.png)

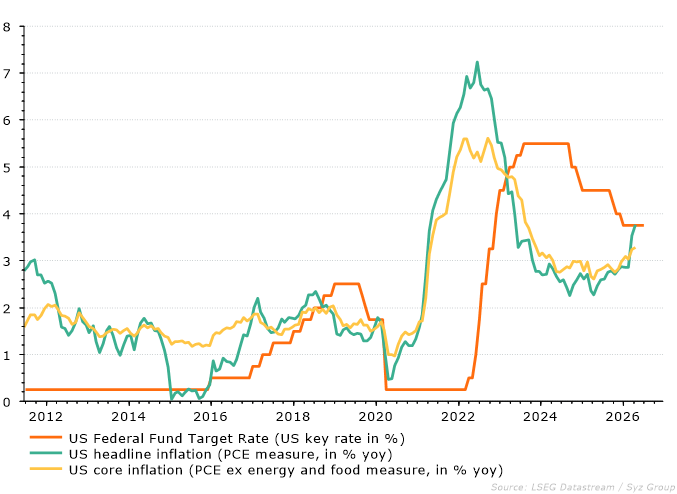

- The first FOMC meeting under Chair Warsh kept rates unchanged at 3.50%-3.75%, but marked a clear shift in Fed communication. The statement was much shorter, removed forward guidance and no longer included the previous “easing bias”.

- The policy tone was somewhat more hawkish, mainly because of the dot plot and the inflation message. Warsh did not submit his own dot-plot forecast, but nine of eighteen Fed officials now see a rate hike in 2026, while Warsh strongly reaffirmed the Fed’s commitment to the 2% inflation target and that it was missed during the last 5 years.

- Warsh announced an institutional review of the Fed through five new task forces. These will cover communication, the balance sheet, data sources, productivity and jobs, and the inflation framework, suggesting a broader rethink of how the Fed analyses and conducts policy.

- On the balance sheet, there was no immediate reduction announced. Instead, Warsh launched a review of the balance sheet and the composition of the Fed holding, but confirmed for now the ample-reserves regime. This makes the signal strategic rather than operational.

Many changes in communication and style, but key rates remain stable for now

The FOMC left rates unchanged at its June meeting, keeping the federal funds target range at 3.50%-3.75%, as expected by us and by markets. The first decision under new Fed chair Kevin Warsh was unanimous, with no dissenting votes. The monetary policy statement removed forward guidance and no longer includes an “easing bias”. It was also shortened significantly, from more than 340 words to only around 130 words.

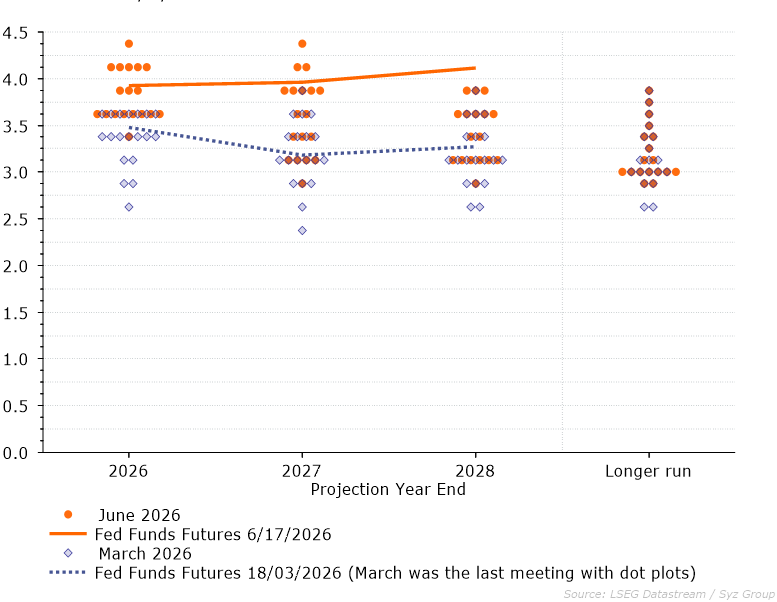

Another clear sign that Warsh wants to change the Fed’s communication strategy was his decision not to submit a dot-plot projection. He confirmed that he had abstained from providing his own rate forecast. This reflects his long-standing scepticism about the current format of the Summary of Economic Projections. At the same time, he made clear that he encourages his fellow FOMC members to continue providing their projections for growth, inflation and key rates, in line with long-standing practice. Interestingly, the most important market signal seems to have been the shift in the dot plot. Nine of the eighteen Fed officials submitting forecasts now see a rate hike in 2026, while the median projected policy rate moved substantially above the latest dot-plot-range from March.

The shift towards a more hawkish FOMC rate outlook is clearly visible in the dot plot when compared with the March dots

An institutional reset at the Fed, but with a strong commitment to keep the 2% inflation target

The much shorter statement already pointed to a change in communication. The press conference then marked a broader institutional reset at the Fed. Warsh announced five task forces covering communications, the balance sheet, data sources, productivity and jobs, and the inflation framework. This suggests that he wants to review not only policy settings, but also how the Fed analyses the economy and communicates its decisions.

Does the first meeting under Warsh imply a hawkish shift at the Fed?

The inflation message seemed to be deliberately firm. Warsh reiterated that the Fed remains committed to the 2% inflation target. He also said there is no reason to reconsider that target before the Fed has re-established its ability to deliver it. Warsh emphasised that the commitment to price stability is “strong, unanimous, and unambiguous”. He added that this message had been missed over the past five years and now needs to be fixed. The shortened policy statement noted the balanced labour market and the solid pace of economic activity, despite elevated uncertainty partly linked to the situation in the Middle East. On inflation, the statement was clear that it remains above the 2% target and that this only partly reflects the supply shock from the Middle East crisis. The statement ends by confirming that “the Committee will deliver price stability.”

