.png)

A bad start for debt

Emerging market (EM) sovereign and corporate bonds (hard currency) are off to the worst start in their history, with a performance of close to -4%. This added pressure to the already poor performance of 2021: since January 1, 2021, emerging market sovereign bonds have lost about 7%.

First two weeks of performance each year

Source: Bloomberg

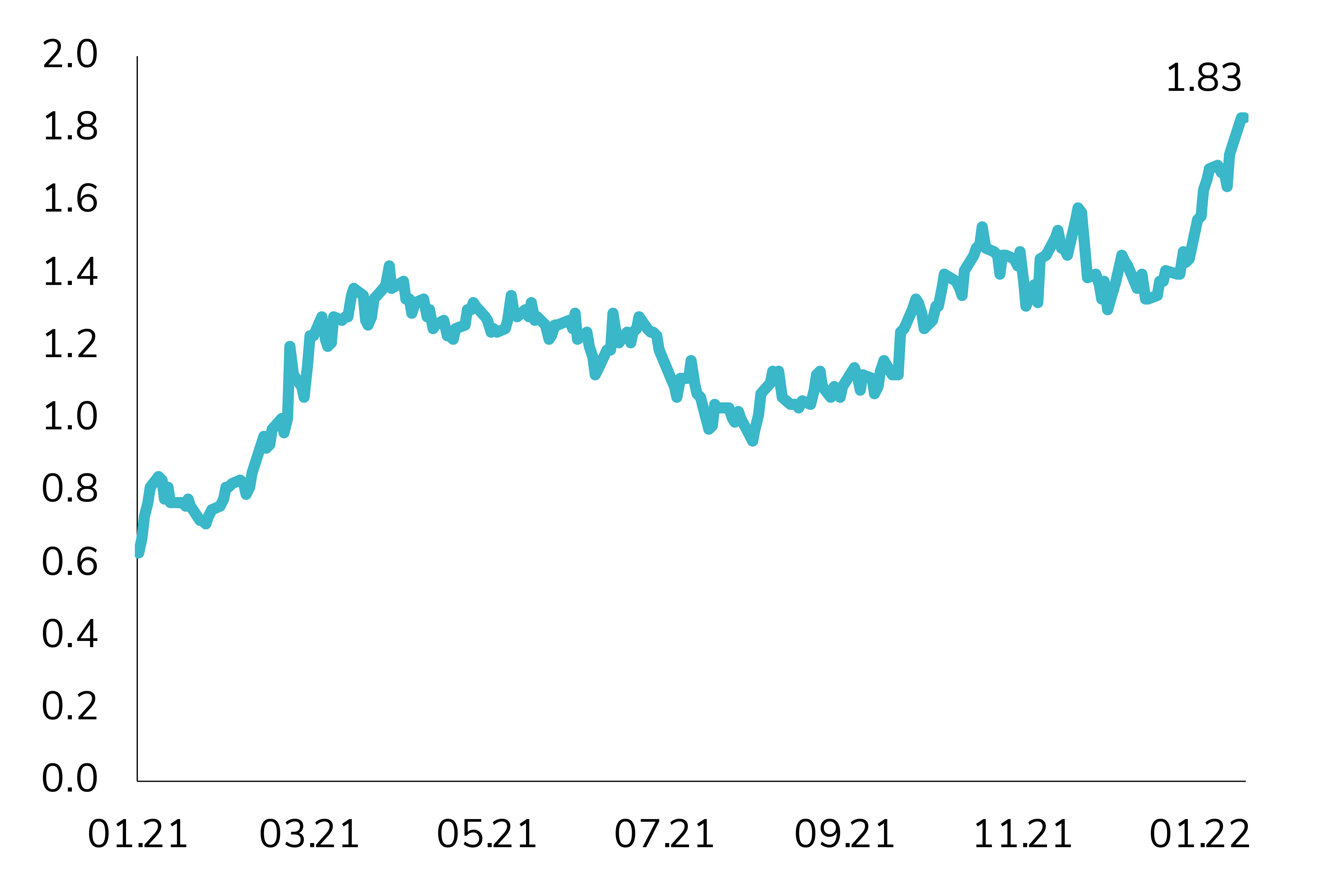

This performance is in part due to rising US interest rates. In fact, the US intermediate yield curve (7-10 years) has lost more than 3% since the beginning of the year.

