.png)

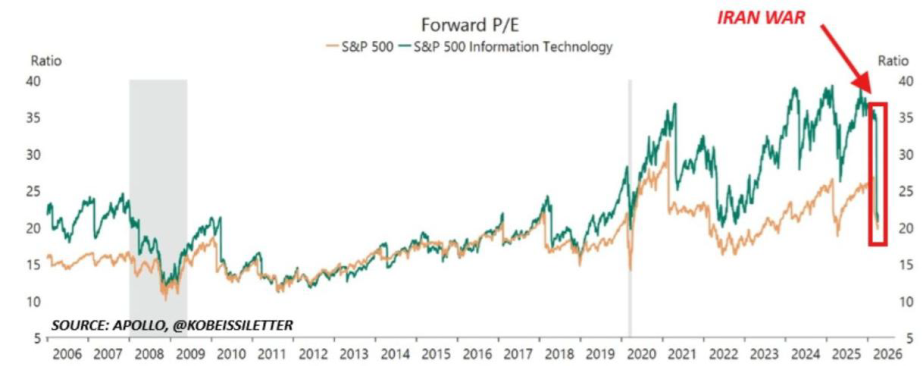

Tech Valuations Back to Pre-AI Boom Levels

Source: Apollo

We are sorry that for legal reasons we are not able to help US citizens or Canadian residents other than in Ontario, Quebec, or Alberta. Best wishes for the future…

We are sorry that for legal reasons we are not able to help US citizens or Canadian residents other than in Ontario, Quebec, or Alberta. Best wishes for the future…

You chose the following profile. If you made a mistake, please change here USA

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material.

This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor.

This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other

Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

Tech Valuations Back to Pre-AI Boom Levels

Source: Apollo

Global markets

Global equity markets staged a powerful and broad-based advance last week, with the MSCI All Countries World index gaining 4.2% in USD. The defining event was the announcement mid-week of a two-week humanitarian and diplomatic ceasefire between the United States and Iran. This single development reshaped the investment landscape in a matter of hours, sending oil prices into one of their steepest single-day declines since 2020 and triggering a decisive rotation out of the defensive and energy positioning that had dominated portfolios since the conflict began. Airlines, consumer discretionary, and technology names were among the principal beneficiaries, while energy and defence stocks gave back part of their conflict premium.

The macro backdrop was also supportive: March CPI printed at 3.3% year-on-year - elevated, but driven almost entirely by a 21.2% surge in gasoline prices. With core CPI rising a contained 0.2% month-on-month and 2.6% year-on-year, markets correctly concluded that the Federal Reserve retained the analytical cover to remain on hold without tightening, and equities absorbed the data constructively. The most striking feature of the week was the leadership of emerging markets, which surged 8% in USD, their best weekly return in years, as the regions most damaged by the conflict saw the sharpest reversal.

US

The S&P 500 rose 3.6% for the week. The Nasdaq Composite outperformed as the ceasefire-driven improvement in the global growth outlook revived demand for riskier stocks that had been under disproportionate pressure during the weeks of peak uncertainty.

The best performing sectors where Semiconductors (which rallied nearly 14%), as well as other high beta / cyclical sectors such as Metals&Mining (+8%) or Banks (+6%). On the flipside - Energy underperformed (-4%) as the high oil prices that had supported them for weeks partially reversed. The worst performing pocket of the market was Software, which dropped -7%, driven by the newsflow coming out of the AI start-up space (Anthropic new model release fed the existing fears of software disruption).

The week's CPI data, while generating an eye-catching headline, reinforced rather than undermined the equity rally: the subdued core reading of 2.6% year-on-year provided the narrative that the inflation spike was primarily energy-driven and likely transitory. The prevailing view appears to be that the Fed was likely to "look through the energy-driven noise" provided the ceasefire held. Fed funds futures shifted modestly to price a marginally higher probability of a cut later in the year.

