.png)

In mid-August, we entertained the possibility of a rebound in risky assets ("U.S. equities: the start of a new bull market?"). At the time, we recommended that investors be cautious, as the monetary tightening cycle remained unfavorable for equity markets.

Since then, the major US equity indices have continued their downward trend. At the end of the third quarter, the S&P 500 was down nearly 24% for the first nine months of the year, one of the worst performances in history.

The magnitude of the decline suggests that the worst is certainly behind us. What remains is to find the trigger for a sustainable rebound. Today, investors seem to be waiting for the famous "Fed pivot", i.e. the moment when the US Federal Reserve decides to abandon a restrictive monetary policy in favor of a more accommodating one (rate cuts, liquidity injections, etc.). Indeed, the correlation between monetary policy and the performance of risky assets is anchored in the minds of most investors. If the Fed "cracks", it could be the end of the "bear market" and an opportunity to rake stocks at good prices.

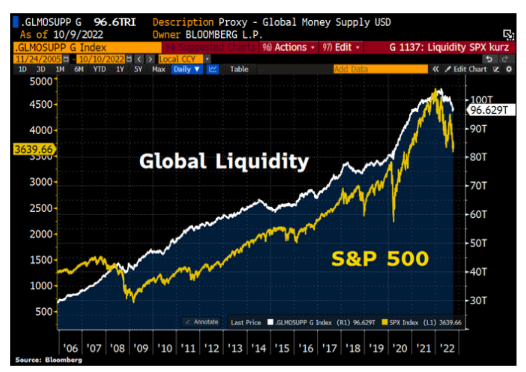

Liquidity proxy S&P 500 index

Source: Bloomberg

Are the conditions for such a "pivot" met?

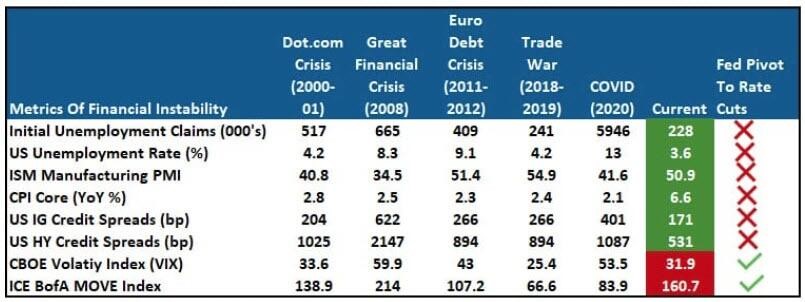

A Fed pivot checklist

In a recent study, Bank of America listed the conditions necessary for a Fed pivot. The different factors considered are classified in 2 categories: macro-economy and financial markets.

Regarding macroeconomic factors, a low unemployment rate, a PMI (monthly purchasing managers' survey) that remains in economic expansion territory and an inflation rate (excluding energy and food) that continues to accelerate are not likely to encourage the Federal Reserve to abandon its restrictive monetary policy.

Among the market elements considered, yield spreads between investment grade and junk bonds have not yet reached the stress levels that forced the Fed's hand during previous crises.

Only the MOVE (for bonds) and VIX (S&P 500 index) volatility indices are in a red zone, even if the VIX is still far from the record levels observed in 2008.

In aggregate, this historical comparison does not suggest an imminent pivot by the Fed.

Indicators that could cause the Fed to capitulate

Source: BofA

Are investors too pessimistic?

For many strategists, a simple change in tone from Jerome Powell could be enough to start a sustained rebound in risky assets. The reason for this is that market sentiment has reached such a level of pessimism that the slightest positive news can trigger a violent reversal of the trend.

It is true that the leverage of hedge funds is currently at a very low level, reflecting an excess of caution. A significant number of hedge funds are currently net short. In the event of a rise in equity markets, many hedge funds would certainly be forced to hedge and therefore buy massively.

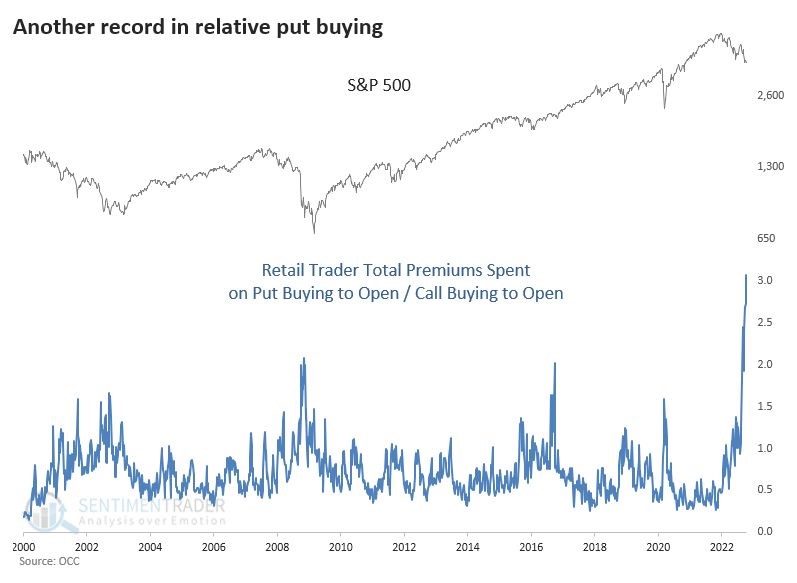

On the retail side, we are seeing massive purchases of put protection. Two weeks ago, the number of put options purchased was three times the number of call options purchased. Sentiment surveys also suggest that the market is oversold.