Since the beginning of 2021, the US Treasury 7-year rose more than by 120 bps

Source: Bloomberg

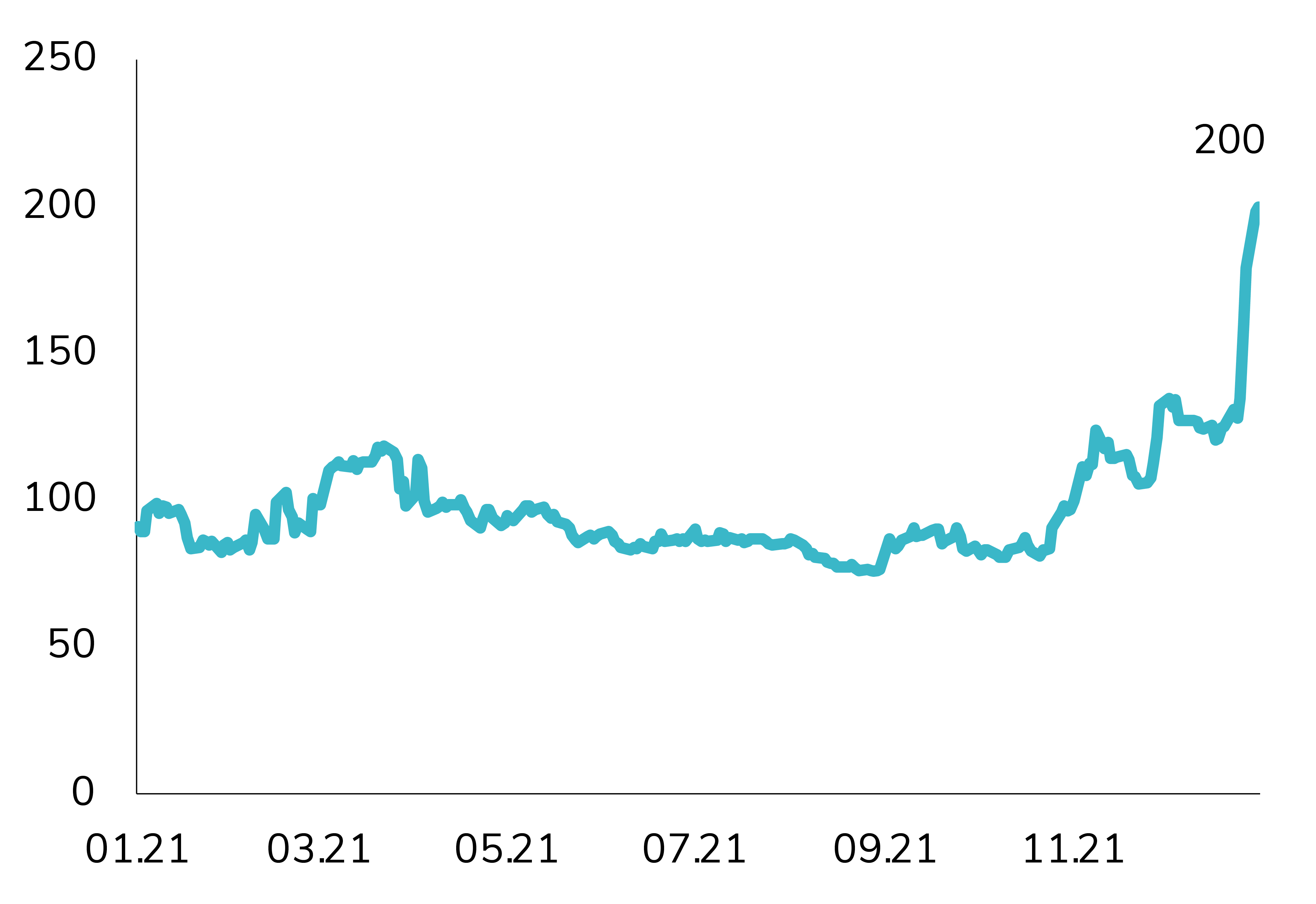

Furthermore, some idiosyncratic risks are also weighing on performance. Tensions between Russia and Ukraine have hit their bonds, with an average performance of -7.5% since the beginning of the year.

