.png)

"More money than God” was how President Joe Biden referred to Exxon Mobil's profits. Like other political leaders, the American president is facing the discontent of households as gasoline (petrol) prices rise at the pump. In June, the average price per gallon nationwide exceeded five dollars for the first time in US history. This increase, of course, has implications for the Consumer Price Index (CPI) since energy accounts, directly and indirectly, for about 20% of the benchmark basket.

Oil refining margins have exploded

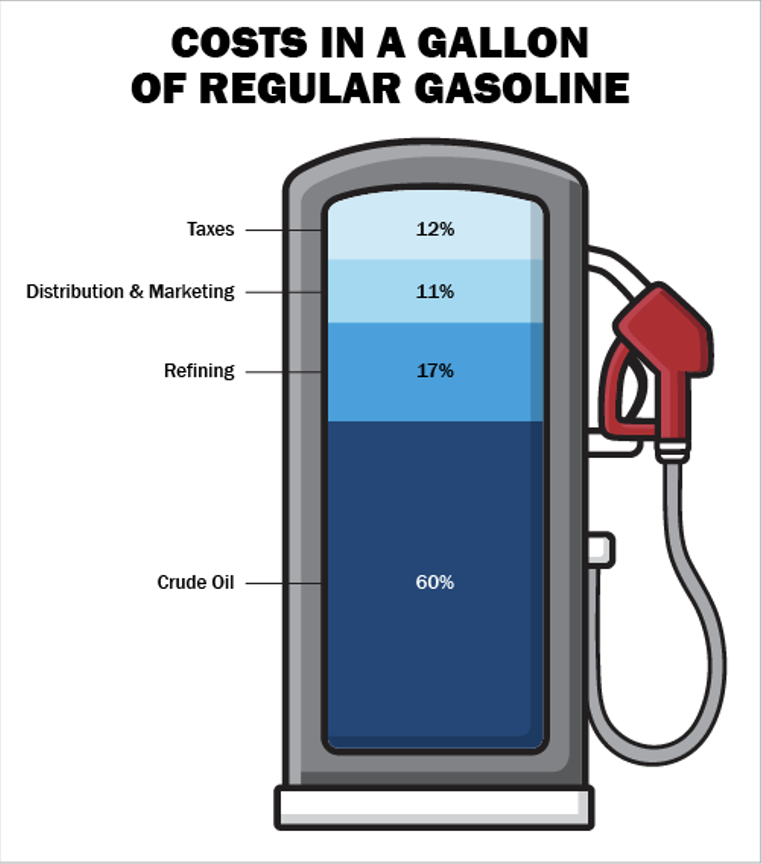

One reason for President Biden to point the finger at the oil giants is the surge in refining margins. While the rising price of a barrel of crude oil does have an impact on gasoline prices, other costs - taxes, distribution, and marketing costs, as well as refining margins - also determine the price of fuel.

Source: US Energy Information Administration, Gazoline and fuel update. & www.chaikinanalytics.com

The percentages in the chart above represent an average over several years and could be used to predict the price of a gallon of gasoline at the pump based on the price of a barrel of crude. Historically, there is a ‘counter-cyclical’ effect on refinery margins: a rise in crude oil prices tends to reduce refinery margins due to lower sales. Conversely, a fall in prices usually leads to an increase in margins due to recovering demand.

