.png)

Surprise #1 —

US Inflation drops below 4%

[Probability: Medium]

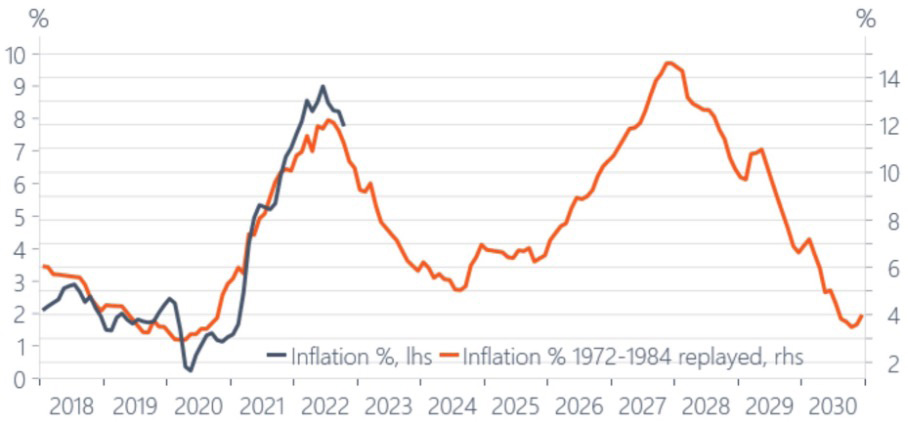

The surge of inflation to almost double-digit levels was most likely the biggest macro-economic surprise in 2022. As we enter into a New Year, inflation might well surprise investors again – but this time positively instead.

Inflation is the rate at which prices change on a year-on-year basis. As the base effect will become more favorable, and due to a sharper than expected drop in goods prices, US inflation might come back down to surprisingly low levels.

However, this drop might prove to be short-lived. As in the 70s (see chart below), structural factors and a Fed policy mistake (aka premature pause in the tightening cycle) could prompt a new inflationary wave in the years that follow.

Inflation today vs. 1970s

Source: Bloomberg

Surprise #2 —

QE for the markets, rate hikes for

everyone else

[Probability: High]

While global economic growth and inflation might both surprise on the downside, the Fed could initially be reluctant to pause its rate hike cycle. In other words, they might over-tighten. Consequently, equity and bond volatility could jump in the first half of the year, with the risk of triggering financial accidents.

For instance, G7 countries could face a buyer’s strike for their claims, as international investors might be reluctant to get low or negative real rates for bonds issued by highly indebted countries. Similar to the UK, the Fed (and the ECB) would initially refuse to stop hiking. But with the spike in long-term bond yields, they would have no other choice than to re-launch QE (Quantitative Easing), targeting the long-end of the curve. In other words, they would be resorting to QE to save financial markets while hiking rates for everyone else.

Surprise #3 —

A housing crash of epic proportions

[Probability: High]

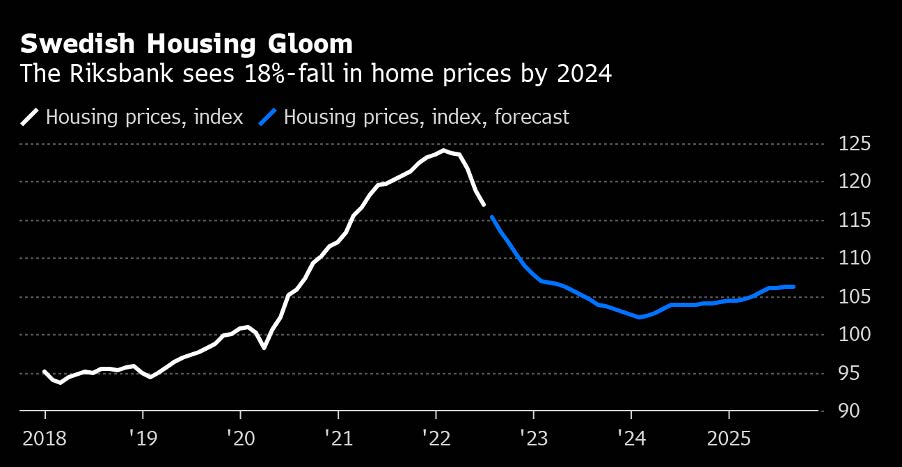

2022 saw the burst of several bubbles (bonds, equities, cryptos). In 2023, real estate could be the last shoe to drop. Indeed, the tightening of the monetary cycle is hitting the interest-rate sensitive part of the economy the most. Countries with a high percentage of variable rates mortgages could endure a double-digit decline of housing prices. Sweden, a country where nearly 70% of the mortgages have variable rates, could face a double-digit decline in housing prices according to the Riskbank.

