.png)

What we learnt?

While the official statement was in line with market expectations, the press conference was much more hawkish than expected. European Central Bank (ECB) Governor Christine Lagarde is clearly showing signs of stress (or pressure from Germany? other Central Bank peers?) regarding European inflation. She said the risks are on the upside for the next few months - a “unanimous concern” among ECB members.

European inflation, which exceeded 5% in January, is likely to continue to be above the ECB’s 2% target for some time, driven mainly by commodities (the Russia-Ukraine conflict is not helping) and supply shocks, exacerbated by Omicron’s potential impact, however small, on China’s supply chains.

Christine Lagarde has set the stage for a significant shift in March. It could be seen as a pivot in ECB monetary policy. She also indicated that:

- PEPP (Pandemic Emerging Purchase Program) will end in March 2022;

- APP (Asset Purchase Program) will partially offset the end of PEPP through 40 billion euros a month in 2Q22, 30 billion euros a month in 3Q22 and 20 billion euros a month thereafter;

- It is not prudent to exclude a 2022 rate hike (10basis points?);

- The end of APP net buying in 3Q22 is possible.

ECB quantitative tightening schedule

Source: Bank Syz, Bloomberg

What are interest rates signaling?

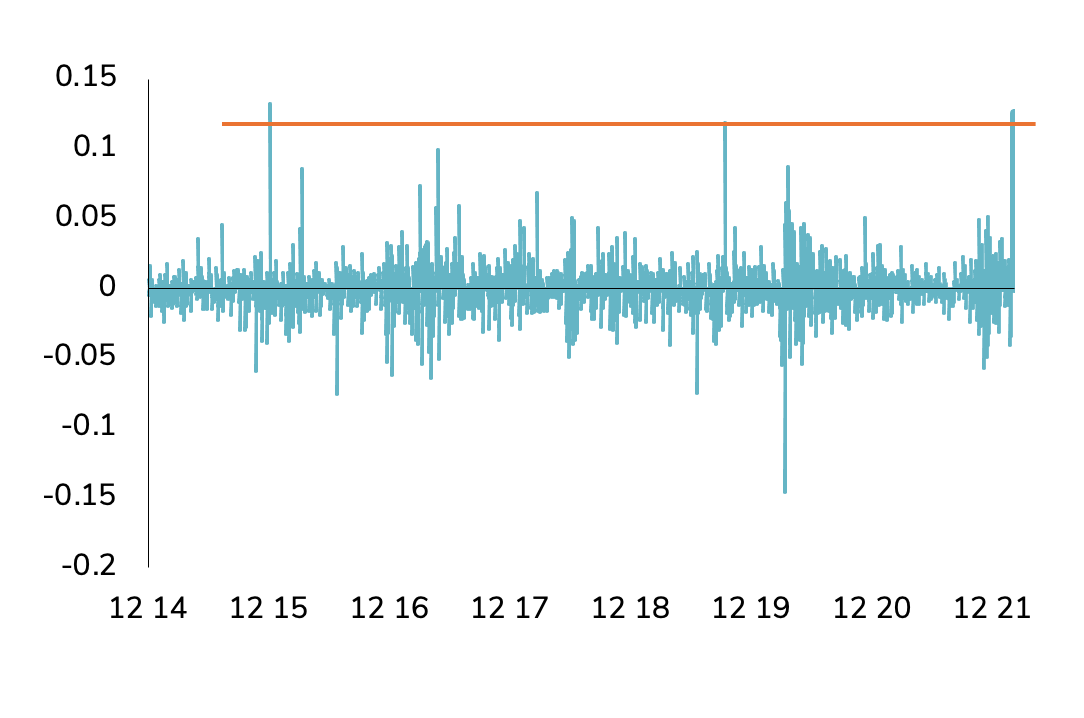

The front-end of the German Treasury yield curve rose sharply: the German 2-year yield saw its largest increase since December 3, 2015 (and a less dovish ECB than market expected), jumping 13 basis points in a single day.