Russia CDS 5-Year (in BPS)

Source: Bloomberg

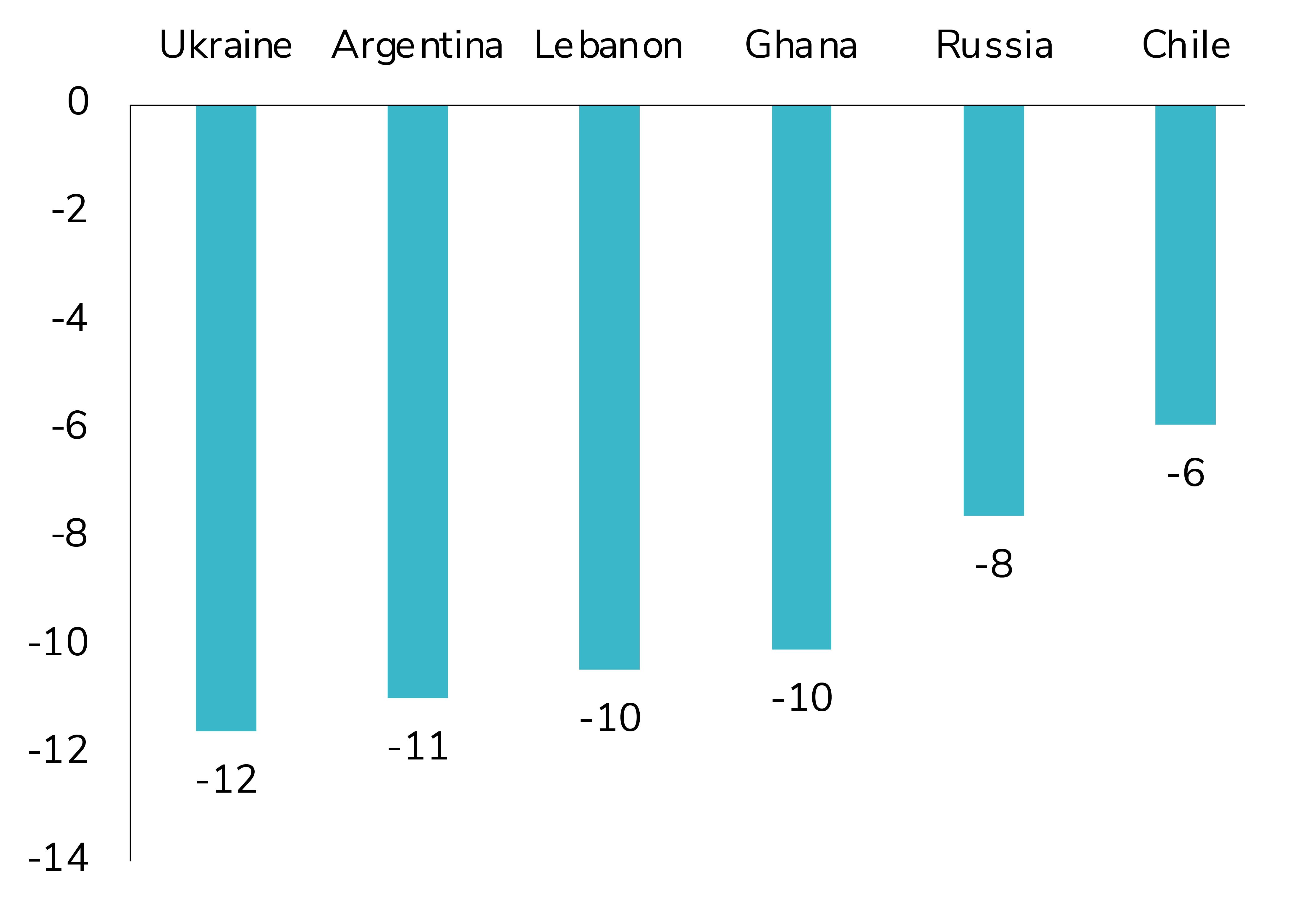

In Argentina, bonds, which are among the worst performers since the beginning of the year, lost nearly 10% due to difficulties in reaching an agreement with the IMF on debt restructuring. In Mexico, bonds were hit by a loss of more than 3% from a new supply (an amount of $6 billion) that gave an attractive premium.

Largest underperformers of 2022 so far - Total Return (%)

Source: Bloomberg

The house’s take on things

In general, we are less negative on EM debt, which is justified by rising commodity prices, more attractive valuations and the fact that the monetary policy tightening cycle is already well underway in Emerging Markets. We also prefer corporate bonds to sovereign bonds, as the latter are more sensitive to rising US interest rates (and a stronger US dollar).