Any news on future action regarding the Federal Reserve’s balance sheet?

Warsh did not announce an immediate cut in the Fed’s balance sheet. Instead, he announced a task force to review the balance sheet, the ample-reserves regime and the composition of Fed holdings. The official implementation note still maintains ample reserves. It even allows Treasury-bill purchases when needed to support reserve levels. The signal is therefore strategic rather than operational. Balance-sheet reduction may become a major theme under Warsh, but today’s meeting launched a review process, not a new quantitative-tightening programme. This is important for investors, as older Fed attempts to reduce the balance sheet show that patience is clearly needed. In 2019, the Fed had to halt such an attempt, conduct three ad hoc rate cuts and finally restart temporary liquidity injections into financial markets. A recent study by the Dallas Fed concluded that a balance-sheet reduction of USD 1.2 trillion to USD 2.1 trillion could be achieved through regulatory, supervisory and operational changes to the Fed’s framework. Most importantly, these changes would allow and incentivise US banks to hold more government debt and help the Fed lower its balance sheet. Such regulatory changes require a majority of the seven governors on the Fed Board. This could make former Chair Powell’s position important, as he still sits on the Board as a regular governor. He could become the decisive vote, as the other six members appear rather split: three governors, including new Chair Warsh, seem to be in the pro-deregulation camp, while the other three appear to favour keeping the current regulatory set-up.

How did financial markets react?

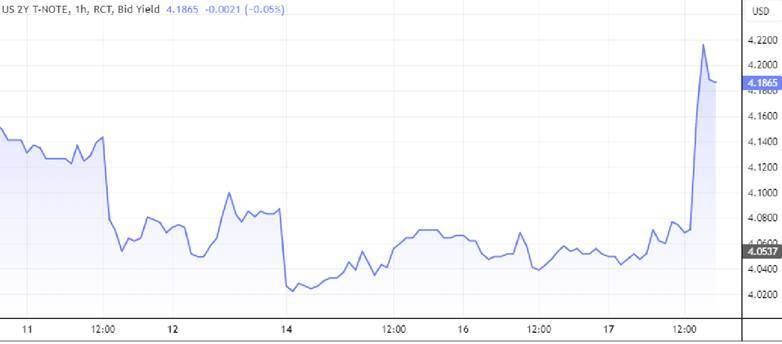

Market pricing moved in a more hawkish direction after the meeting. Traders moved towards pricing a full rate hike as early as October. Before the meeting, markets had not expected a full hike by December. This was reflected in short-term rates, which rose significantly during the meeting.

US short-term rates jumped during the press conference (2-year Treasury note yield)

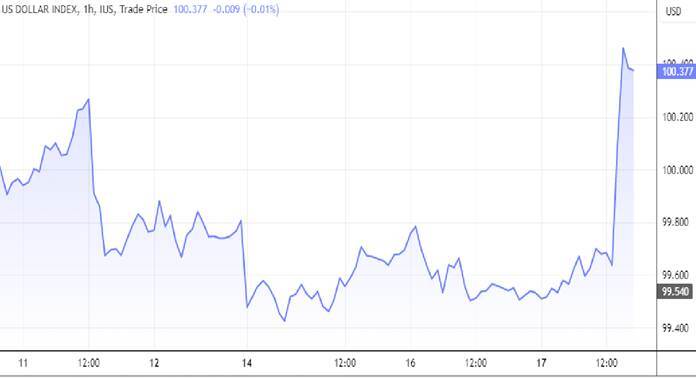

This led to an initially negative reaction in US equities, with stock prices falling, while the US dollar appreciated quickly. The more hawkish tone now points to a wider positive policy-rate differential for the US dollar versus other major currencies, such as the Euro, Yen, British pound and Swiss franc.

A strong and swift appreciation of the trade-weighted US dollar index

How independent from political influence will the Fed be under Chair Warsh?

The political dimension remains sensitive. Warsh avoided saying whether he had spoken with President Trump since taking the Fed job, while acknowledging regular contact with Treasury Secretary Scott Bessent. Many commentators framed this as an early test of how Warsh balances White House trust with Fed independence. So far, at least, the words of Warsh and President Trump point in that direction. Trump has said in recent days that Warsh should “do whatever he wants” and be “totally independent”, even though the President and some of his advisers continue to call for lower interest rates.

Bottom line: risks of a rate hike in H2 have risen again, but we stick to our view of unchanged rates in 2026

For markets, the key takeaway is that Warsh’s Fed looks less inclined to pre-commit to any action or policy path. It has also abandoned the former “easing bias”. The unchanged rate decision matters less than the signal from the dot plot. The Fed may keep policy unchanged, or even tighten further, if inflationary pressures do not abate sooner rather than later. Risks for higher key rates have clearly shifted to the upside and markets now expect a first hike in October.

At the press conference, Warsh emphasised how balanced the US economy is. The labour market is solid but not too tight. Stronger productivity growth helps to contain inflation. Consumers are being hit by higher prices, including energy prices, but so far this has been largely offset by wage gains. We expect the large tax refunds to fade in H2 and higher prices to weigh on domestic demand. Tensions in the Middle East have eased and we forecast oil prices to remain low over the coming quarters after falling closer to levels before the Iran war started. This should significantly reduce the inflationary pressure from energy prices and give the Fed time to keep interest rates unchanged in 2026. This is in line with the timeframe in which the new working groups are due to present their findings and until the Mid-term elections from November are over.