.png)

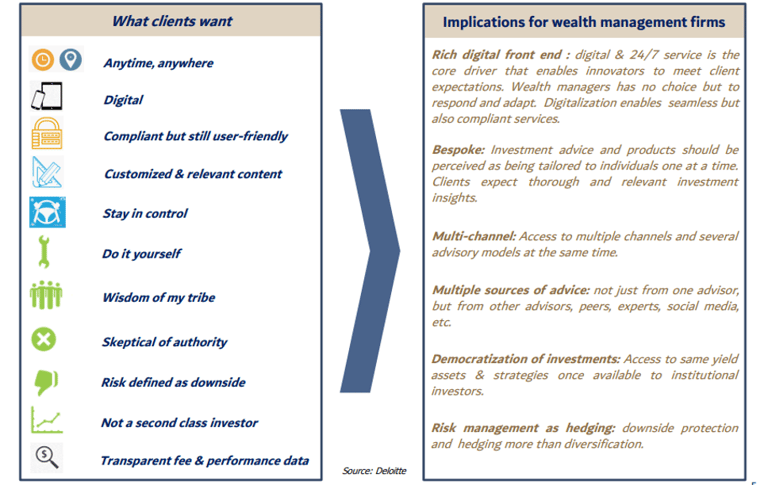

What clients want

The needs of private customers have changed significantly in recent years. Most of them want to receive information anywhere, anytime, with just a few clicks. They understand the regulatory constraints but want the smoothest possible client experience - from the account opening process to the monitoring or their positions. When it comes to investment advice, the content must be personalized and consistent with the client's specific needs. The banker is no longer seen as the only competent source for advice and management: many clients want to keep control of their investments and want access to different sources of advice. Most private clients - including those in the "affluent" segment - no longer want to be treated as "second-class" investors.

They demand access to complex solutions that were once reserved for institutional investors (venture capital, private debt, real estate, structured products, etc.). Performance and fees must be transparent.

This evolution of needs has important implications for banks and asset management companies. A 24/7 digital interface is becoming a necessary tool to serve them and meet their expectations. Investment recommendations must be perceived as being as targeted as possible. Advice must be provided through different platforms (blogs, messaging, email but also live) and come from various sources (social networks, specialized websites, webinars, experts, peers).

We are now talking about democratization of investments in order to give everyone access to sophisticated investment strategies and products. Risk management involves the use of downside protection instruments rather than simple portfolio diversification.

––––––––––

Client needs are evolving and have deep implications for wealth management firms

Source: Deloitte

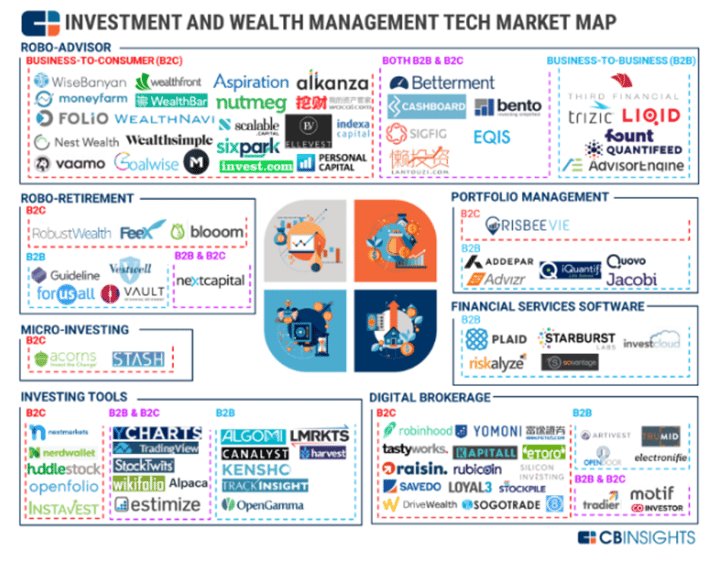

The Wealth management industry is being disrupted from different sources

Banks are facing the arrival of new entrants and business models. Fintechs have the advantage of offering streamlined value propositions, being cheaper and faster.