German treasury 2-year yield net change (daily)

Source: Bank Syz, Bloomberg

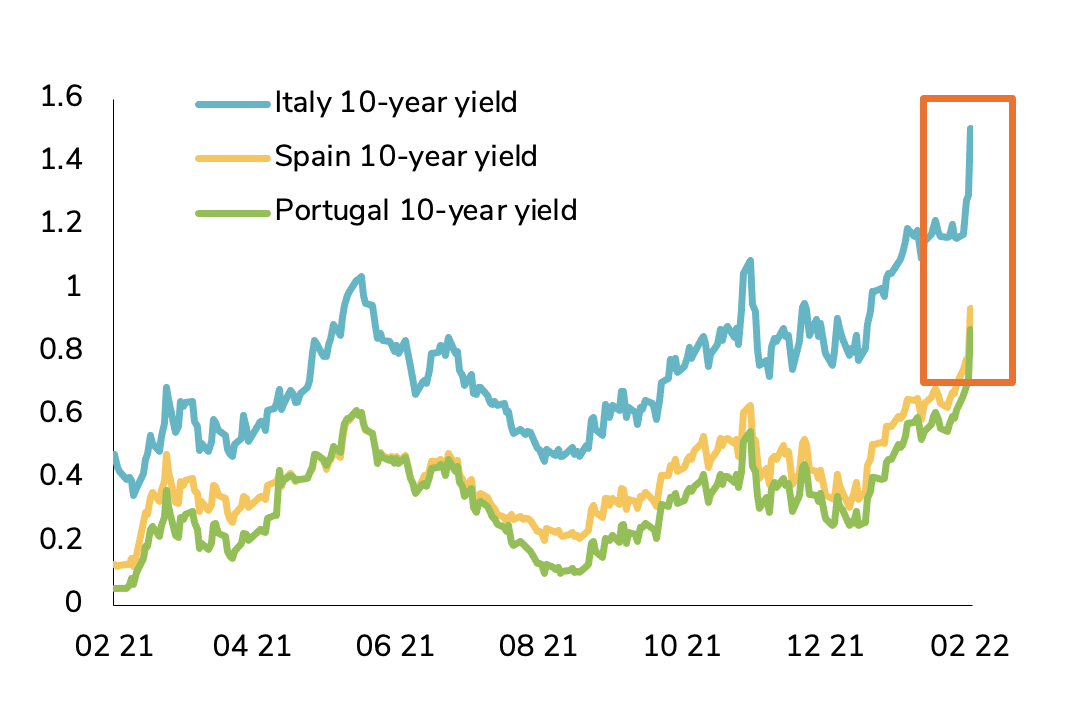

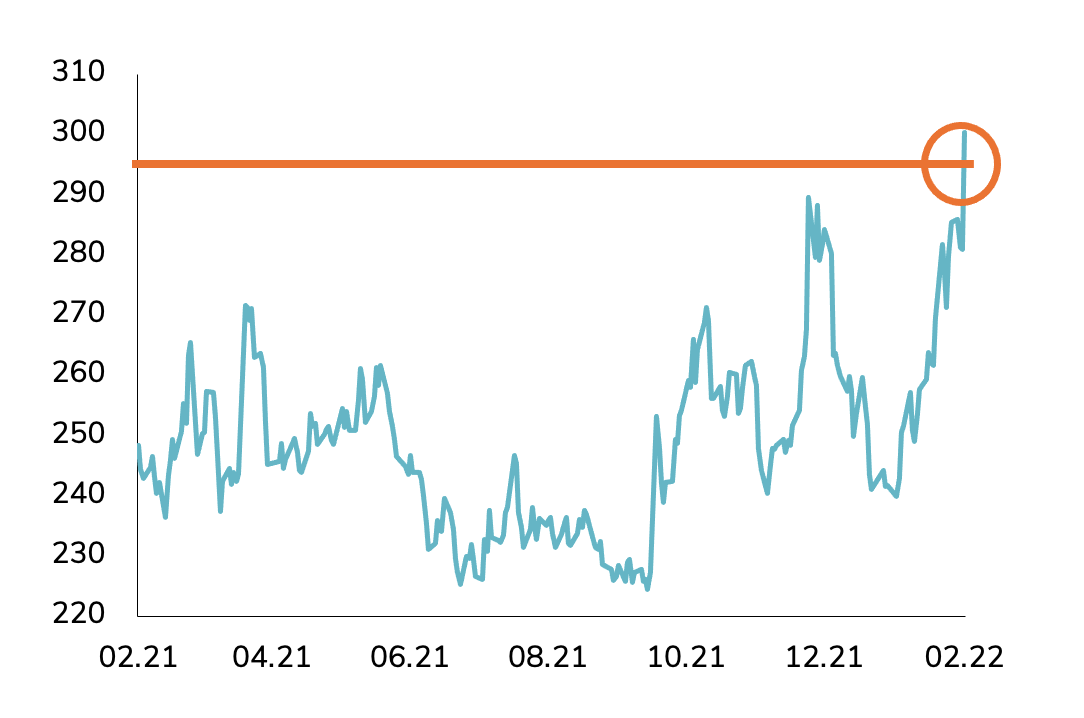

The Peripheral yields rose sharply during the press conference, reaching their highest levels since June 2020. The difference between Italian and German 10-year yields exceeded 150bps and the Italian curve has a positive yield from the 2-year tenor (November 2023).

Peripheral 10-year yields

Source: Bank Syz, Bloomberg

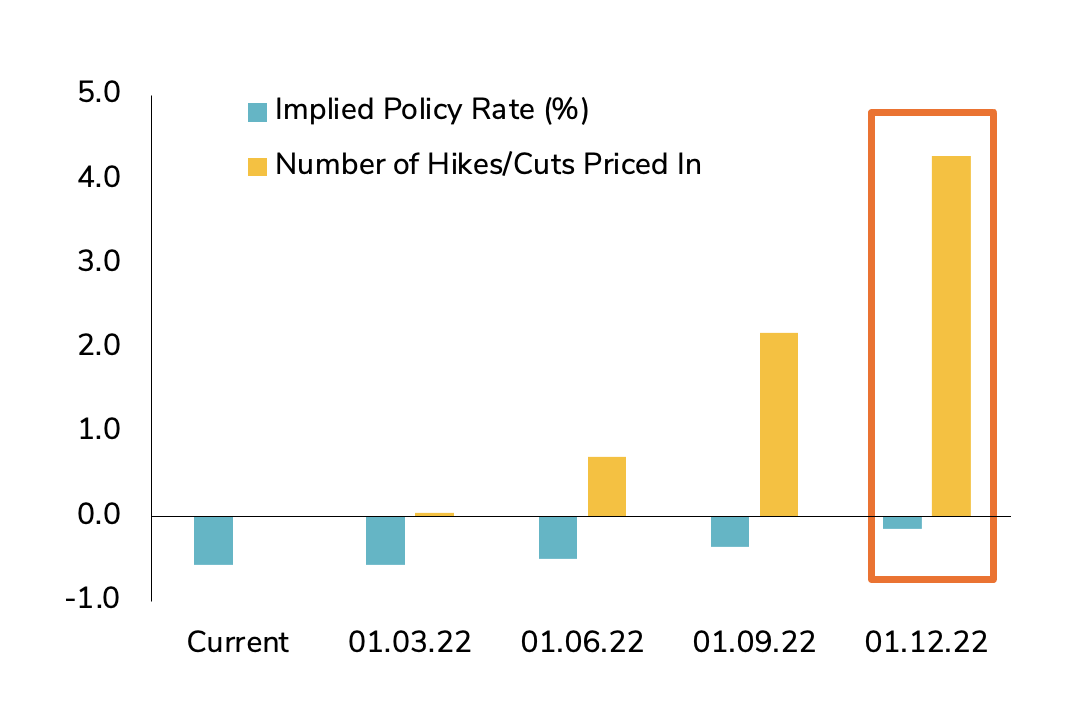

This morning, market participants (economists, investment bank research, brokers) adjusted their outlook based on the latest ECB meeting. They now see a high probability of a first hike in 2022.

The market also expects it, although their view is more aggressive: The EUR’s OIS Curve now calls for four hikes (of 10 basis points each) by December 2022.

ECB – Eur overnight indexed swap curve (%)

Source: Bank Syz, Bloomberg

But this optimism that the European economy is so strong also raises the question of whether the resilience of European economy could offset this potential tightening of monetary policy. And for now, the market’s answer is clearly negative with the acceleration of the flattening of the German yield curve: the German Government curve is now the flattest it has been since 2008 (!)

