.png)

First, retail investors have largely exited the market, as shown by the significant ETF outflows. Many investors sold assets that performed very strongly, such as gold which reached an all-time high in February, and have redirected the funds toward the AI theme, tech stocks at large, and semis in particular. More recently, some have moved into cash while waiting for high-profile IPOs such as SpaceX and OpenAI.

Among professional investors, specs had already been reducing their long positions; but when gold fell below its 200 days moving average, this became the final trigger for CTAs which have now shifted from being net long to short.

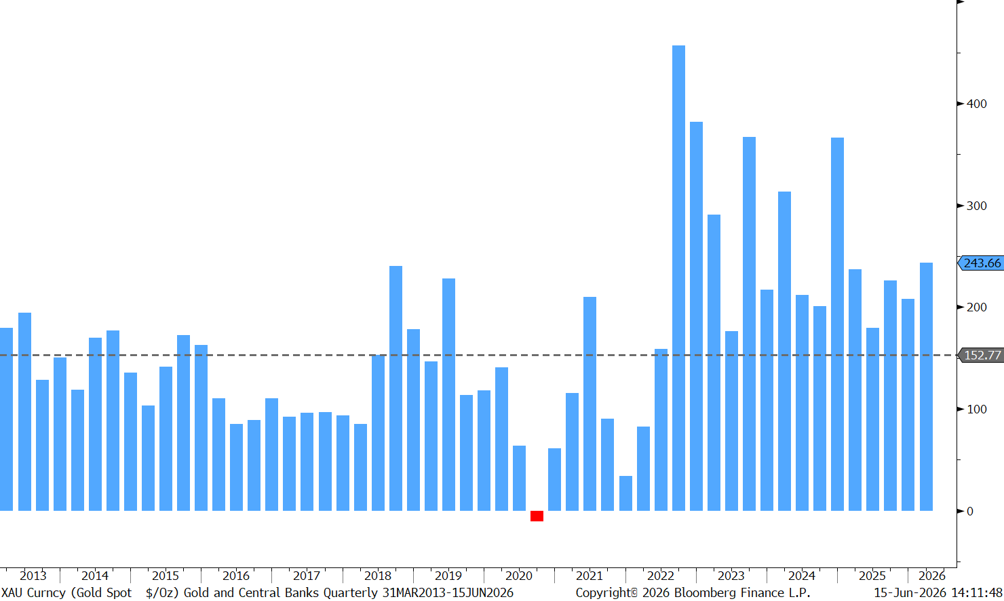

Central bank activity has also been mixed. Some countries, such as India, Turkey and Russia, have been selling gold from their reserves to fund their defense spending, defend their currency and/or to finance their budget (for oil-importing countries). However, other central banks used corrections as a buying opportunity in the past. Reportedly, the PBoC has continued to buy gold, reflecting the continued debasement and de-dollarisation trends (cf graph 1).

Interestingly, according to the ECB's June 2026 report, gold represented 27% of global central banks reserves at the end of 2025 (vs. 20% in 2024); their share of US Treasuries having fallen to 22% (vs. 25% in 2024). If a deal is reached between all parties in the US-Iran conflict as discussed over the weekend, lower geopolitical risk could remove some of the pressure off gold prices. At the same time, it could also support gold if it leads to expectations of lower interest rates.

Looking ahead, gold prices could stay supported once inflation and USD strength begin to ease and markets begin to price in fewer rate hikes. For now, however, investors remain on the sidelines as recent US macro data continue to point to a strong economy, raising the possibility that the Fed may need to hike its key rate at least once, rather than cut them as expected under new Fed chairman Kevin Warsh. In addition, some developed market’s central banks, such as the ECB, the BoE and the BOJ, are expected to implement a more pronounced rate tightening cycle in 2026. As a result, we expect gold prices to remain supported but rangebound this summer. However, we expect stronger strategic support to re-emerge in the latter part of the year. The key long-term drivers remain intact: currency debasement, de-dollarisation, and gold's role as a safe-haven asset and a portfolio’s diversification.

Global Gold Demand from Central Bank Net Purchases Quarterly

Gold – Short Term