––––––––––

Fintechs are growing their market share as they focus on being better or cheaper or faster, and doing one thing and only one thing

Source: CB Insights

On the banks' side, growing regulatory constraints are slowing down the decision making process. Overall, operating and customer acquisition costs are rising due to the high price of IT tools, growing administrative burden and the race for talent. Of course, the current market environment (stock and bond collapse, rising inflation, etc.) further complicates the equation. Demographics also matter: young graduates are less and less attracted to banks. Longer life expectancy means that retirees are more likely to remain very active on their accounts. As for the new generations, their investment preferences are changing (sustainability, cryptos, etc.). Finally, new technologies (artificial intelligence, "big data", advanced analytical tools, etc.) are revolutionizing the wealth management industry with the arrival of "robot advisors".

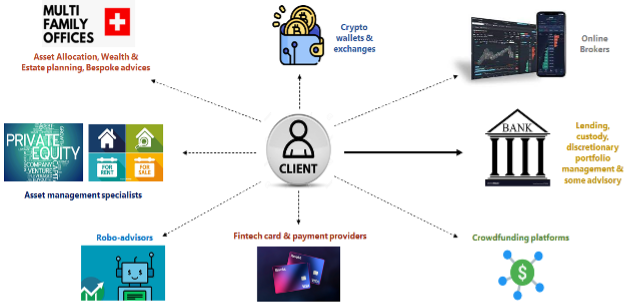

For banks, there is an urgent need to react as clients are increasingly turning to other platforms. Often, private clients have access to online brokers, a Revolut card, an account with a crypto-currency specialist (exchange and/or wallet) and investments through crowdfunding and crowdlending platforms. As for real estate and venture capital, they prefer direct access to specialized managers. For the wealthiest among them, it is good practice to use the services of a multi or single-family office. What is left for the bank, then? The traditional services of custody, advisory and discretionary mandates. Much of the value added (and therefore fees) is de facto generated outside of the traditional banking platforms.

––––––––––

Traditional banks are losing market share to new platforms

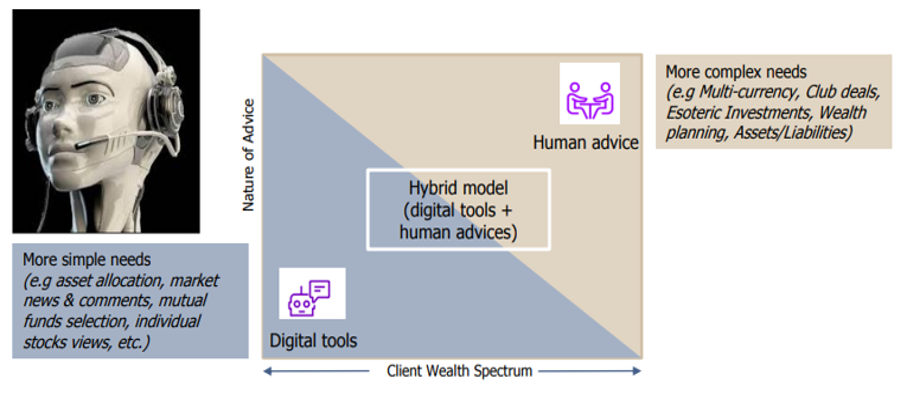

Robo--advisor versus human advisor

One of the avenues favored by banks is the digitalization of processes and customer experience. The temptation is great to switch advisory services to a robo-advisor solution. But beware, both the traditional model (based on the human relationship) and the purely digital solution have their advantages and disadvantages.

Traditional advisory model

Human intervention allows for tailor-made financial planning, to better measure the emotional dimension of clients, to preserve a privileged client relationship and to present sophisticated solutions.

However, this model has its limitations: it is relatively expensive and not very scalable. The high fees associated with it limit its application to "small" accounts. It is not suited to the new generation and to clients who want a digital experience.

Robo-advisor

This model has the advantage of being scalable, unlimited by time and geography, and in line with regulations while providing a good client experience. It facilitates "Do-It-Yourself" and allows for promotion and communication across multiple channels. It can be offered with little or no minimum amount and fees.

