.png)

Charles-Henry Monchau

Chief Investment Officer

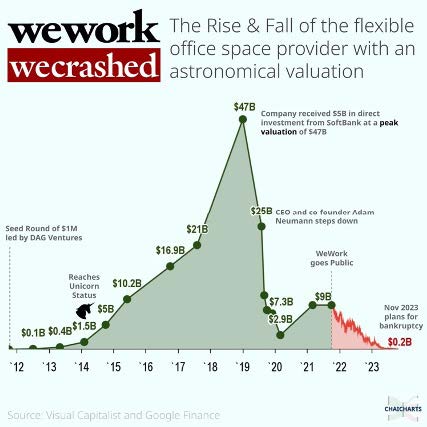

Founded in 2010 by Adam Neumann and Miguel McKelvey, WeWork initially positioned itself as a disrupter in the office space sector. The company offers short-term rental solutions for collaborative workspaces to individuals and companies. WeWork's offices are characterised by a vibrant yet relaxed atmosphere, with bright, modern décor, and the unique offer of unlimited (!) alcohol in its offices. WeWork has deliberately positioned itself as more than just a provider of cheap office space and technology, but as a company striving to fulfil a "mission" to "raise the consciousness of the world". In 2019, Masayoshi Son's SoftBank valued WeWork at $47 billion, sparking an unprecedented buzz around the company.

However, signs of trouble began to appear as WeWork prepared for its 2019 IPO. In urgent need of funds, the company sought to go public that year. Nevertheless, the IPO was halted due to governance issues and poor financial performance within the company. This led to Mr. Neumann's resignation as CEO, following criticism of his unconventional management style. SoftBank stepped in and took WeWork public in 2021 with a valuation of $8 billion.

The restructuring plan will also enable WeWork to reduce its portfolio of office leases. Tenants should see a strate-gic rebalancing of the company's office lease agreements. WeWork has defined a comprehensive lease rejection plan aimed at optimising value and operational efficiency, spe-cifically targeting leases deemed "largely non-operational". This intentional approach also serves as leverage to negoti-ate more favourable terms for retained leases. Although the specific offices to be retained remain uncertain, WeWork has communicated advance notices to relevant members in cases where lease rejection is being considered.

For tenants outside the USA and Canada, WeWork is commit-ted to business as usual. Franchises worldwide are expected to operate as usual in the majority of the more than 700 loca-tions worldwide and around 730,000 members.

In addition, a recent study by Market Reports World estimates the current value of the coworking space market at $19 billion and forecasts an annualised growth rate of almost 17% to 2028. Mark Dixon, founder of IWG, WeWork's competitor, points to the acceleration of his company's global growth due to the rise of hybrid working trends.

"Today, companies of all sizes are terminating their long-term commercial leases and replacing them with shorter-term agreements with flexible workspace providers such as IWG," said Dixon (DW).

"Today, companies of all sizes are terminating their long-term commercial leases and replacing them with shorter-term agreements with flexible workspace providers such as IWG," said Dixon (DW).

The Swiss-headquartered company, which enjoys an exten-sive global presence with almost 3,500 sites in over 120 countries, reached a historic milestone by posting the highest quarterly sales in its 30-year history on Tuesday, November 7, 2023. Dixon has confirmed that the company is actively studying the possibility of acquiring additional premises from WeWork. This strategic move demonstrates IWG's interest

in expanding its presence and potentially capitalising on the challenges facing WeWork.