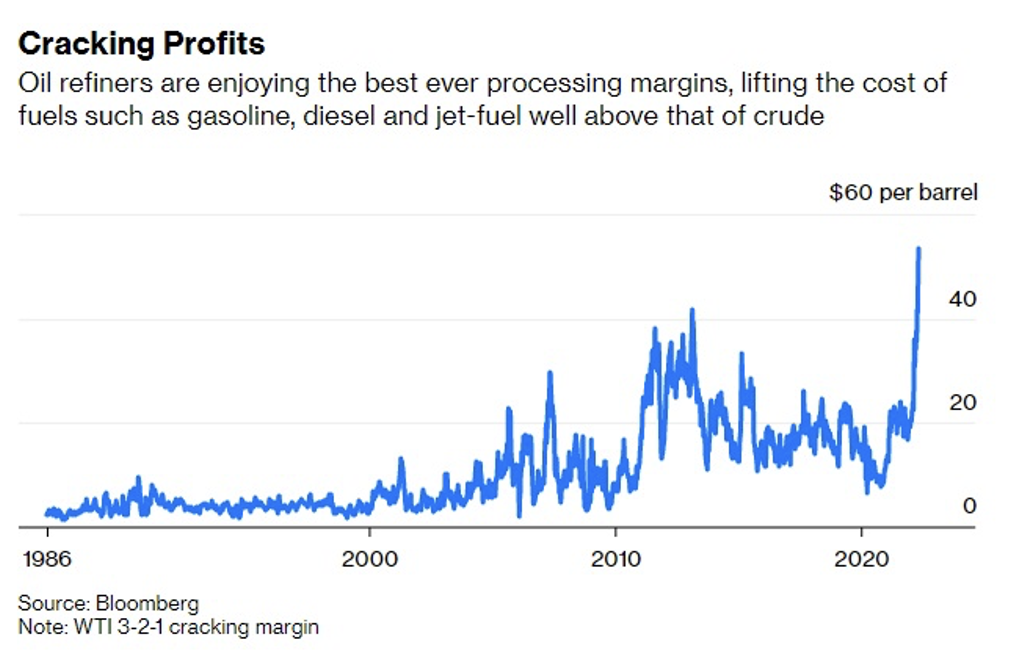

This relationship has been undermined for several quarters. An increase in refining margins accompanies the rise in the price of oil per barrel, with a multiplier effect on the price of fuel. The price of a barrel of oil is reaching record highs, but the price of gasoline is rising even faster than the price of crude. Today, the price of gasoline in the US is more than 60 cents per gallon higher than expected, based on crude oil prices.

While the price of oil has soared nearly 40% in the first half of 2022, refining margins continue to rise. The ‘crack spread,’ or difference between the price of crude oil and the price of refined products, was historically around USD 20. Today, that figure is in the USD 60 range. The largest refining companies, such as Valero and Marathon Petroleum, are generating their highest profit margins in decades.

Source: Bloomberg

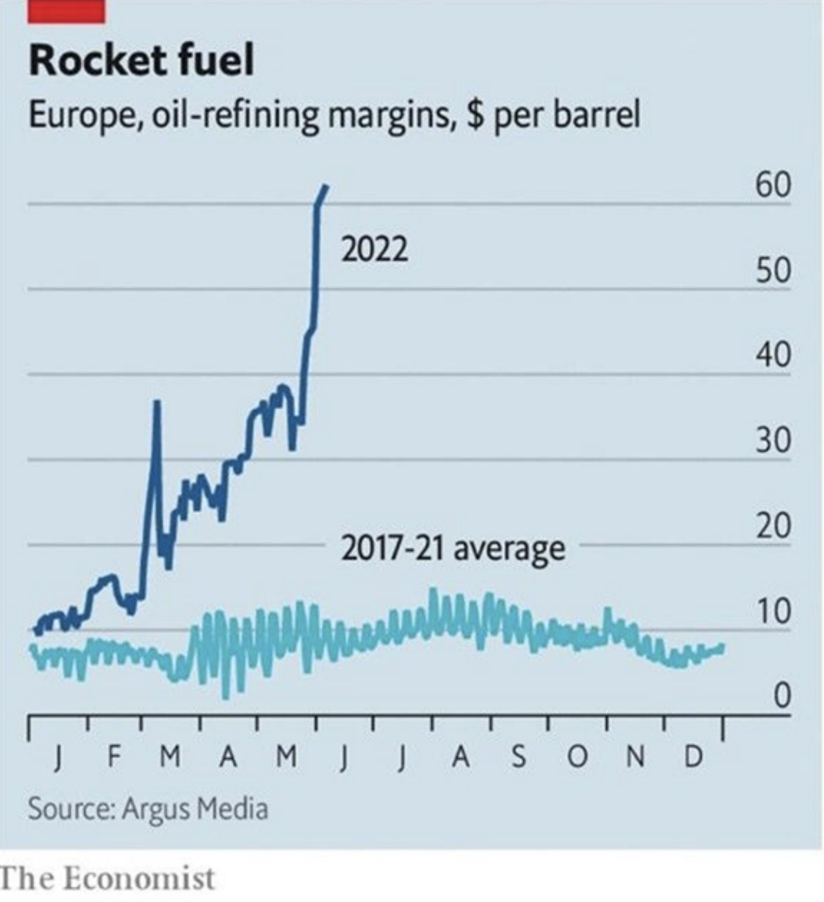

The explosion of refining margins (and its consequences for petrol prices) does not stop at the US border, it is a global phenomenon that also affects the European continent (see graph below).