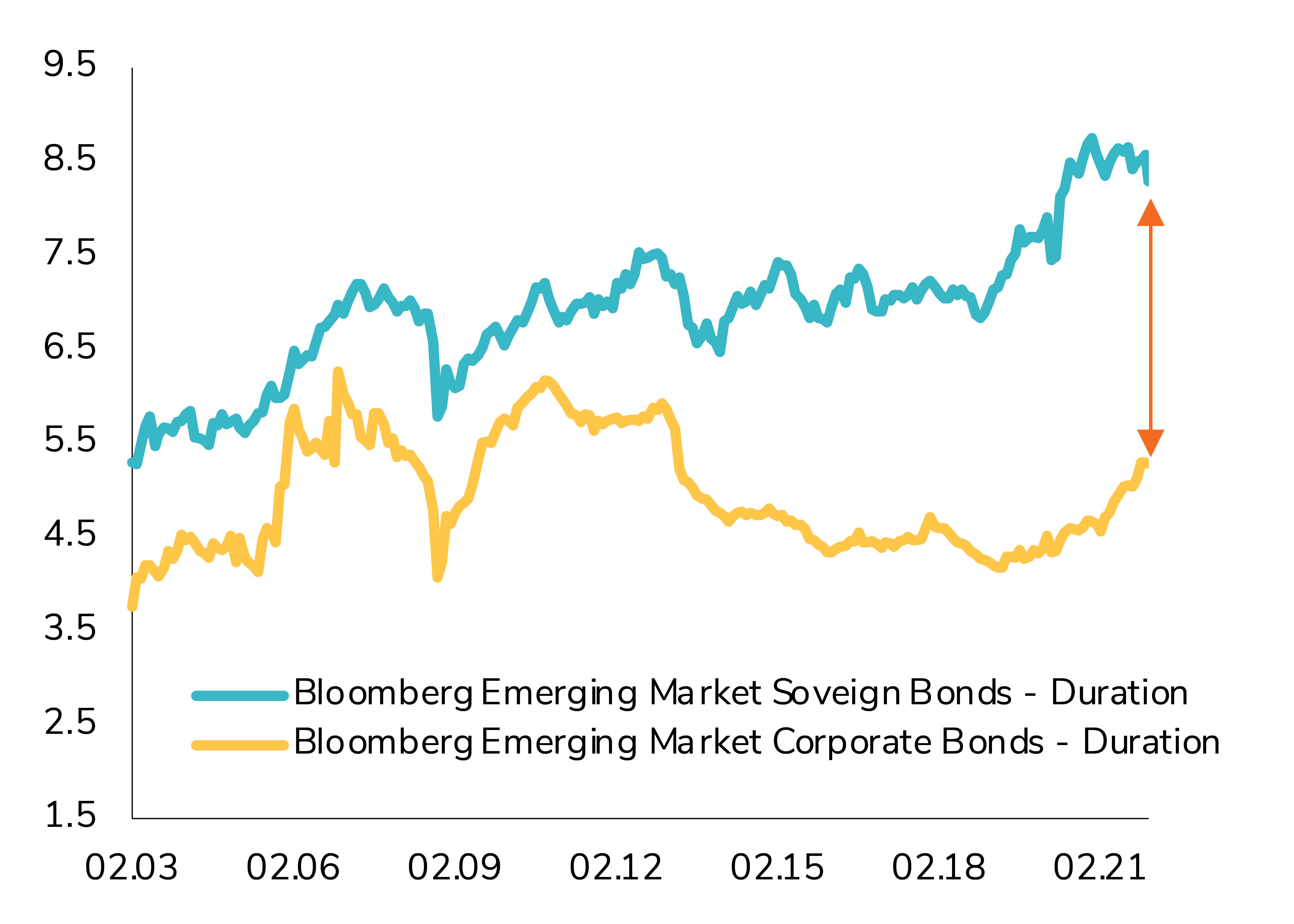

The sensitivity (duration) to a rise in U.S. interest rates is almost at its widest between the emerging market sovereign and corporate bond indices.

Source: Bloomberg

On a negative note, geopolitical tensions are rising (e.g. Russia/Ukraine), which will continue to affect the performance of emerging market sovereign bonds. The Brazilian elections will also continue to put pressure on Brazilian bonds until the end of the year.

