.png)

At the beginning of the year, copper prices printed fresh all-time highs on the London Metal Exchange (LME), hitting $13,407 a metric ton. Year-to-date, copper is already up around 3%, following a gain of roughly 40% in 2025.

Historically, copper has been a cyclical commodity, closely tied to the global growth cycle, particularly construction and manufacturing activity. In previous upcycles, price strength tended to fade once growth slowed or inventories rebuilt. This time, however, demand drivers appear broader and more durable. An increasing share of copper consumption is now linked to long-term electrification trends that are less sensitive to short-term economic fluctuations.

From a demand perspective, copper is a critical material for conducting electricity. It enables efficient power transmission, resists corrosion, has natural antimicrobial characteristics and retains its properties through repeated recycling. Substitution options are limited. Aluminium is often cited as an alternative, but it has only about 60% of copper’s conductivity, meaning cables must be thicker to carry the same electric current and often require additional insulation due to poorer heat dissipation.

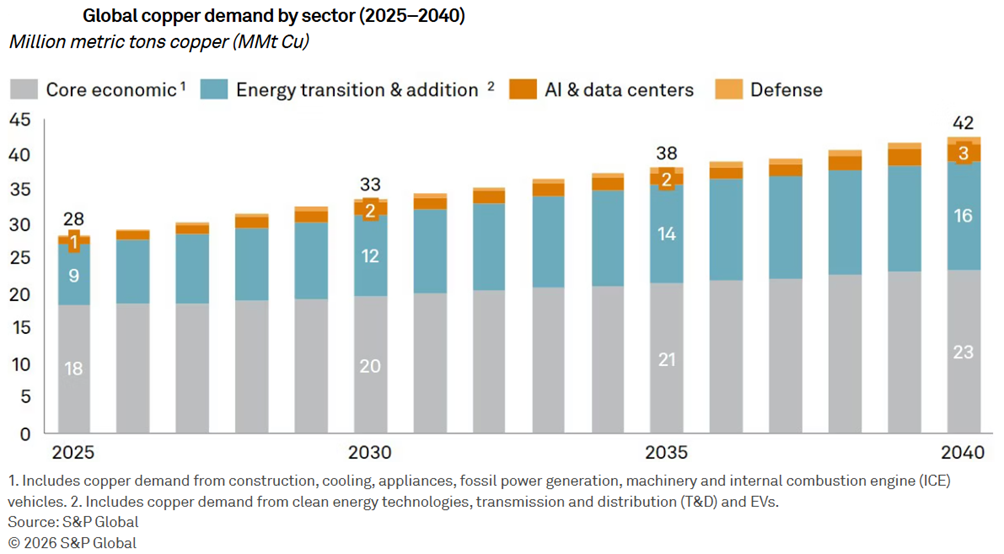

According to S&P Global, global copper demand is expected to increase by around 50% by 2040, rising from roughly 28 million metric tons today to about 42 million. This growth is driven by four main vectors: core economic demand, the energy transition and capacity additions, AI and data centres, and defence modernisation. Core economic demand and energy transition–related uses are expected to remain the largest contributors, and Asia is likely to account for 60% of the incremental demand.

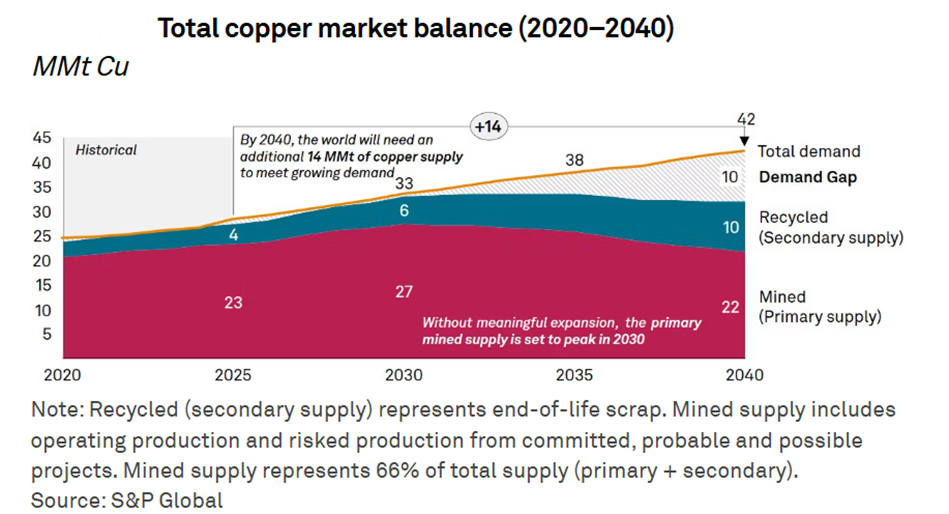

Global demand is increasing, but supply is projected to remain constrained due to the ageing of current mining assets. In the absence of significant capacity growth, this could lead to a deficit of around 10 million metric tons by 2040.

Closing this gap is a massive challenge for the coming decades. The supply response is complex and structurally constrained. Substitutes are not a viable solution, due to copper’s exceptional conductivity, durability, and recyclability.

