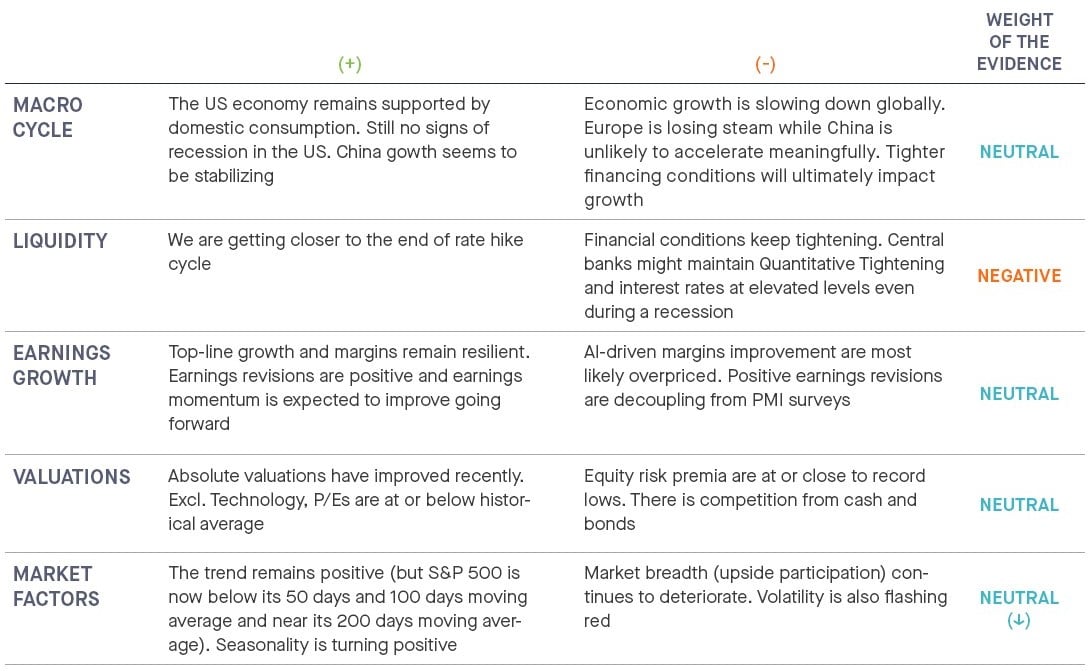

Ongoing risks continue to shape bear steepening. Firstly, the continuous reduction of the Fed’s Balance Sheet is depleting liquidity, further accentuating rate movements. Secondly, the escalation in geopolitical tensions and the resurgence of oil prices might exert temporary upward pressure on rates in the short term. However, this also reinforces the argument for an impending long-term growth slowdown. Thirdly, an inverted yield curve is not conducive to favouring the long end of the spectrum. Lastly, inflation, as reflected in breakeven rates, is not cheap, while the real yield curve is still deeply inverted.

Despite these challenges, several positive factors are emerging.

1. There exists an attractive asymmetry in rates, bolstered by the anticipation of a slowdown in both economic growth and core inflation. Ex: US 20-year yield @5% yield to maturity.

2. Real rates presently stand at their highest levels in a decade.

3. The market's consensus still leans towards fewer than one rate hike, with no cuts expected before the latter half of 2024.

