.png)

As a reminder, U.S. commercial real estate is a very broad asset class, encompassing offices, retail space, industrial facilities, multi-family residential units and shopping centers. The commercial real estate market plays a vital role in the U.S. economy, supporting over 7 million jobs and contributing nearly $1,000 billion to U.S. GDP. It also generates significant tax revenues for local and state governments. Additionally, the value of real estate assets influences the overall wealth and financial stability of individuals, businesses, and institutional investors.

The Big short 1.0

During the US housing collapse of 2007/2008, some high-profile investors, such as John Paulson and Michael Burry, made huge profits by shorting residential mortgage-backed securities (RMBS) or buying ABX CDS on various subprime residential and commercial mortgage-backed securities. Their financial success was portrayed by Christian Bale in the film "The Big Short" (2015).

The Big Short 3.0

After the residential sector (Big Short 1.0) and malls (Big Short 2.0), version 3.0 focuses primarily on offices. To short a specific segment of commercial real estate, you need to short a dedicated index. For malls, it is the CMBX 6 index. For hotels, the benchmark index is CMBX 9. For offices, a Goldman Sachs note cites the CMBX 15 index, which has a 33% exposure to the office sector. To be precise, the investment bank highlights the BBB- tranche, which is the one with the highest convexity to underlying price variations.

Sector exposure of the various US real estate mortgage indices. CMBX 15 has relatively high exposure to offices and low exposure to hotels and retail.

Source: Intex, Goldman Sachs Global Investment Research

Note that the CMBX 15 BBB- index is currently trading close to its lowest level since its inception.

Bloomberg CMBX 15 BBB-

Source: Bloomberg

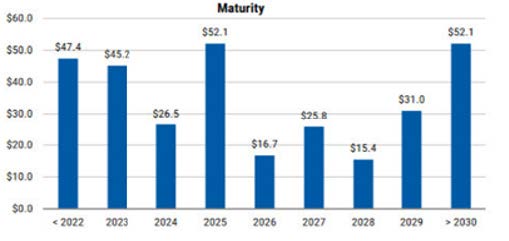

CMBS repayments by maturity (in billions of dollars)

Source : Trepp, Morgan Stanley Research

Most CMBX indices are currently falling at a rate not seen since the COVID crash or the Lehman bankruptcy. Vornado Realty, a real estate trust (REIT), is now trading at its lowest level since 1996. The stock has fallen from $66 in January 2020 to less than $16 in June 2023.

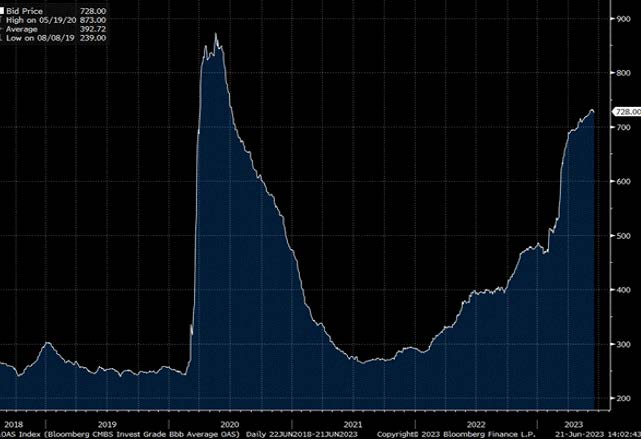

Meanwhile, yield spreads (OAS for "Option adjusted spreads") on BBB- CMBSs versus US Treasury yields have begun to diverge significantly. Widening OAS spreads are indicative of increased risk as perceived by the market, signaling concerns about tenant creditworthiness, vacancy rates and potential declines in property values. Investors and creditors keep a close eye on OAS spreads, as they reflect market sentiment and influence financing conditions for office building acquisitions and refinancings.

Bloomberg CMBS BBB OAS

Source : Bloomberg

The impact of Big Short 3.0 on the financial industry

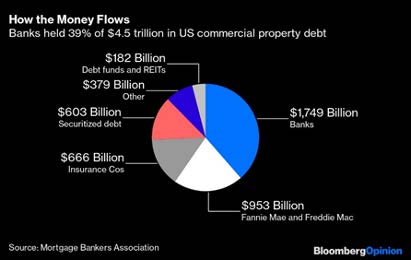

Banks are heavily involved in the financing of commercial real estate, including loans for the acquisition of office buildings. It is estimated that banks hold around 39% of the $4.5 trillion in commercial real estate debt, leaving them vulnerable when default rates start to rise.

Who holds US commercial real estate debt?

Source : Bloomberg

Declining property values and increasing vacancies could lead to a reduction in the collateral value used for office loans. This could result in higher default rates and potential losses for banks. Non-performing loans and foreclosures in the office real estate sector could have a negative impact on banks' asset quality, profitability and capital adequacy ratios, jeopardizing the financial stability of weaker players.

Smaller regional banks are more exposed to commercial real estate risks, as they concentrate their lending on this category. Two-thirds of their loan book is concentrated on commercial property, compared with one-third on residential. In contrast, the major banks have a much more diversified loan portfolio.

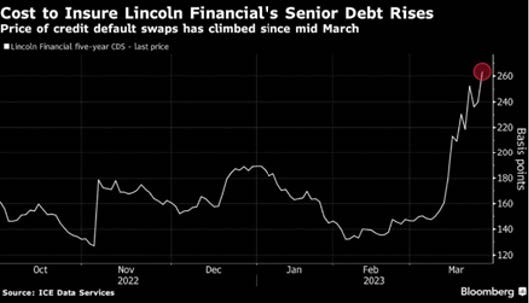

Insurance companies also have significant exposure to US real estate debt, with $666 billion of exposure to commercial real estate. An example of stress linked to this sector's exposure to real estate: the cost of insuring the senior debt of Lincoln Financials, an insurance company, has recently risen sharply (see chart below).

CDS on Lincoln Financials senior debt

Source: Bloomberg

Finally, shadow banks - financial institutions without a banking license and therefore less subject to strict financial regulations - are also exposed, in amounts that are difficult to estimate