.png)

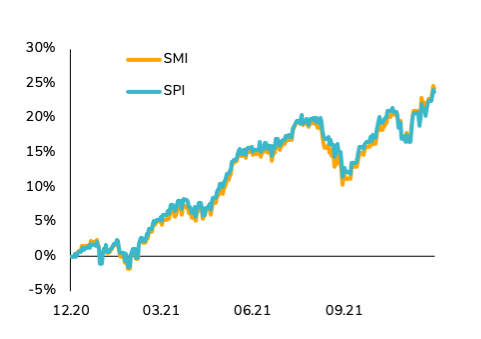

Swiss equities had a strong year in 2021, reaching record levels. The performance of the SPI - the index that covers virtually the entire stock market with more than 210 stocks - is comparable to that of the SMI (the 20 largest market caps). Factoring in the currency effect (i.e. an appreciation of the Swiss franc against the euro), Swiss stocks outperformed the main European equity indices last year.

SMI & SPI indices 2021 PERFORMANCE

Source: Banque Syz, Bloomberg

With regards to sector performance, it is difficult to establish a clear hierarchy. At the end of 2020, many strategists expected cyclical stocks to outperform at the expense of more defensive sectors. In the end, neither of these two market segments really dominated. Idiosyncratic factors explain the over- and underperformance of individual stocks.

For example, the top three in the SMI for 2021 are a luxury goods company (Richemont), an industrial stock (Sika) and a financial company (Partners Group). While defensive stocks such as Novartis (healthcare) and Swisscom (telecoms) had negative contributions to the performance of the index, the same is true for Logitech (technology) and Holcim (materials) for specific factors. In the SPI index, stocks such as Medartis Holdings (medical technology), Swissquote (online banking) or Sensiron Holdings (energy transition) recorded triple-digit gains.

Nevertheless, a classification of stocks according to “growth” and “value” style exposure reveals a clear outperformance of the former. This dichotomy is also reflected at the valuation level, a dimension we will cover in the last part of this article.

A strong Swiss franc

It seems difficult to discuss Swiss equities without mentioning the Swiss franc. Indeed, Swiss companies in the SPI generate - in aggregate - around 33% of their sales in dollars and almost 40% in euros. At the same time, the share of costs denominated in foreign currencies is much lower. This unfavourable equation has always pushed Swiss companies to innovate and increase their productivity in order to cope with the long-term appreciation of the franc. Nevertheless, short- and medium-term exchange rate fluctuations have consequences for the performance of the SMI and SPI indices.

The dollar appreciated against the vast majority of international currencies in 2021, thanks in particular to the strong growth of the US economy and expectations of rate hikes in a context of the highest level of inflation since the 1980s. The strength of the greenback has enabled the Swiss franc to remain stable against the dollar in 2021. This is not the case against the euro. Indeed, despite an euphoric market sentiment, the Swiss franc has not been penalised by its safe haven status - quite the contrary. In fact, the euro depreciated by almost 5% against the franc over the year, despite the Swiss National Bank continuing to be very active in the foreign exchange markets.

The strength of the Swiss franc is mainly explained by the very solid fundamentals of its economy. The economic growth rebound of Swiss GDP in 2021 (+4% in real terms) was admittedly less spectacular than that of its European neighbours, but it was still twice as high as the 10-year average. The growth rate should remain above potential in 2022, at around 3%. Public finances deteriorated during the pandemic but to a much lesser extent than in other developed countries. While the budget deficit is expected to be close to 3% of GDP in 2022, the fiscal situation should return to a positive balance as soon as 2023. Switzerland has also maintained a current account surplus. It should be 7.2% in 2022 and above 8% in 2023, well above the European surplus (3.2% according to the consensus).