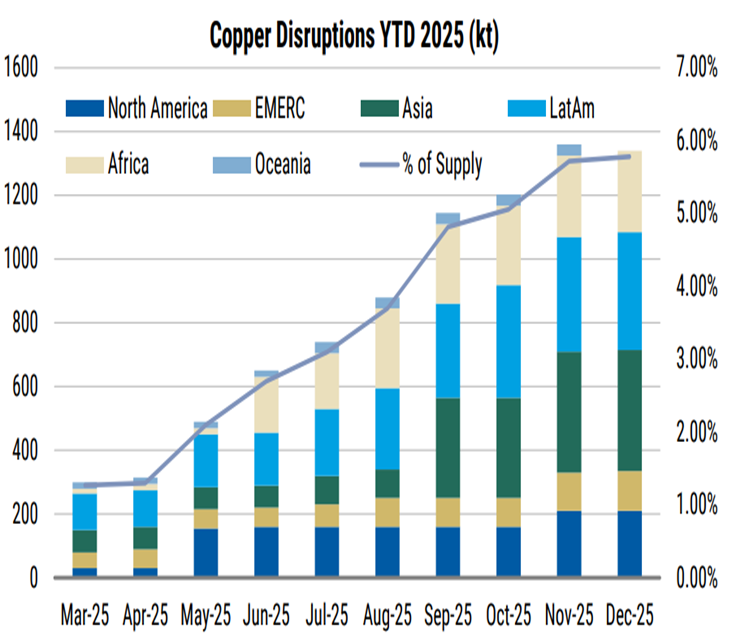

Over time, the depletion of copper mines has made extraction increasingly complex and costly, while mining companies face growing regulatory pressures and environmental opposition from local communities. These fragilities have translated into repeated disruptions in recent years. Freeport-McMoRan declared force majeure at its Grasberg Mine, the world’s second-largest copper mine which represents around 4% of global output, with a full recovery not expected until 2027. Supply disruptions are set to persist this month following strikes at Capstone Copper’s Mantoverde Mine in Chile.

Source: Morgan Stanley

Developing new copper assets takes nearly two decades, approximately 17 years, from discovery to first production- due to regulatory, environmental, political, and cost-related challenges. Current prices, however, provide insufficient incentive to bring major new deposits into production by 2040. Most of the easily accessible copper deposits have already been mined or are currently being mined. This emphasises the need to maximise production from existing assets, improve operational efficiency, and streamline permitting and incentive frameworks for new projects. Future supply will depend on deeper exploration and will be more costly and technically complex.

Several deposits have been discovered that could, in theory, help meet future demand. However, many of these proposed projects may never exist, as they are not feasible at current prices or with current technologies.

Secondary supply relies on recycling, which provides an additional source of production but cannot fully close the gap. Unlike other metals, copper retains its essential properties when recycled, making it virtually identical to newly mined material. As copper use expands across industries, more waste will become available for recovery as assets reach the end of their useful life. Total end-of-life copper waste is expected to grow by about 4% per year, reaching over 15 million metric tons by 2040. According to S&P Global, if recycling rates rise from 50% in 2025 to 66% in 2040, recycled copper from end-of-life materials could contribute roughly 6 million metric tons to the total supply.

The development of copper recycling depends on the establishment of more efficient collection and processing infrastructure. Compared to mined copper, scrap supply is relatively flexible, but policies will play a crucial role in expanding recycling worldwide. Several regions, including the United States, the European Union, and China, have already introduced policies setting recycling targets or supporting infrastructure development. These measures aim to increase the supply of secondary copper while reducing environmental impacts. Even with significant improvements in processing methods, recycling could contribute at least one-third of total copper supply by 2040.

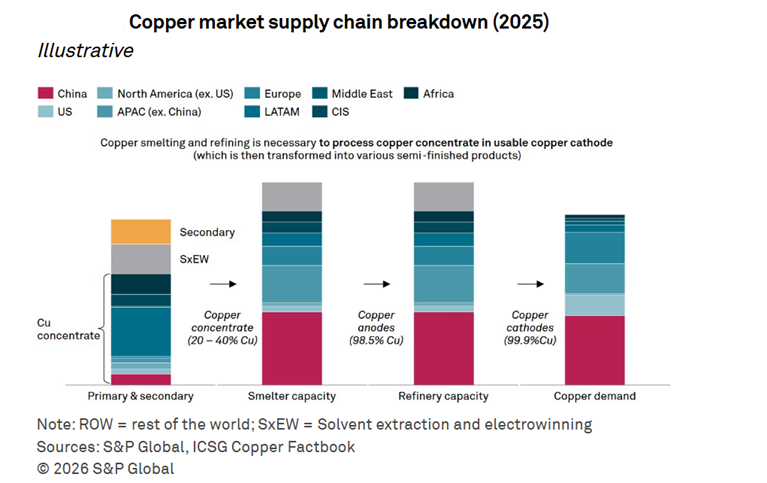

The conversion of raw materials through smelting and refining is concentrated primarily in China, making it a strategic point in the global supply chain. China controls a substantial share of global smelting capacity roughly 12 of the 29 million metric tons worldwide and continues to expand its footprint, further increasing industry concentration. Processing margins are becoming increasingly fragile due to declining treatment and refining fees, as well as regionally varying costs and regulations. At the same time, the high concentration of capacity, estimated at 40 to 50% of the global total, heightens systemic vulnerability and the risk of geopolitical disruptions.

For all these reasons, governments recognise the strategic importance of mineral supply chains. New forms of international cooperation and the growing involvement of sovereign wealth funds are creating alternative strategies for strengthening and diversifying access to critical mineral resources and supply chains away from China.