Swedish housing gloom

Source: Bloomberg

Surprise #4 —

A (temporary) come-back of the 60/40

[Probability: Medium]

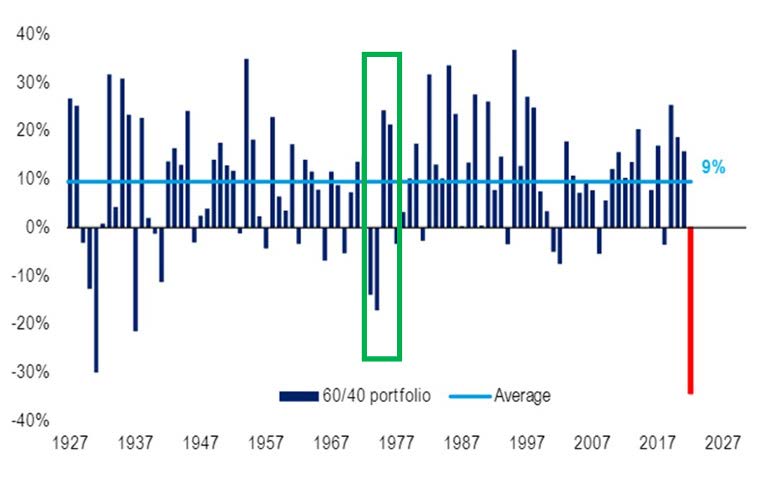

2022 was an “annus-horribilis” for the 60/40 (stocks-bonds) portfolio, as both equity and fixed income markets strongly correlated on the downside. 2023 could see a turnaround in both markets. After another volatile semester (1H 2023), a pause by the Fed and attractive valuations could lead investors to come back to equity and bond markets. Multi-assets portfolios would then enjoy a massive rally and record one of their best years ever. This would be similar to what happened in the 70s (see red box in the chart below).

In 2022, the “60/40” portfolio annualized return is the worst in the past 100 years

Source: BofA Global Research

Surprise #5 —

China (sanitary) pivot… or not

[Probability: High]

China’s zero-covid policy has had a disastrous impact on growth in 2022 and has triggered a wave of protests. Beijing is now at a tipping point, which could lead to two tail risk outcomes:

Positive outcome: Beijing finally decides to change its economic and monetary policy. Zero-covid restrictions get progressively lifted. Regulations for technology, gaming and education sectors become more supportive. Significant fiscal and monetary stimuli are injected into the economy. Relationship with Washington progressively improves. On the back of these tailwinds, Chinese equities become the best performing asset in 2023 and the yuan rallies.

Negative outcome: China experiences protests reminiscent of Tiananmen. Human casualties rise to the point where the West decides to apply sanctions and cut some ties with China. The global supply chain is severely disrupted and leads to upward pressure on inflation and downward pressure on growth. The Yuan crashes and stems a wave of competitive devaluation in China. Risk assets tumble globally.

Surprise #6 —

Dollar drops; Emerging Markets and

European assets outperform

[Probability: Medium]

2022 has again been favorable to US assets (dollar, US stocks). At the time of our writing, US now accounts for 70% of the MSCI World and non-US assets remain massively under-represented in global portfolios.

In the case of a favorable macro-economic and liquidity scenario (the Fed pausing, China re-opening and the global economy avoiding a deep recession), the dollar could end its two-year bull market while the Euro, the Yen and Emerging Market currencies would enjoy a spectacular rally. For once, European, UK and Emerging Market assets would outperform the US.

US stocks are relatively more expensive than international equities

Source: Edward Jones

Surprise #7 —

Iraq collapse in H2 leads to another spike in oil prices

[Probability: Low]

The war in Ukraine is entering stasis. The support for war is ebbing on all sides and the market is slowly moving into indifference (although the human cost of the war must never be dismissed). But the real danger to oil supply in 2023 likely won’t come from Russia’s war in Ukraine, but Iraq’s instability. A big geopolitical surprise could be if Iran and Saudi Arabia enter into conflict over Iraq. That is where oil supply loss would happen. With dramatic consequences on oil prices.