Yield differential between 5-year and 30-year German government bonds

Source: Bank Syz, Bloomberg

What credit market is telling us?

In sympathy with European equities (-2%), the credit market took the news badly with Investment Grade (above BBB-) credit spreads rising the most since the mid of 2020.

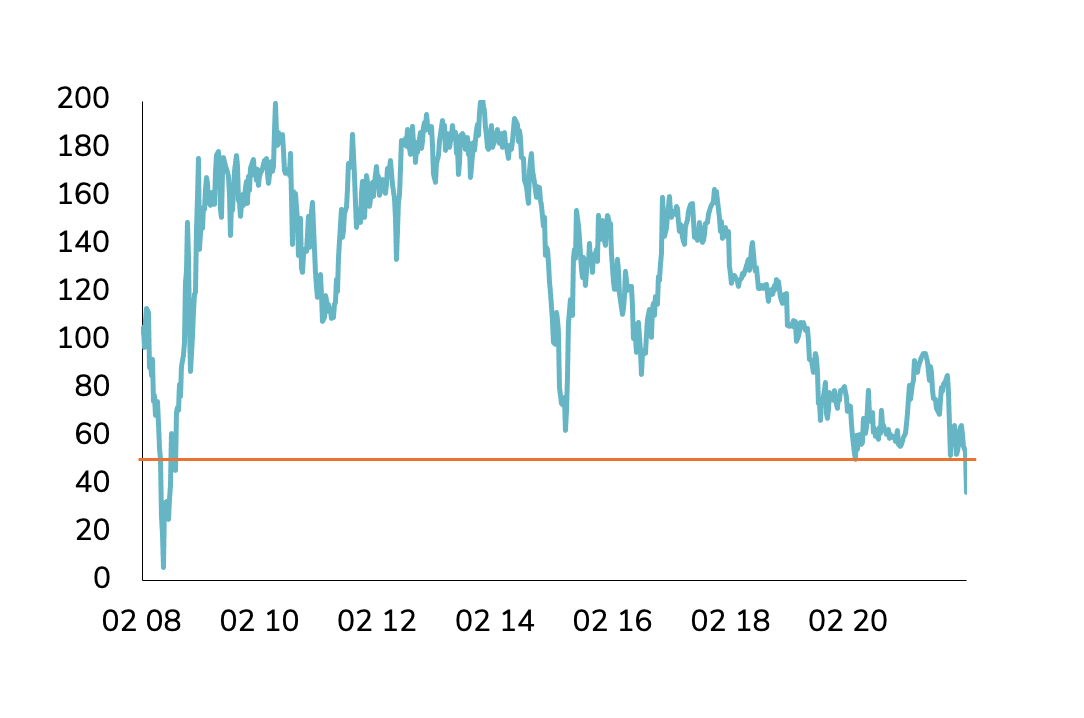

The European High Yield market also performed poorly on the news. The average credit spread of the US High Yield market reached a new 1-year high, putting further pressure on the 2022 performance which have already lost more than 1.5% in January).

European high yield - average credit spread (in bps)

Source: Bank Syz, Bloomberg

Our take

The first ECB meeting of 2022 was more optimistic than the market expected. It puts additional (upward) pressure on all European government yield curves, especially on the short end (1-5 years). In the U.S., the Federal Reserve (FED) is reducing U.S. financial conditions in the face of high inflation, but driven by demand and wages in addition to a tight labor market. In Europe, inflation is mainly driven by commodities, while wage growth remains weak, which is seriously hurting consumption. But current conditions (end of pandemic?) leave a small window for Christine Lagarde to tighten monetary policy without doing too much damage to the European economy. Base on this new scenario:

- The European Treasury yield is expected to rise again, with the 2-year yield approaching 0%.

- Pressure is likely to remain strong on peripheral government bonds, with Italy (the main beneficiary of the ECB’s quantitative easing) the most at risk.

- The flattening of the European yield curve is not a positive sign for the credit market. It could suggest that the European economy is not strong enough to support a much less accommodative monetary policy.

- Finally, European high yield is likely to suffer more from declining liquidity, rising interest rates (investors will be less likely to seek lower ratings for higher yields), and continued tight valuations.

Overall, this will lead to greater volatility in the European fixed income market throughout 2022.