Among the disadvantages: the services offered have to be standardized and sometimes feel second rate. They also leave no room to mitigate the emotional dimension of a potentially rash decision by the client. Last but not least, the robots have not been tested during real bear markets.

The hybrid investment advisor model

Neither of the two models described above can be considered perfect. The solution is therefore a so-called hybrid platform, i.e. mixing a digital platform with human intervention.

A hybrid advisory model has a human advisor as a key selling point although the user has the possibility to manage his/her investments on the go via apps. Usually this model uses blogs as a mean of educating clients on hot economic and financial topics and also to raise awareness on how the service differentiates itself from the traditional financial services sector.

The advisor remains essential at the beginning of the relationship and when it comes to covering certain higher value-added services (financial planning, specific questions about the account, complex investment solutions). For certain services (market news, fund selection, views on specific securities and sectors, performance and views on account positions) purely digital access is sufficient.

The hybrid model is particularly suitable for risk profile analysis, asset allocation models, portfolio management, sending targeted investment recommendations, financial education, tax reporting, etc.

––––––––––

The Hybrid Advisor

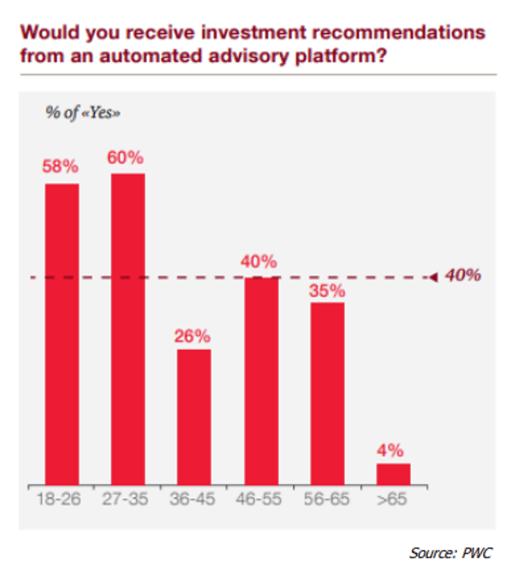

The core existing wealth management business is not yet seeing a lot of this disruption because of the traditional high net worth individual (HNWI) clients are NOT demanding so much change.

Rather, we are seeing the normal trajectory of disruptive changes that comes first from those excluded from the old way of doing things.

However, even in this core market, the demographic time bomb (when the wealth transfers to the digitally native next generation) is ticking (see chart below). Most traditional players now need to adapt their strategy and prepare for this.

––––––––––

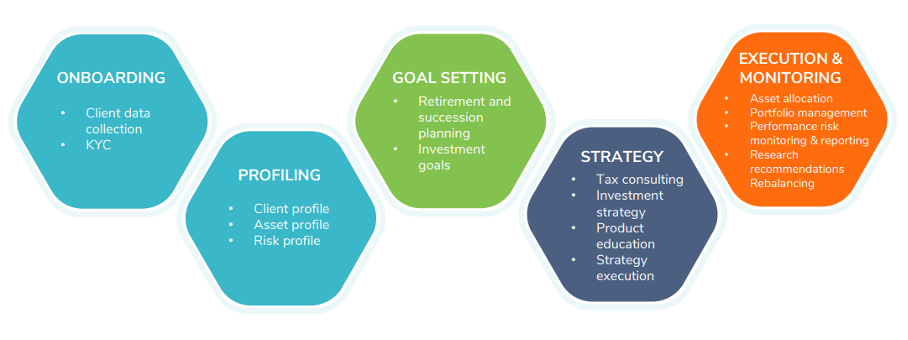

The future of advice will be digital

Good news for banks: the arrival of new technologies should facilitate the digitalization of many services. Artificial intelligence, big data, blockchain and robotic process automation allow for the (partial) automation of services such as onboarding, client risk profile analysis, investment strategy, and position execution and monitoring.

––––––––––

New Technologies such as Big Data, Artificial intelligence, Blockchain and robotic process automation can be applied across the Wealth Management value chain

The fact that technology is needed more than ever to serve clients means that traditional private banks will compete head-on with fintechs. But there is more good news for banks: it is in most cases easier for a bank to integrate fintech tools into its infrastructure than for a fintech to obtain a banking license, which remains a major entry barrier.