A record year for put purchases vs. call purchases

On the other hand, the aggregate allocation to the equity markets by the different types of investors has declined only slightly since 2021. So there has not been a massive reduction in the equity allocation. Perhaps because investors continue to believe that a rebound is both certain and imminent. But also because individuals have accumulated enough savings during the covid years, which makes them less inclined to panic than during previous bear markets.

Most investors are therefore not underexposed to the equity markets. This has two consequences: 1/ fewer sources of liquidity to sustain the rally in case of a rebound; 2/ some investors could start to panic and lower their allocation to equities if the bear market is prolonged.

Are equities cheap enough?

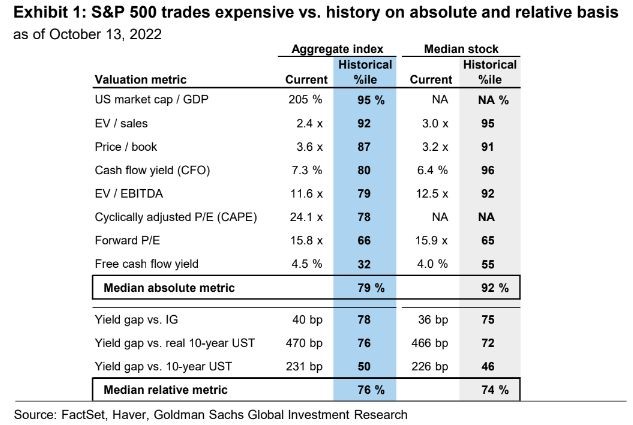

Looking at the U.S. market, the major equity indices cannot be considered undervalued, despite the very sharp decline since the November 2021 highs. Indeed, the S&P 500 is paying more than 15 times expected earnings for 2023. As a reminder, the same multiple was less than 10 times in the 1970s, the last decade with very high inflation.

The S&P 500 looks relatively expensive on a historical basis, both in absolute and relative terms (as of October 13, 2022)

As for the rest of the world, multiples are for the most part much cheaper than in the US. But there is some doubt about the earnings growth expected for next year, as analysts' expectations seem overly optimistic. And just as in the US, the bond market is now a serious alternative to equities.

Is a Fed pivot a enough for a sustainable rebound?

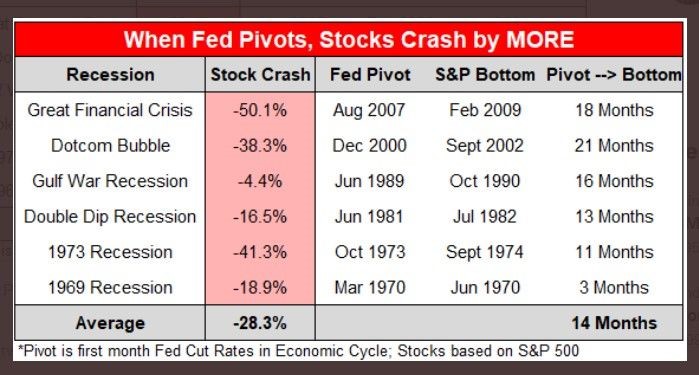

While a Fed pivot is considered by many investors as a necessary and sufficient condition for a rebound, this has not always been the case in recent history. Indeed, the table below shows that, on the contrary, the Fed's emergency course changes have often led to a continuation of the decline. Indeed, the pivots have mostly occurred during periods of financial market dislocations, marked by forced liquidations and panic selling. On average, there was a 14-month gap between the Fed's pivot and the market lows.

Buying stocks in anticipation of a pivot is therefore risky - even if the hoped-for pivot does occur.

Historically, a Fed pivot has triggered an accelerated decline in equity markets

Source: Nick Gerli, Thomas Callum

Rising real rates as the main market barometer

Rather than watching for the slightest hint of a pivot by Fed members, markets might be well advised to keep a close eye on another indicator: real rates, i.e. the difference between nominal bond yields and the rate of inflation expected by the market.

As the chart below shows, the real 10-year yield has been rising steadily, which is rather surprising. Indeed, if the market's expectations for inflation one year or more out come down substantially, bond yields should also start to fall and reflect rate cuts in the years to come. But this is not the case as the entire yield curve continues to rise.

In fact, this rise in real yields reflects a more worrying phenomenon: that of a dollar shortage linked to the fact that governments or companies are currently struggling to have sufficient access to the greenback. In order to obtain dollars, they are selling U.S. Treasury bonds, which is causing a drop in the price of U.S. government bonds (despite the drop in inflationary expectations) and de facto a rise in real yields.

To reassure the financial markets, a drop in real yields seems necessary. This decline can only occur if the markets perceive a deceleration in inflation, which would then lead to a decline in bond yields and the dollar, two pre-requisites for an improvement in financial conditions and liquidity in US Treasuries.

US 10-year real yields since 2008

Source: Bloomberg

Conclusion

An imminent pivot by the Fed seems unlikely, at least on the basis of macroeconomic and intrinsic financial market indicators. On the other hand, the pivot is not in itself a sufficient condition to reverse the downward trend of the markets. A worsening of the liquidity crisis due to the shortage of dollars could certainly force the Fed's hand, but this does not guarantee that the market lows are behind us. We are maintaining an under-exposure to the equity markets even if bear market rallies may occur before the end of the year.