Source: Argus Media & The Economist

How can we explain such a rise in margins? The main reason is the decrease in refining capacity.

The collapse of refinery capacity

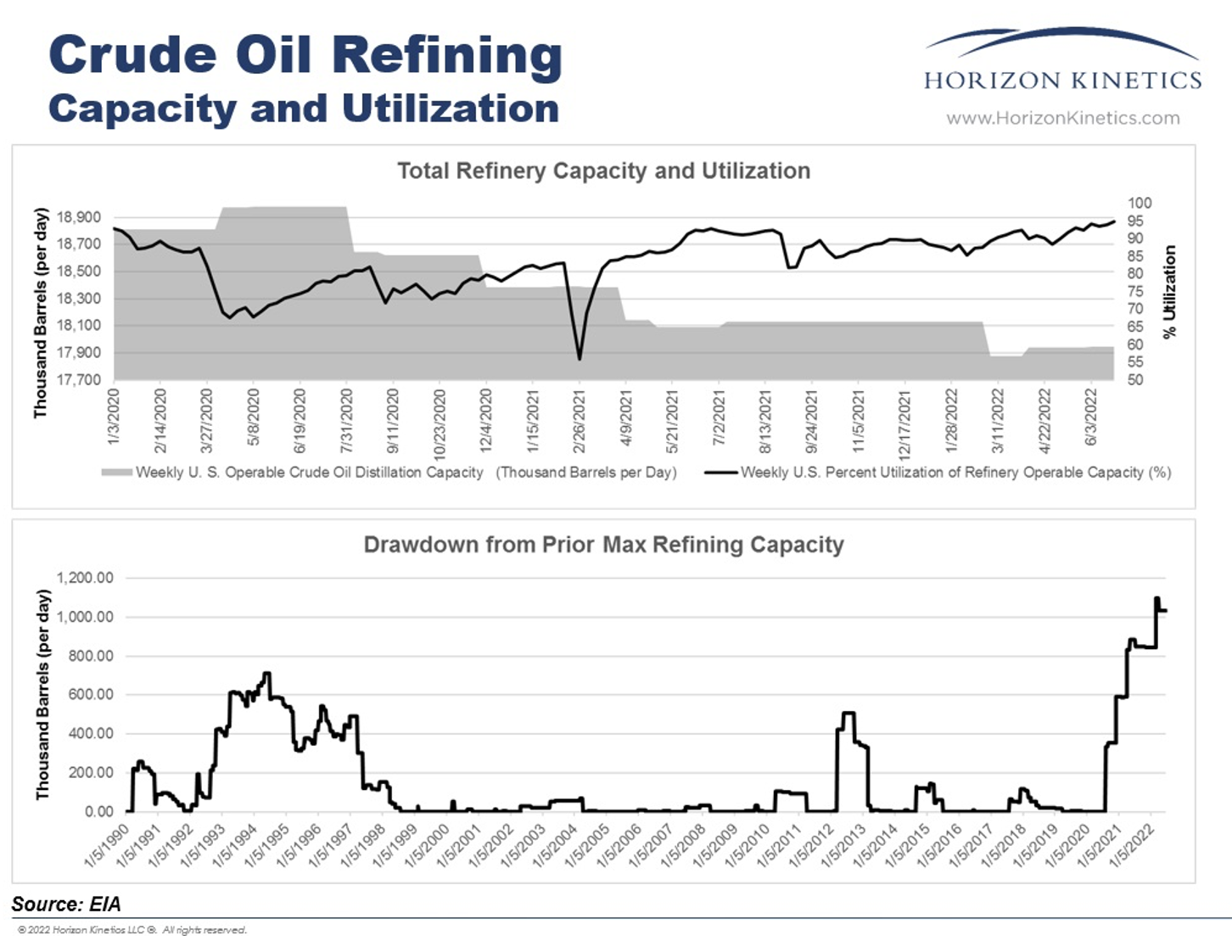

As shown in the chart below (top), refining capacity in the US (grey area) has been declining steadily since 2020, pushing utilisation rates to near 100%.

On the lower part of the chart, we can see that the US has lost more than one million barrels of crude oil per day in refining capacity since mid-2020. This is the largest decline on record.

