.png)

Scenario 01 —

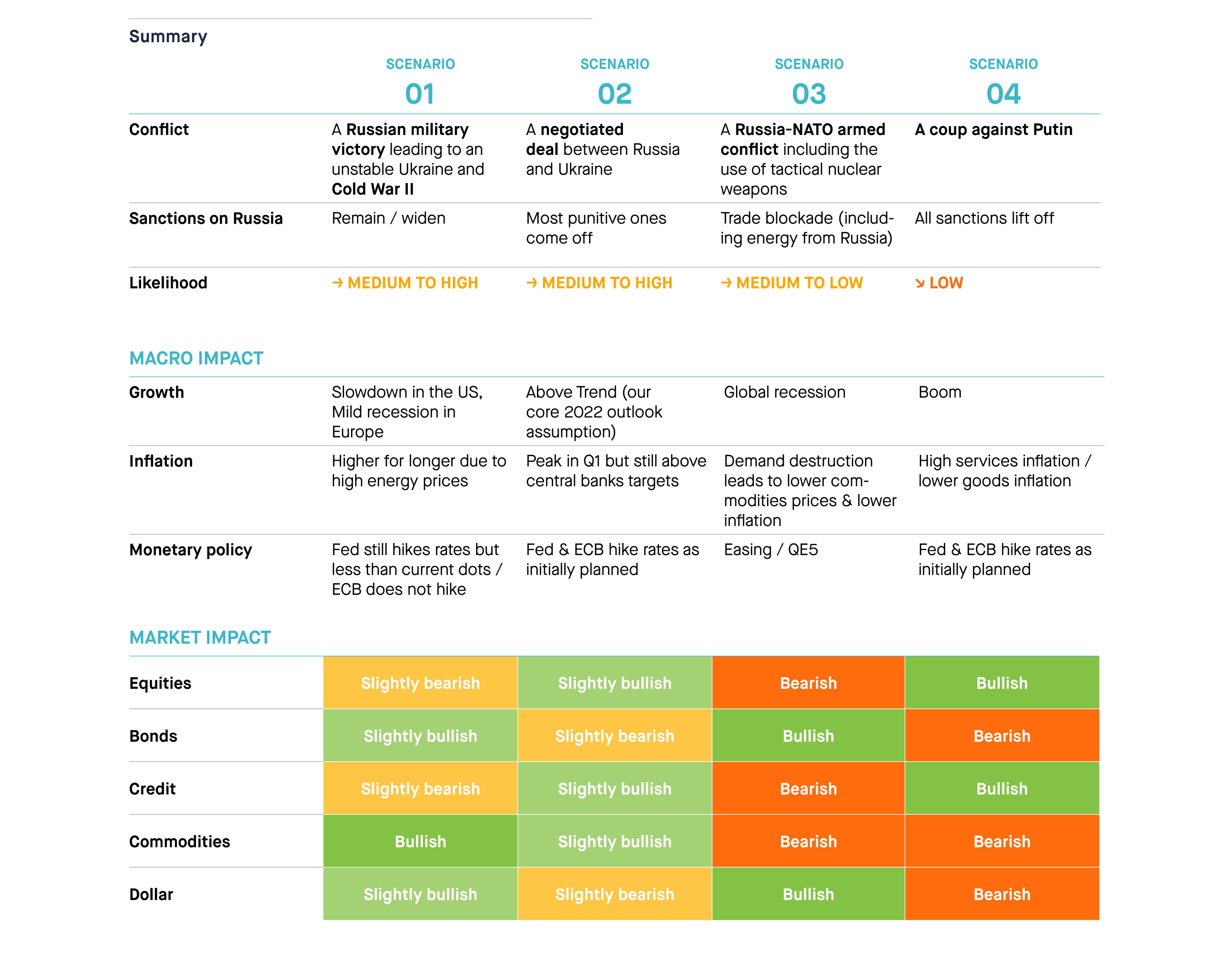

A Russian military victory leading to an unstable Ukraine and Cold War II

This scenario is a devastating one from a humanitarian perspective as it would probably imply heavy human casualties – including civilians – on both sides. In such a scenario, Putin is likely to stay a pariah on the international stage while the Russian economy and financial markets would be unlikely to reestablish their links with the West.

Macro impact

Under this scenario, we expect a slowdown of US GDP growth and a mild recession in Europe, i.e no stagflation but not too far from it. As Russian energy supplies are likely to stay limited, oil and natural gas prices are likely to stay high and should keep inflation higher for longer. Supply chain disruptions are expected to be significant and probably the longest since WWII in several industries.

On the monetary policy front, the Fed is likely to hike rates but probably less than what the current Fed dots imply. The ECB is unlikely to hike rates despite energy prices keeping inflation much higher than the ECB target.

Market impact

This scenario is not the most bullish one for risk assets. However, as it does not involve a material deterioration from where we currently stand, we expect further equity and credit market downside to be limited. Earnings growth should be revised downward by around 10% while equity valuation should not deteriorate further. Global equities could decline by another 5% to 10% while Equity volatility is expected to stay high. In this context, investors are likely to favor defensive quality growth stocks with strong business models, robust balance sheet, high free cash flow generation and pricing power. US equities are likely to outperform the rest of the word.