Europe

European markets advanced solidly, with the STOXX Europe 600 rising 3.1% in Euro terms. The DAX was among the stronger performers within the region, as German industrials — disproportionately exposed to energy input costs — rebounded on oil price relief. The CAC 40 similarly recovered, led by luxury goods and globally-oriented multinationals that benefit from improved growth expectations. The FTSE 100 lagged at +2.4%, a reversal of its outperformance in the prior week that is directly explained by its heavy energy weighting: the sharp fall in oil prices became a drag. The Switzerland SPI added 2.0%, with the defensive quality of its healthcare and consumer staples heavyweights providing ballast against residual uncertainty while still participating in the broader risk-on move.

The macro backdrop, however, remains challenged in Europe. The EU's Economy Commissioner flagged an impending downward revision to the eurozone's 2026 growth forecast, warning of a stagflationary shock. The OECD maintained its lowered eurozone growth projection of 0.8% for the year. These concerns did not derail the week's equity gains but they represent an important structural overhang heading into the second quarter.

Rest of the world

The transformation in emerging market performance last week was dramatic. MSCI EM returned +8.0% in USD — strongest weekly gain in several years — as the ceasefire triggered a wholesale reversal of the forces that had most damaged EM assets since the conflict began.

The tech heavy equity markets such as South Korea and Taiwan led the region. Both continued from the ongoing demand for datacentre hardware, and in the Korean memory chip companies, the rebound was additionally helped by the positioning which had cleared significantly during March. On the other hand Chinese equities remained a relative EM-laggard, though they too posted positive returns during the week. MSCI China gained +3.1% and domestic A-shares indices rose 4–5%, stronger interest in growth and technology names as global risk appetite recovered.

Outside the Emerging Markets, Japan's TOPIX 100 added 2.5% in local terms (+3.9% in USD), with the yen's partial recovery against the dollar amplifying returns for USD-based investors.

Equity asset class

We have shifted to a neutral stance on equities, as the repricing of inflation expectations, interest rates, and geopolitical risk premia is creating significant headwinds.

We continue to advocate diversification across regions, with a recent underweight to Europe given its significant exposure to the energy shock, particularly through natural gas dependence.

Markets still price a manageable shock; the most likely scenario remains a correction within an uptrend.

Earnings

Earnings remain supportive but are likely to be revised down with a lag, with growth potentially shifting to single digits, especially in energy-sensitive regions.

Valuation

US large caps are no longer as stretched as they were, but they remain expensive in absolute terms. The forward P/E has compressed from ~22x to ~18.5x, reflecting a partial normalization in valuations. The equally weighted S&P 500 appears more attractive at ~16x, highlighting less demanding valuations beyond the mega-cap segment.

Japan also trades at elevated levels (~21x forward P/E), while other regions offer more compelling, notably Europe (STOXX Europe 600 at ~14x) and Asia ex-Japan (MSCI Asia ex Japan Index at ~12x), where valuations remain comparatively more attractive.

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

Global equity markets performance between 26 June–3 July 2026 was marked by a partial unwind of an unprecedented Q2 chip rally, a softer US jobs report that eased near-term Fed tightening expectations, a European defence-and-industrials rally ahead of the NATO Ankara summit, and extreme volatility in South Korean chipmakers that dragged emerging markets sharply lower.

Global equity markets sold off sharply in the week to Friday 26 June 2026, as investors reassessed AI-related valuations against a backdrop of hawkish Federal Reserve signalling and sticky inflation. The MSCI ACWI fell 2.2%, with technology and semiconductors bearing the brunt of the decline — the Nasdaq 100 lost 4.2% and the iShares Semiconductor ETF shed 7.7%. The sell-off was sharpest in AI-exposed markets across North Asia, with the KOSPI and TAIEX both falling over 5%. Defensives and small-caps outperformed globally, with healthcare, insurance, and consumer staples all posting gains. Micron's record quarterly earnings provided a late-week counterpoint, but were insufficient to reverse the broader de-rating of growth assets.

A weekly review of global equity markets for the period ending 12 June 2026, covering the impact of renewed US-Iran tensions and the ECB's first rate hike since 2023 on regional equity performance, the rotation away from mega-cap technology into financials and cyclicals, and the significance of the SpaceX IPO as a landmark moment for the AI infrastructure investment cycle.

Live feeds, charts, breaking stories, all day long.

Our latest research, commentary and market outlooks