Source: EIA & Horizon Kinetics LLC

This phenomenon is not specific to the US, however, as the global reduction in daily capacity is approaching three million barrels.

There are many reasons for the decline in refinery capacity. These include extreme weather, errors in demand forecasting, and the withdrawal of refineries located in Russia from the market, due to the war with Ukraine.

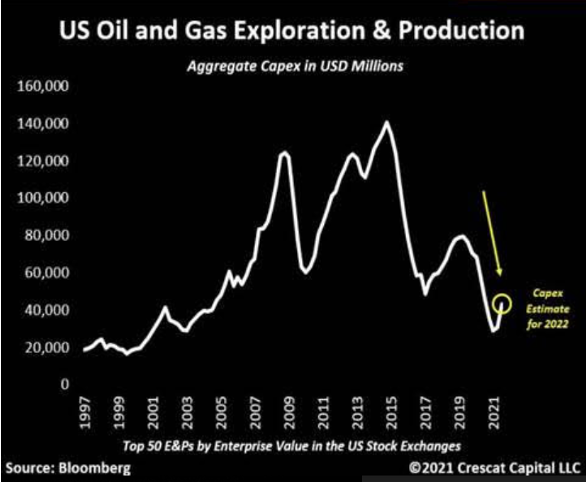

However, the most important cause of this loss of refinery capacity is the significant decline in investment in the industry. This is not a recent phenomenon, as the number of refineries has been decreasing since the early 1980s.

In fact, no new major refinery has been built since the late 1970s, while many are closing or being integrated into large oil groups. In 2021, the number of refinery closures exceeded newly-built capacity for the first time in decades. This trend has created inadequate refining capacity to meet demand. In the event of adverse weather or unforeseen disruptions, the imbalance between supply and demand becomes very wide and leads to even higher margins.

While politicians are singling out refineries, the fact is that companies are operating within legal limits and antitrust laws do not prohibit higher margins.

It should also be noted that refining companies tend to track certain market indicators to forecast demand. When the Covid-induced blockades began, the transportation industry came to a halt and most companies forecast lower oil demand in the future.

In addition, the social movement favouring soft mobility and the energy transition, mean it is understandable that oil companies have tended to reduce production capacities.

However, as of 2021, energy demand has picked up much more strongly than expected. After years of very strong pressure from governments to reduce fossil fuels in favour of green alternatives, oil companies are reluctant to increase capacity again. These companies have been so discouraged from expanding that the CEOs of some major oil companies have gone as far as saying that no new refineries will ever be built in the US. Given the resources and large investments required to build a refinery and the pressure from environmental lobbies, there is currently no viable short-term solution.

Solutions to gasoline price pressures

While no immediate solution appears to exist to pressure refinery margins, governments do have some tools to mitigate soaring prices at the pump. One of the most popular is the use of taxation: either imposing one-time taxes or reducing the national petrol tax. The latter has already been proposed by President Biden, who has called for a three month suspension of the national gasoline tax to offset record prices.

Crude oil accounts for 60% of the price of gasoline, with refining costs, federal taxes, and distribution costs making up the rest. Removing the national tax could therefore have a substantial impact on fuel prices for consumers. It would not solve the imbalance between supply and demand for petroleum products, but at least start to curb price increases in the short term.

Another solution is to put pressure on demand. Rising US interest rates should eventually increase unemployment and decrease wages, which should then weigh on demand. However, it is important to note that energy demand is inherently inelastic. Many of our daily activities require us to move, likely requiring fuel. Imposing recessionary conditions only restricts low-income households' access to this resource, plunging them further into poverty, without a significant impact on the demand for gasoline.

In the long term, the reduction in pump prices will have to be resolved by improving the supply situation. This means increasing refining capacity once again. For oil companies, that means reversing the sharp decline in fossil fuel investments that began several years ago.

Russia's invasion of Ukraine has changed the energy security situation in many developed countries. It is imperative that we adopt pragmatic policies that continue to invest in the energy transition while encouraging oil companies to increase their fossil fuel production capacities in the coming years. Indeed, Germany has just pushed for the Group of Seven countries to backtrack on a commitment that would end funding for foreign fossil fuel projects by the end of 2022. This may be just the beginning of a new investment cycle in this sector.

Source: Bloomberg & Crescat Capital LLC