.png)

Source: Tesla

Source: Tesla

The development of autonomous driving technologies relies on a few core technologies that are each crucial to enabling vehicles to navigate their environment entirely without human intervention. These crucial technologies include sensors, artificial intelligence, and high-definition mapping.

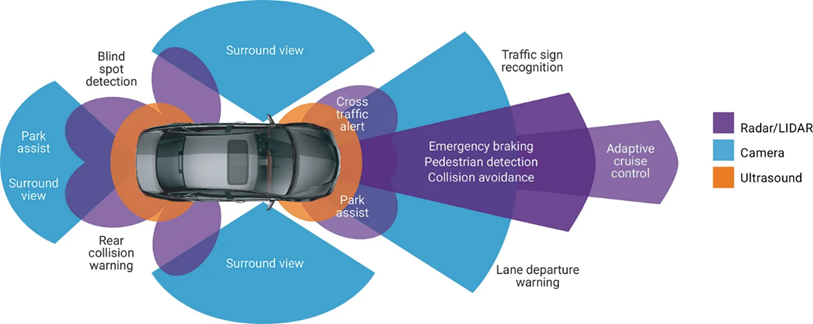

Sensors, which provide the vehicles with real-time data about their surroundings, are central to autonomous driving. The three main types used are LiDAR, radar, and cameras. LiDAR creates highly accurate 3D maps of the surroundings with the use of laser beams, which allows the vehicles to detect objects at long distances under various lighting conditions. The precision of LiDAR is unmatched, an advantage that also comes with a heavy price tag. However, the technology isn’t bulletproof and can still struggle in adverse weather like a heavy rainstorm or fog. While radar is more affordable and functions reliably in all weather conditions, its resolution is lower, making it harder to distinguish fine details. Cameras on the other hand provide high resolution images that are crucial for identifying visual cues like lane markings and traffic signs.

While they are cost-effective, they also depend on lighting conditions, which makes them less reliable in low light environments or adverse weather.

Source: Eetimes

Each player in this space has chosen to adopt a different combination of these technologies. Waymo, a subsidiary of Alphabet, is widely regarded as the current leader in this field with its sensor-heavy approach that integrates LiDAR, radar, and cameras to provide several layers of data. Implementing this variety of sensors ensures the vehicles can operate safely even when one sensor becomes unreliable. This approach, however, comes with significantly higher costs. The expensive LiDAR systems might give them a head start in this race, but they also make it challenging to scale this technology to mass-market vehicles with an affordable price tag. The company has already launched fully autonomous Robotaxis in a handful of cities like Phoenix, LA, and San Francisco.

Another major player in the US is Cruise, the autonomous driving subsidiary to General Motors, which has opted for a similar path as Waymo, leveraging all three sensor technologies to emphasize safety.

Tesla, in true Tesla fashion, has decided to take a radically different approach. The company has chosen to forgo LiDAR altogether and instead rely on a vision-based system that uses cameras as its primary sensors, complemented by radar. The company’s full self-driving (FSD) system uses AI to process the visual data in real time and make driving decisions based on what the cameras see. This approach is far more cost-effective than that of its rivals as cameras are significantly cheaper than LiDAR systems. Another advantage for Tesla is that the company benefits from already having millions of vehicles on the road equipped with FSD hardware, allowing them to collect huge amounts of driving data, which is a key asset in refining its AI systems.

However, Tesla’s cost-effective approach is not without its setbacks. As previously mentioned, cameras are highly dependent on lighting and weather conditions. Additionally, lacking the depth perception offered by LiDAR means that Tesla’s system may be less reliable in handling complex scenarios such a crowded intersections or obstacles in low visibility. Their belief is that their AI systems will eventually overcome these limitations through continuous learning and remote software updates.

Furthermore, in addition to all the on-board sensors, connectivity will play a key role in enhancing the cars’ capabilities through IoT integration. Connected vehicles will be able to communicate with each other as well as with infrastructure like traffic lights and share real-time information on traffic patterns or roads hazards. This connected network is often referred to as “vehicle-to-everything” communication. Players like Google who already have extensive mapping data and IoT expertise will likely have a significant advantage in building a highly efficient robotaxi ecosystem.

Source: Not a Tesla App

Source: Not a Tesla App

For Tesla, on the technological side, the key advantage lies in its ability to mass-produce autonomous vehicles on a scale that few competitors can yet match. On the other hand, on the ride-hailing front, companies like Uber, Lyft, and DiDi, currently benefit from their extensive networks of drivers and highly adopted applications, which allow them to aggregate demand and provide higher vehicle utilization rate. Following Tesla's Robotaxi event, the company’s shares fell 10%. In contrast, Uber’s stock surged by around 9%, while Lyft saw a near 10% gain. As a side note, Tesla's stock had surged more than 20% last Thursday, largely due to its operating performance as an auto OEM rather than for autonomous vehicle developments.

Uber initially ventured into autonomous vehicle development with Volvo in 2016 but abandoned the effort in 2018. Since then, Uber has focused on expanding its rider-driver network, creating a platform that efficiently connects riders with nearby drivers. Uber benefits from a capital-light business model acting as an intermediary without owning cars or employing drivers directly, allowing it to scale easily and reduce costs when demand fluctuates.

To integrate AVs, Uber is partnering with companies like Cruise, Waymo, and Wayve, a UK AI start-up for AVs. Starting in 2025, Cruise will supply Uber with self-driving Chevrolet Bolts. Similarly, Uber plan to expand Waymo’s autonomous ride-hailing service to Atlanta and Austin, with Waymo’s all-electric Jaguar I-PACE vehicles available through Uber's app. Uber will handle vehicle cleaning and repairs, while Waymo will manage operations and testing. Uber is also eyeing AVs from BYD, following their July 2024 partnership. This multi-year deal plans to bring over 100,000 new BYD electric vehicles to Uber's platform, some featuring self-driving capabilities.

DiDi, the Chinese ride-hailing company, is entering the AV space through a joint venture with GAC Aion to produce Robotaxis by 2025. Their collaboration aims to launch fully autonomous Level 4 vehicles for DiDi's ride-hailing service.

Source: Arthur D. Little analysis

Source: Arthur D. Little analysis