A very important macroeconomic variable to consider is inflation. As in the rest of the world, inflation is on the rise in the Swiss Confederation. Although November’s inflation rate of 1.2% is the highest in a decade, it is nowhere near the price increases observed in the US and Europe. Why such a difference? While the strength of the Swiss franc plays a deflationary role, Switzerland’s lower dependence on fossil fuels and the openness of the labour market to foreign workers also play an important role. This relatively low inflation rate makes the Swiss franc more attractive in real terms. Indeed, real 10-year bond yields in Switzerland (-1.4%) are currently well above the German Bund (around -5% in real terms) and the US 10-year (-4.8%). This trend does not seem likely to reverse in 2022, unless a stabilisation or decline in energy prices provides a breath of fresh air to European inflation. From a fundamental perspective, it seems difficult to expect the franc to weaken in the coming quarters.

2022 Swiss equities Outlook

In our 2022 global asset allocation strategy, we continue to favour equities over bonds and cash. Indeed, global growth should remain above potential and earnings growth should remain positive. On the other hand, the normalisation of monetary policies in a context of high valuation multiples suggests that the risk/return trade-off should be less favourable for global equities than in 2021.

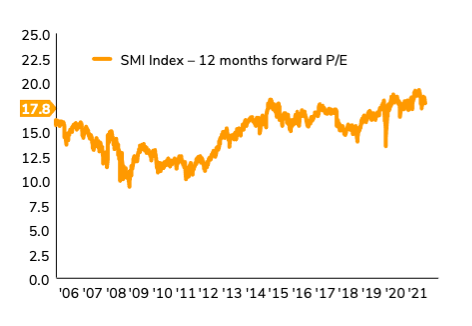

The same is true for the Swiss market. As mentioned above, Swiss equities have performed very well in 2021. Even if this rise is partly corroborated by an increase in earnings (+15.5% for the SPI), valuation levels at the end of the year are relatively generous, both on an absolute basis (P/E of around 20x expected earnings for the SPI in 2022) and in relative terms (the risk premium is now at 4%, the lowest since 2010).

SMI Index Valuation

Source: Banque Syz, Bloomberg

But in the context of negative real bond yields, investors will probably have no choice but to favour risky assets - including equities. Especially since earnings growth should remain robust in 2022 (around +12% for the SPI in aggregate) and could even be boosted by an acceleration of the consolidation trend. On the other hand, some companies are likely to experience pressure on their margins due to rising raw material and component costs, as well as rising wages in some countries of the world.

In terms of thematic and sector positioning, we have identified opportunities in three distinct segments. The first one is high quality Swiss stocks (strong balance sheet, stable earnings, strong free cash flow generation and which offer a high dividend yield). The phase of the economic cycle we are entering (tighter global monetary policy) is historically favorable to quality stocks. The pharmaceutical sector - which accounts for almost 40% of the SMI index - is a good source of defensive growth stocks. One example is Novartis, which has been sharply underperforming Roche recently and yet has a recognized pipeline of new products in the medium term that is somewhat undervalued at the moment.

The second attractive segment is financial stocks. Although we do not expect bond yields to rise sharply, we would not be surprised to see a slight steepening of the curve - at least early in the year. Banking and insurance stocks could benefit from this. These sectors continue to trade at a significant discount and have been underperforming last year.

Finally, we hope that interesting entry points will present themselves on the so-called secular growth stocks, as was the case with Logitech last November. Indeed, the stock has lost more than 40% since the summer, correcting past exaggeration. Many of these stocks are currently trading on very high multiples. While it seems justified to pay a premium to the market for some of these stocks, it would appear that market euphoria has led to some excesses. Typically, a stock such as Straumann, the world leader in dental implants, has returned 90% and is valued at over 70X future earnings. A correction in the equity markets would allow us to build up positions in Swiss “nuggets” at more reasonable price levels. Let’s not forget that technological and industrial innovation is one of the strengths of the Swiss economy. Its domestic equity market is full of companies with unique know-how and a sales growth rates that are on a par with the Nasdaq. But you have to be able to pay the right price...

Conclusion

Despite relatively high valuations overall, Swiss equities remain attractive not only to domestic but also to foreign investors. However, we expect more limited upside potential in 2022 than in 2021. We also expect more volatility, meaning very good alpha opportunities for stock pickers.