.png)

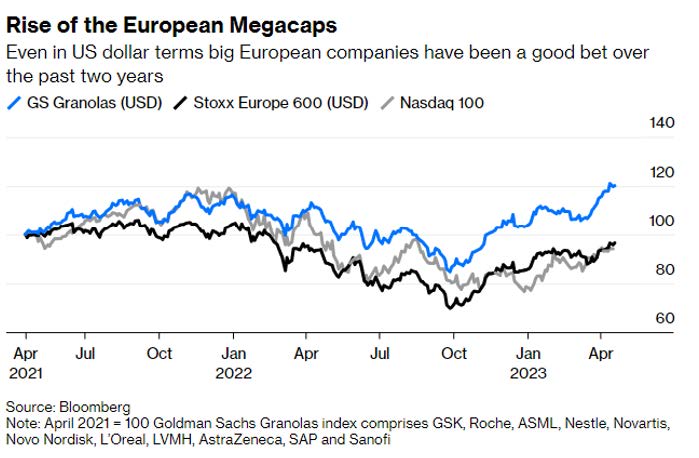

The great "Granolas" companies

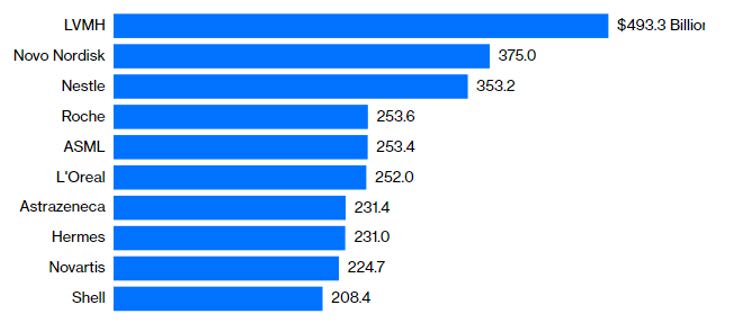

Three years later, the ranking of the largest capitalizations has changed somewhat. GlaxoSmithKline, Sanofi and SAP have dropped out of the Top 10, while Hermès and Shell have entered.

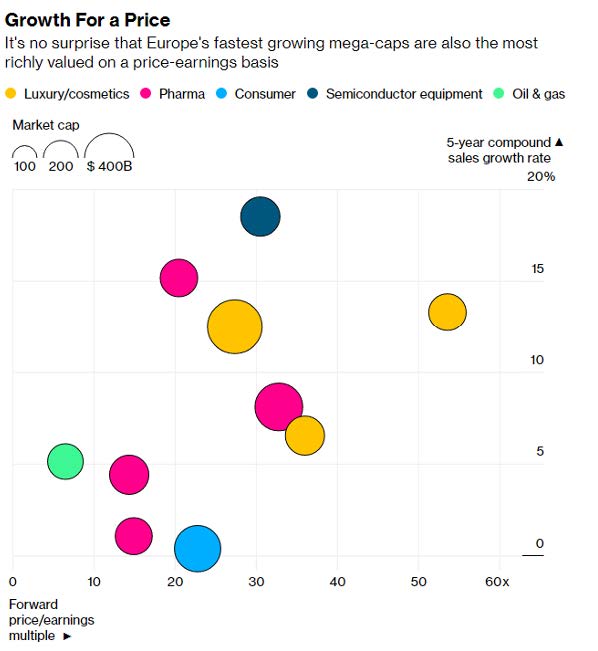

But the characteristics of these stocks remain the same: strong balance sheets, strong earnings growth that is not sensitive to the economic cycle and high dividend yields. Unlike the US, Europe is not dominated by technology. Instead, the luxury, healthcare and consumer sectors account for the lion's share of the Top 10.

For the first time in history, a European company has seen its market capitalization exceed 400 billion euros: LVMH Moet Hennessy Louis Vuitton SE, whose operating profit reached 21 billion euros in 2022. The other GRANOLAS are not so far behind: the Danish pharmaceutical company Novo Nordisk A/S has reached a capitalization close to 350 billion euros, while the Dutch semiconductor equipment company ASML NV is worth 230 billion euros. Ten European companies now have a market capitalization of more than $200 billion, crossing the threshold of "megacapitalization. Ten years ago, there were only three.