.png)

The bond market is experiencing one of its worst years in its history. The market value of global bonds has fallen from $69 trillion to $55 trillion since the July 2021 highs. The bear market is also affecting sovereign debt, a market segment where one of the main buyers in recent years has undoubtedly been central banks. According to the Financial Times, central banks have accumulated more than $30 trillion in bonds over the past decade.

With bond yields rising sharply, many economists fear that central banks will have to absorb huge losses, resulting in negative equity that could undermine their efficiency and eventually bankrupt them.

The Fed's balance sheet and profit and loss account since 2008

In the case of a commercial bank (or any other business), having fewer assets than liabilities can lead to insolvency. In many countries, it is illegal to do business while insolvent, as you are committing a kind of fraud on anyone who owes you money, since there is a significant risk that the bank or company in question will not be able to repay its debts.

Like commercial banks, central banks have a balance sheet and their liabilities can theoretically be greater than their assets on the balance sheet. As shown in the chart below, the US Federal Reserve's capital seems relatively small compared to total assets (less than 0.5% or 200 times leverage). It is this capital that theoretically allows for the absorption of potential losses.

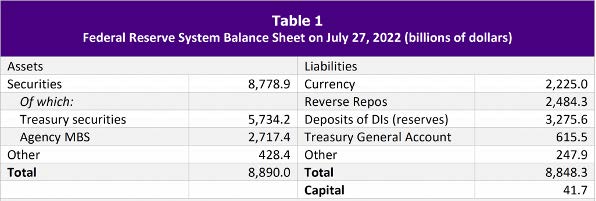

Fed Balance Sheet as of July 27, 2022

Source: Federal Reserve Statistical Release H.4.1

Although the Fed's capital has historically been low (less than 5% of liabilities), years of quantitative easing (QE) have changed the structure of the US central bank's balance sheet. Before QE, the Fed issued money for free and bought securities paying interest, allowing it to accumulate profits and create reserves. But QE brought two important changes: 1) the Fed continues to accumulate securities, but these purchases are financed by very large reserves held by commercial banks; 2) the Fed pays interest on the reserves.

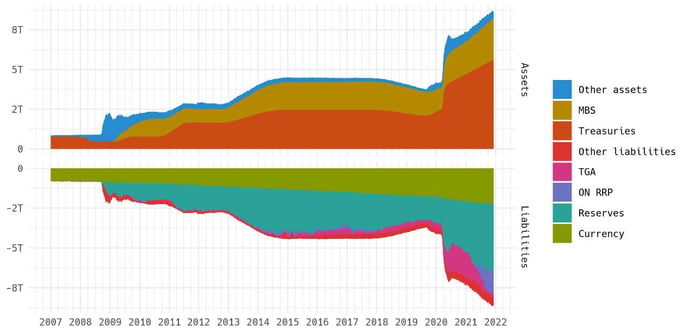

Since 2008, the Fed's balance sheet has expanded at a record pace, peaking at nearly $9 trillion (see chart below). On the asset side, the securities held are mainly treasury bills and mortgage debt. On the liabilities side, the reserves on which the Fed pays interest now account for nearly two-thirds of the balance sheet.

Fed balance sheet since 2007

Source: H.4.1, FRED and neilson.substack.com

Source: H.4.1, FRED and neilson.substack.com

The Fed, like other central banks, is expected to generate structural revenues - called seigniorage - that somehow guarantee its long-term profitability and capital strength. It is this structural income that allows central banks not to face the same capital reserve requirements as commercial banks.

In the case of the Fed, the securities accumulated since 2008 on the asset side have generated relatively low yields, but still slightly higher than the interest paid on the reserves, which has allowed it to generate profits (distributed to the U.S. Treasury) and to keep its equity in positive territory. Before the great financial crisis of 2008, these profit distributions amounted to 20-25 billion per year. With the expansion of the balance sheet, these annual profits have reached about 100 billion.

