.png)

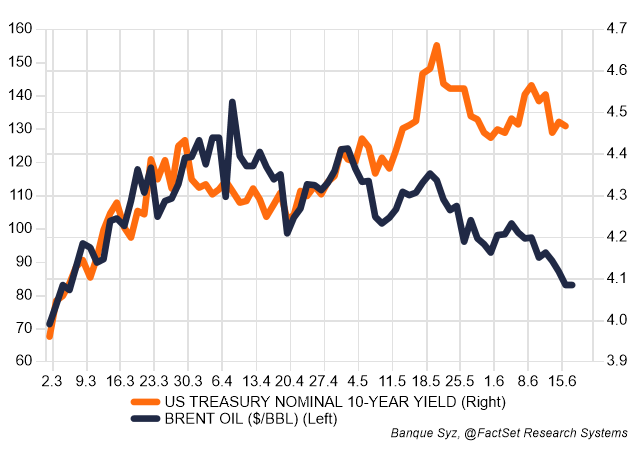

US Treasury Yields are no longer solely driven by oil prices as the US economy remains strong

Oil prices and US Treasury 10-year yield

The US-Iran war appears about to end after the announcement of an agreement on a memorandum of understanding that should be signed next Friday in Geneva. This would put an end to a conflict that started on February 28th.

In the initial phase of the conflict, the surge in oil prices and its expected impact on inflation drove global interest rates higher. Up until the beginning of May, US long-term yields were moving in tandem with oil prices.

But this close relationship then broke down when the US economy exhibited unexpected resilience to this energy price shock. Since May, most economic data in the US have been above expectations, as reflected by the spike in economic data surprises to their highest level since 2023.

Even as oil prices continue to decline and are back close to their pre-conflict levels, the US 10-year yield remains anchored around 4.5%, a level reflecting expectation of sustained solid nominal growth ahead. The US-Iran deal announcement has only triggered a moderate decline in US Treasury yields. The Fed’s meeting this week, with the update on economic projections and the first communication of Kevin Warsh as Fed Chair, will be key for the US long-term rate outlook in the second half of the year.