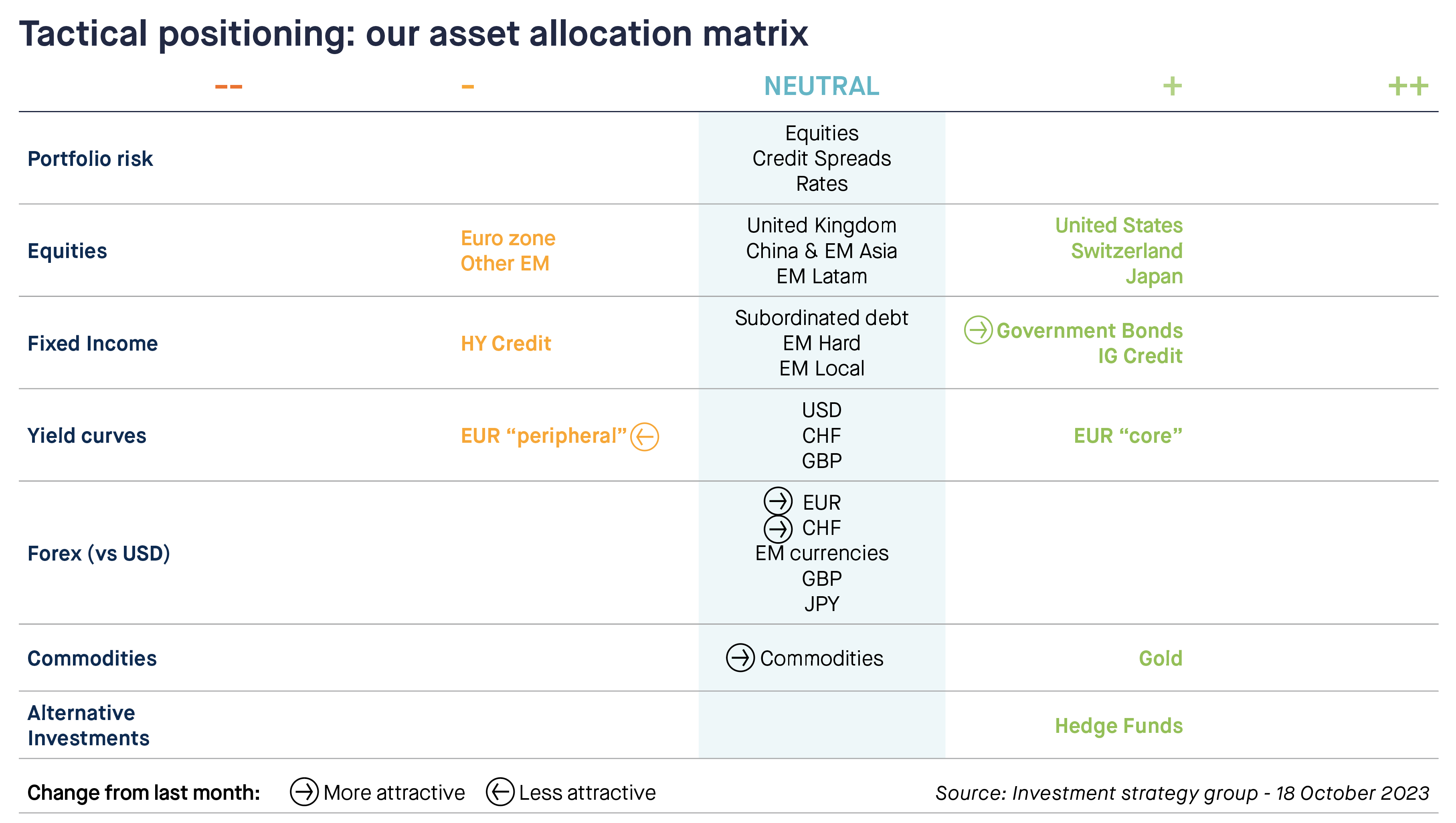

In this context, we recommend adding government bonds and to gradually extend duration, as there is an attractive asymmetry in long-term rates, supported by expected moderation in growth and inflation. The resurgence of oil prices could temporarily weigh on short-term rates but increases the case for a long-term growth slowdown.

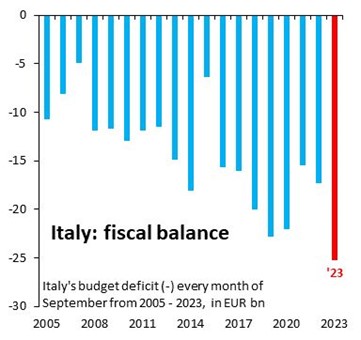

In Europe, considering our concerns about the Eurozone's growth outlook and the potential conclusion of the ECB rate hike cycle, we are adopting a neutral stance on EUR rates. We are downgrading Euro Peripherals bonds mainly due to the concerns on Italy’s fiscal situation. Indeed, Italy 10y risk spread over German bunds have spiked >200bps. Italy fiscal balance continues to worsen at a time when debt ratio is 140% of GDP while borrowing costs are rocketing.

Source: Robin Brooks

Within the credit space, our neutral stance emphasises high-quality corporate bonds. We are avoiding the pursuit of higher yields in the high yield sector due to overpricing relative to risk. In Emerging Market debt, we maintain a vigilant stance due to valuation and potential risk considerations. Higher oil prices and a strong US dollar pose challenges for oil-importing EM nations, especially Asian countries, while some Latin American countries may benefit.

FOREX & ALTERNATIVES

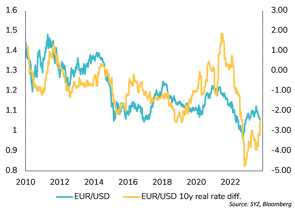

On the forex side, we are upgrading EUR and CHF against dollar from negative to neutral. Weak growth dynamic and disappointing economic data in Europe still are a drag for the EUR. The real rate differential remains in favour of the USD, but the gap has recently narrowed somewhat. We remain neutral on JPY, GBP and EM currencies (versus USD).

The real rate differential remains in favour of the USD, but the gap has recently narrowed somewhat.

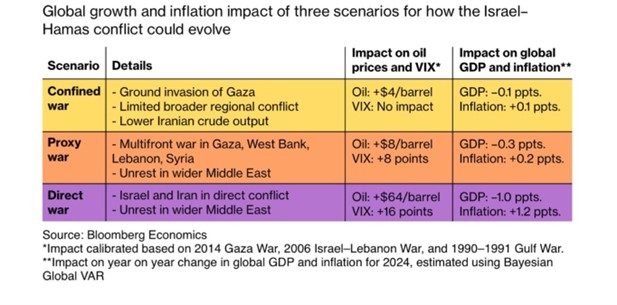

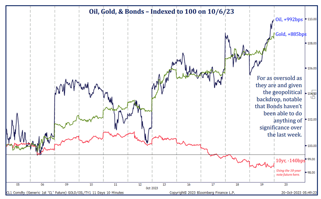

We are upgrading commodities from negative to neutral. Indeed, oil and gold have been the best portfolio hedges so far, since the start of Israel/Gaza conflict.

Within commodities, we remain positive on gold, which continues to exhibit low volatility with other asset classes and should be a beneficiary of any tail risk event. We note that a significant gap has opened between gold and real yields. Why? 1) With debt sustainability having become an ever-increasing issue, the market anticipates that real interest rates cannot stay at this level for too long; 2) Investors buy gold as an insurance against adverse circumstances (inflation, recession, etc.) But for gold to appreciate in dollar, a drop in real yields is probably required. In the meantime, gold remains a true diversification asset.

Oil and gold have been the best portfolio hedges since the start of Israel / Gaza conflict.

Source: Strategas

We also maintain our positive view on Hedge Funds. We like well-established Global Macro funds that have a multi-portfolio managers approach. We cautiously like Relative Value funds but are wary of liquidity conditions. We like having a core position in a diversified systematic strategy with a long-term commitment. We prefer staying away from equity long/short and directional funds as their beta is too high. We do not like Event Driven funds as we believe the merger & arbitrage landscape will be very challenging in 2023.

.png)