––––––––––

FinTechs are becoming banks while banks are acquiring FinTechs. Yet, it’s significantly harder to be a well-run bank than have a good app.

The future of investment advisory

With their first-mover advantage, private banks will be able to evolve their business model in the following way.

Value proposition -> an offer centered on clients' needs and delivered through a hybrid (human/digital) and holistic platform (all asset classes and products).

Regulation / compliance -> the investment portal will become more and more self-directed. Take for example the platforms giving access to solutions reserved for qualified investors (direct purchase of real estate). Once the client profile is filled in, the user can go and consult the product offer without the advisor having to check if the solution fits the client's risk profile.

Investment products and solutions -> it is no longer a question of offering standard solutions (shares, bonds, funds) but of widening the spectrum to differentiated investments. We are now talking about open platforms and ecosystems that allow clients to access solutions from third parties belonging to the traditional world (asset managers) as well as fintech (crowdfunding) and new asset classes (cryptocurrencies). The sources of advice are multiple (owners but also social networks, experts, other customers, etc.) and can be shared via blogs, apps, etc.

Target customers -> it's not just about covering existing customers but using the bank's visibility and membership in an ecosystem to attract new customers and assets held outside the bank.

Interface -> access to the bank account, information and recommendations must be digital and 24/7

Fees and commissions -> while billing based on transactions and assets under management should remain, a "freemium" model could be gradually introduced. The idea is to attract potential clients through a first experience (blog, information) without a fee. Then, a certain number of bespoke services can be offered through a progressive price scale (silver, gold, platinum).

Team and organization -> banks need to adapt the structure of their departments and staff around key functions. IT and digital profiles are gaining in importance as it is imperative to create the best possible digital experience. Investment experts perform selection and due diligence of complex and differentiated investment solutions. External platforms and skills are integrated into the offering. Consultants continue to interact with clients in addition to the digital interface.

––––––––––

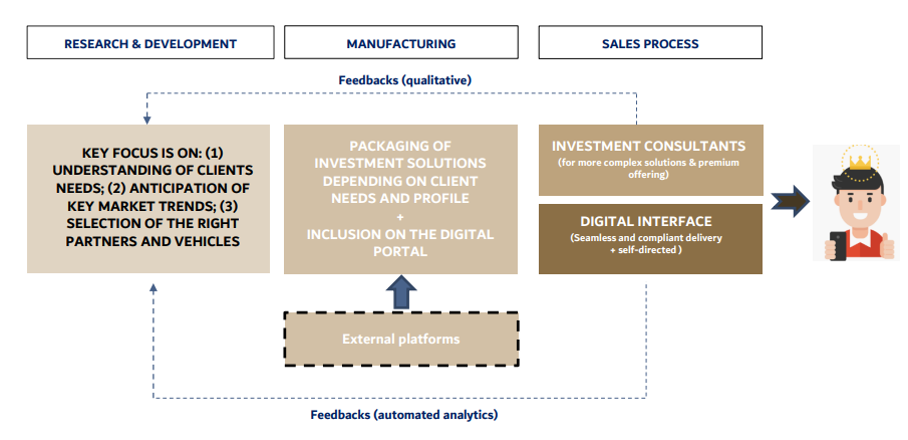

From R&D to client interaction

Conclusions

The new face of wealth management marries human and artificial intelligence. The basic idea behind the hybrid model is to retain the high level of personalized advice that most clients value from their financial advisor while leveraging the power of digital communication and new technologies.

In this model, advisors must work with digital platforms to simplify parts of the advisory process, but they still provide the personalized services that clients demand.

In other words, the hybrid model does not mean the automation of wealth management. Nor should it be confused with a high-end "call center" or "small" client advisory service. Rather, it is an integrated financial services delivery model that offers an augmented value proposition to private banking clients.

This mix should not only improve the client experience but also the profitability of traditional private banks. But while incumbent wealth managers are aware of the urgency to evolve their advisory services, very few have yet been able to adapt to meet new client needs and expectations. There is therefore a unique opportunity for private banks to differentiate themselves by being more innovative and faster to transform.