.png)

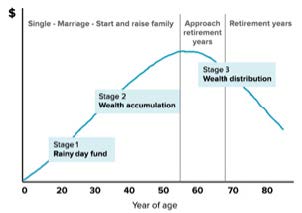

Investors’ financial priorities change they move through the various stages of life. Baby boomers have reached the stage where priority is given to planning for a comfortable retirement. For Generation Xers, the priority is to accumulate wealth in order to finance their children's education and meet their various financial responsibilities. As for millennials and generation Z, they are in the ascending phase of their financial life cycle; they are concentrating on their professional career development and building a solid financial base.

An individual's financial life cycle (ages are averages)

Source Image : Stockspot

Generation X, in particular, is expected to experience substantial asset growth. According to a Deloitte study, their assets could almost quadruple to $22 trillion by 2030. However, this generation faces unique challenges. It is referred to as a 'sandwich generation', juggling the financial obligations of caring for ageing parents with the needs of children.

The financial setbacks suffered by Generation X during the great financial crisis (2008) have had an impact on their appetite for risk. They tend to be both cautious and independent investors, showing a degree of skepticism towards the unpredictability of the market.

Millennials, a generation that numbers around 1.8 billion worldwide, are expected to exert a substantial financial influence. UBS estimates that the wealth of millennials

will grow five times faster than that of baby boomers. Projections indicate that by 2030, they could control $20 trillion.

Until now, millennials have been somewhat hesitant when it comes to investing in the stock market. This reluctance is not surprising, given that many of them graduated from university and entered the world of work during the difficult period of the Great Recession. The S&P 500 had lost 57% of its value by the time the oldest millennials were in their twenties. Debt also plays a role; in the US, the 25-34 age group has already accumulated an average debt of $40,000 per person (source: Business Insider).

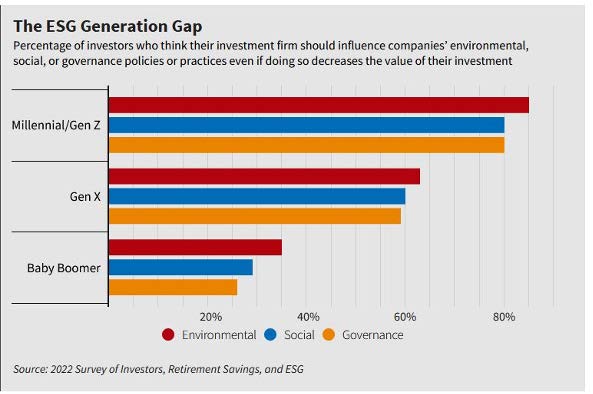

Millennials, known for their ethically based financial decisions, have significantly influenced the growth of sustainable and impact investing over the past decade. Industry reports indicate that millennials are the largest generation of investors in sustainably managed investment funds

Source Image : Forbes