Surprise #8 —

Commodities are the best asset class

again. Gold shines

[Probability: High]

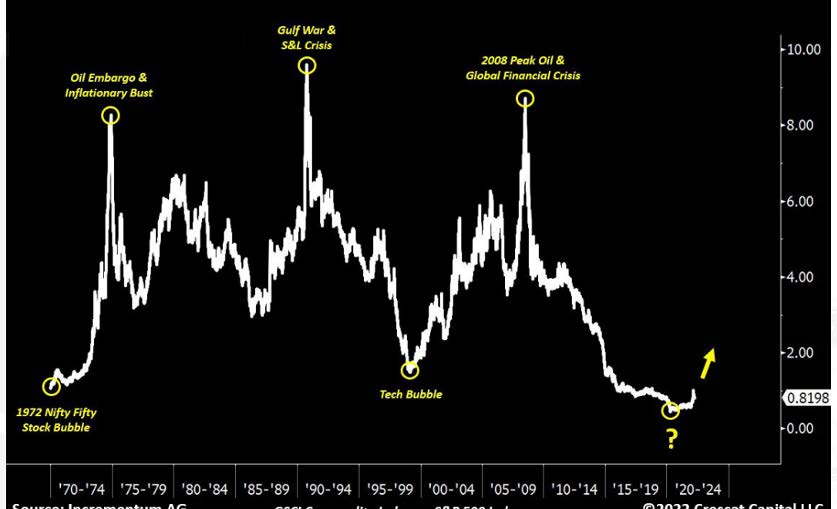

While commodities are the best performing asset class in 2022, fund flows have been negative and it remains massively underrepresented in global asset portfolios. With a potential spike in oil prices in the second half of the year and the drop of the dollar, commodities could record another spectacular year as asset allocators finally decide to include commodities in global portfolios. Precious metals (Gold, Silver) would surge on the back of a weakening dollar and declining real interest rates (due to the rise of long-term inflation expectations). Commodities’ relative performance against equities tend to last several years in both directions (up and down). We might be at the start of a secular upward trend for commodities’ relative performance.

Commodities to equity ratio

Source: Crescat Capital, Bloomberg

Surprise #9 —

Bitcoin hits $40k

[Probability: Medium]

After a dreadful 2022, the recovery of risk assets, the decline of the dollar and significant regulatory improvements could lead Bitcoin to more than double its current price. Meanwhile, thousands of cryptocurrencies would not survive the 2022 crypto-winter and disappear.

Surprise #10 —

The fall of an icon

[Probability: Low]

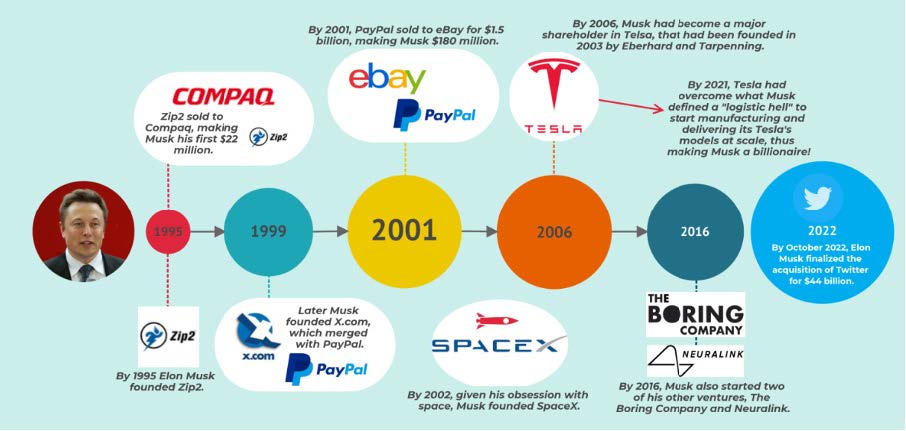

In a very surprising development, the Twitter turnaround story fails as thousands of companies start to boycott the social media platform. Elon Musk would then be forced to sell Tesla stocks to finance another rescue of Twitter, which would ultimately fail. Markets might then start to lose faith in Elon Musk, leading to a demise of his empire.

The Elon Musk entrepreneurial story

Source: Four-week MBA