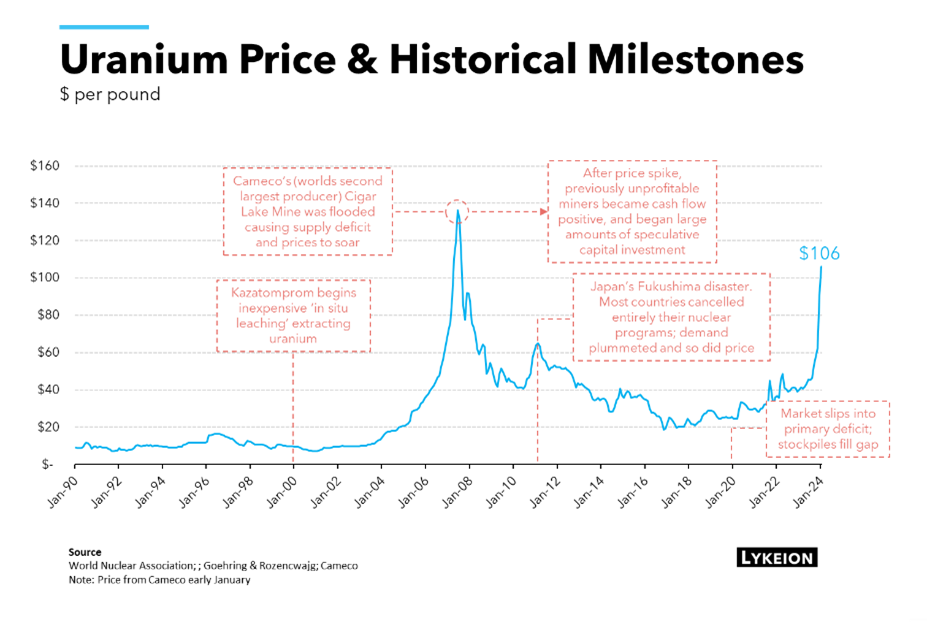

Uranium jumps back to its highest price in almost 17 years due to expectations of rising demand from nuclear plants. Indeed, most of the world's governments are stepping up their plans to increase nuclear power generation and, in the case of the 22 members of the COP28 agreement, to triple their capacity by 2050.

This move, which includes China's current 55 reactors, the 22 under construction and another 70 in planning phase, is already coming up against real physical constraints on the uranium fuel market. New supply levels have been non-existent over the past decade, following the Fukushima accident, and current mine supply is not only insufficient to meet current demand, but uranium stocks have been largely drained. To make matters worse, last month the world's largest uranium miner, Kazatomprom, announced that production targets would not be met due to construction delays and "difficulties related to the availability of sulfuric acid".a crucial ingredient in a mining technique known as "in situ leaching".

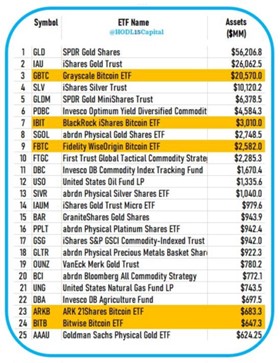

Here we go! After years of waiting, the Securities Exchange Commission (SEC) in the USA and its chairman Gary Gensler have finally relented. On Wednesday January 10, they approved the first Bitcoin spot ETFs. More than three years elapsed between this approval and that of the first Bitcoin futures ETFs (based on dollar-settled futures contracts).

In just 15 trading days, the new Bitcoin ETFs have made the commodities ETF leaderboard. $IBIT is #7, $FBTC #9, $ARKB and $BITB #23 & #24.

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

Live feeds, charts, breaking stories, all day long.

Our latest research, commentary and market outlooks