With global growth slowing down, government bonds are expected to perform decently although bond yields are unlikely to decline much from current levels given the high inflation level.

Under this scenario, the commodities bull market is likely to keep running as supply stays constrained while global GDP growth is likely to be strong enough to avoid demand destruction.

The dollar is expected to stay strong as a safe haven.

Scenario 02 —

A negotiated deal between Russia and Ukraine

This is the scenario, which is obviously the closest to our heart on all counts. It first involves a ceasefire and then an agreement from all parties to find a solution to the conflict. Such a rosy scenario looks unlikely at this stage given the high level of tension but a visit to Moscow over the last week-end by Prime Minister Naftali Bennett of Israel to meet at the Kremlin with President Putin shows that a negotiated deal is still an option (medium to high probability from our point of view).

Should a ceasefire take place, some of the sanctions will be progressively lifted but not all of them.

Macro impact

A negotiated deal means that our 2022 global outlook assumptions – i.e global growth above trend – are still valid.

We also expect inflation to peak in the first quarter and then start to normalize although it is likely to stay above central banks’ target for some time. Central banks will seize this window of opportunity to tighten monetary conditions according to initial plans.

Market impact

Such a scenario will be slightly bullish for global equities. Earnings are expected to grow in the high single digits. Valuation ratios will initially expand due to the relief of geopolitical risk but multiples will be capped as bond yields are expected to resume their upward trend. International stocks (Europe, Japan) are likely to catch up some of their recent underperformance while value should outperform growth.

Within Fixed Income, credit and emerging markets spreads are expected to tighten. Government bonds yields are expected to resume their upward trajectory (bear flattening).

With a ceasefire, we expect commodities outperformance vs. equities to come to a halt as Energy and Food prices are likely to come back to pre-crisis levels. On the currency side, the Euro should strengthen against the dollar and the Swiss Franc.

Scenario 03 —

A Russia-NATO armed conflict including the use of tactical nuclear weapons

This is basically the ugliest scenario both from a human and macroeconomic perspective. The odds are medium to low but it is indeed a very fat tail event with meaningful consequences for our daily lives and obviously for financial markets.

This scenario could occur if the conflict spill over to the West with NATO becoming involved. A deepening crisis would most likely result in massive energy supply cuts to Europe and a trade blockade at the global level.

Macro impact

The resulting macroeconomic effect would be a full blow global recession. While commodities prices and inflation would initially soar, the recession will lead to demand destruction and thus lower commodities prices and deflation in the medium-term. The high level of leverage in the system creates a high risk of sovereign debt crisis and corporate defaults.

Central banks will be forced to reverse their initial plans and move back into a monetary policy easing cycle (Quantitative Easing “5” in the US and more money printing in Europe & Japan) instead of tightening.

Market impact

Global earnings growth could collapse by -20% / -30% while valuation multiples will be hit due to geopolitical risk and macro uncertainty. Defensive / bond proxies stocks are expected to outperform. US Treasuries, Bund and Swiss government bond yields are likely to collapse (bull -steepening) due to deflationary expectations and a flight to quality. Peripheral spreads in Europe are likely to widen similar to credit and emerging bond spreads.

Commodities will enter into a bear market while Gold could become the best performing asset class.

Scenario 04 —

A coup against Putin

There has been constant speculation for most of Putin’s 22 years in power as to what it would take to trigger his departure. Looking back at history, authoritarian leaders tend to leave according to two scenarios (beyond illness or natural death): forced out by the street or by the elite. While neither of these two groups seem to be in a position to remove Putin from power, the sanctions and isolation of Russia by the West might be the catalysts that trigger a coup against him. The New Russian leaders might then negotiate a truce or prepare an orderly retreat enabling all sanctions to be lifted.

Macro impact

Such a scenario could lead to a resumption of global trade, an easing of supply chain disruptions and a boost in consumer spending thanks to a dramatic retreat of energy prices. While services inflation will remain high (wages, rents, etc.), goods inflation will peak in Q1. Central banks are expected to hike rates but financial conditions will improve as credit conditions will be loosening again.

Market impact

This would be a very bullish scenario for equity markets due to an improvement in sentiment and upward earnings revision in some sectors. The segments of the market which have been suffering the most over the last few months (European banks but also unprofitable Tech stocks, Momentum, etc.) would most likely outperform. Russian assets will enjoy a spectacular recovery. Government bonds, the dollar and commodities would underperform.

Final words

At this stage, it is very difficult to assign precise odds to any of these scenarios although cold war II (scenario A) or negotiated deal (Scenario B) look as the most likely ones.

As always, there are the known unknowns but there also “unknown unknowns”. Based on our investment philosophy, we feel it is very important to remain true to our investment process and closely follow our investment risk parameters to optimise downside protection.

A summary of our scenario analysis is provide below.