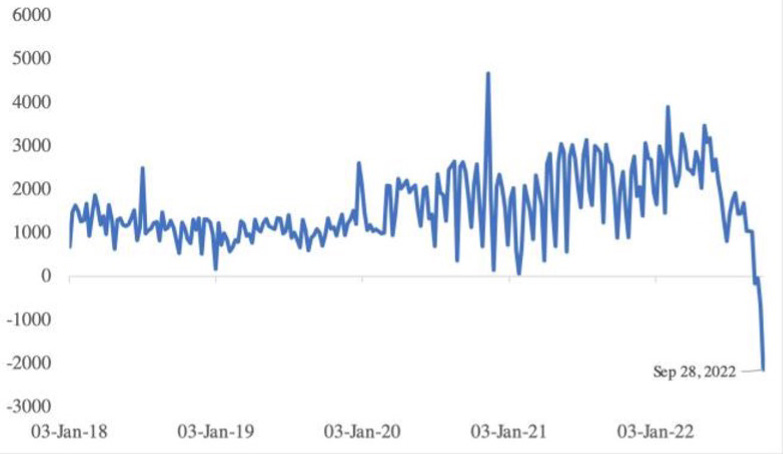

But with the sharp rise in bond and mortgage yields (and hence the decline in the market value of these bonds), the assets side of the balance sheet is now recording substantial (but unrealized) losses. On the liability side, interest on reserves to be paid to commercial banks has increased as a result of rising short-term rates. As the chart below shows, the Fed's profit and loss account has recently moved into the red. According to the Financial Times, the Fed accumulated losses of nearly $720 billion in the first half of the year. These losses continue to worsen and could theoretically push the Fed's equity into negative territory (even though the Fed is not required to record P&Ls until they are realized).

Earnings remittances due the US Treasury (EOP. $ million)

Source: Federal Reserve Board, Haver Analytics

This situation is relatively similar for other major central banks in the developed world. According to the FT, the Bank of England incurred a loss of £200 billion at the end of the second quarter.

Is there a risk that the Fed or other major central banks will go bust?

Why a central bank cannot (theoretically) go bankrupt

First, it should be remembered that a bank or any other type of business can continue to operate even with negative equity as long as it is able to meet its daily cash flow needs. The standard insolvency test as mentioned above applies to the balance sheet at a given time. What matters for day-to-day viability is the flow of income and expenses. Thus, a company that has net liabilities (i.e., negative equity) can continue to operate if it has sufficient cash to pay its day-to-day costs. At some point, if the balance sheet numbers have been correctly calculated, this capacity will run out, but perhaps not for some time.

The case of central banks is very special. Central banks finance themselves in a completely different way than commercial banks and private companies, because their liabilities - bank bills and commercial bank deposits - are the only forms of payment allowed in their jurisdiction. Central banks therefore have a monopoly on money creation. In other words, they are always able to honor their financial commitments: to settle their debts, all they have to do is create money, which they can do at will, instantaneously and at virtually no cost (the interest paid on deposits remains - for the moment - low and the cost of printing banknotes is negligible). An agility that reminds us of a well-known board game...

As explained by Société Générale, the ability to create money to pay debts has three fundamental consequences for central banks:

-

They can lose money to the point of having negative equity (capital) without this being a problem for the entities from which they borrowed money;

-

Since they do not face the risk of banking panic that commercial banks do, they can continue to operate normally even with negative capital;

-

In the event of a balance sheet deterioration, they are therefore not subject to reorganization or liquidation requirements.

An interesting example is the Czech National Bank (CNB). CNB's equity has been in negative territory for most of the last 20 years. The Czech Republic has a relatively small but outward-looking economy, which means that the exchange rate has to be competitive. Most of the assets held on the balance sheet are denominated in foreign currencies. When the Czech koruna rises, the value of its assets falls, resulting in a negative profit and loss account and consequently a negative equity. The same is true for the Swiss National Bank, whose profits and losses have fluctuated by billions in some years, without losing control of its monetary policy.

Risks related to the persistence of negative equity

The above postulate is not necessarily applicable in the case where a central bank has to honour its debts in a foreign currency. In the past, central banks of emerging countries have found themselves in difficulty in paying their foreign debts. The strength of the dollar could therefore be a danger for some of them.

On the other hand, the ability of a central bank to operate normally even with negative capital is only valid if it remains credible in the eyes of financial markets and the banking system.

One can therefore imagine a scenario where, as the negative capital situation is prolonged over time, its level would limit the central bank's long-term profitability and become insufficient to offset current expenses. Such a scenario would force the central bank to create money to cover its expenses, which would affect and disrupt its monetary policy.

Another risk to consider is that of government interference. In the event of a prolonged period of losses on the part of the central bank, it is easy to imagine members of parliament demanding a change in monetary policy that would de facto damage the credibility and independence of the central bank. And possibly at the worst possible time...