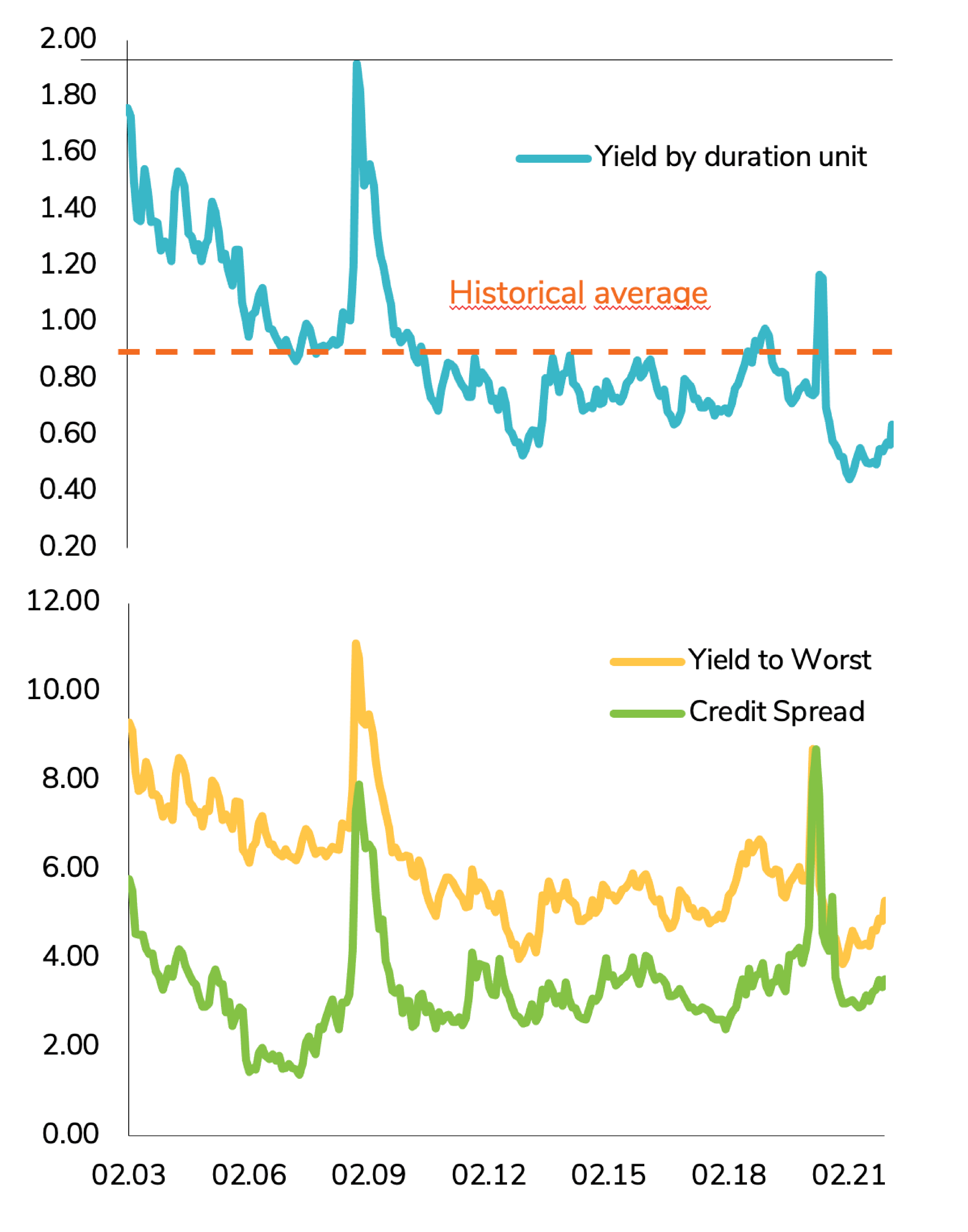

In addition, the average yield to maturity of the USD emerging market sovereign bond index is still below its historical average (5.2% vs. 6%). See the following graphs:

Yield by duration unit

Source: Bloomberg

Conclusion

Overall, the entry point is much better than a year ago, but emerging market sovereign bonds could suffer again in the short term. We therefore recommend waiting for more stability before investing in cash bonds. We would also favor to invest now only via option strategies.