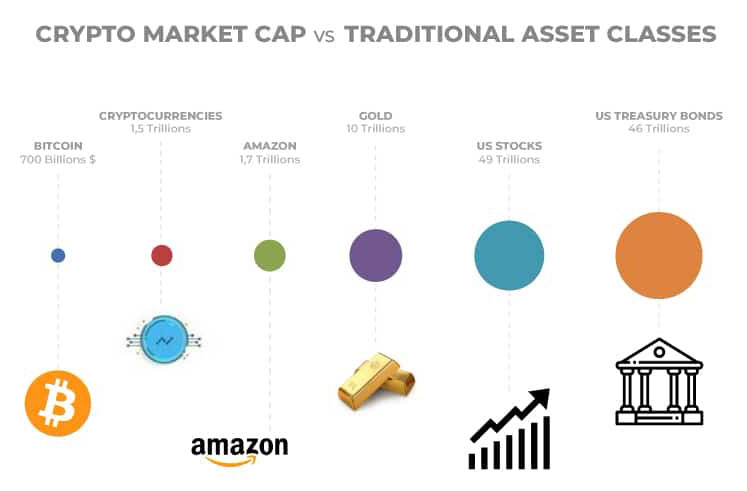

.png)

The vast majority of investors are looking for what are known as "secular bull markets", i.e. assets backed by factors that remain buoyant for years.

But most of these investments are over-represented in portfolios, with the result that valuation ratios are far too generous. As with all overvalued crowded trades, the risk of a sharp fall in the event of bad news is relatively high.

In the recent past, the GAFAs (Google, Apple, Amazon, etc.) and European luxury goods stocks (LVMH) have suffered relatively intense selling without their long-term fundamentals being called into question.

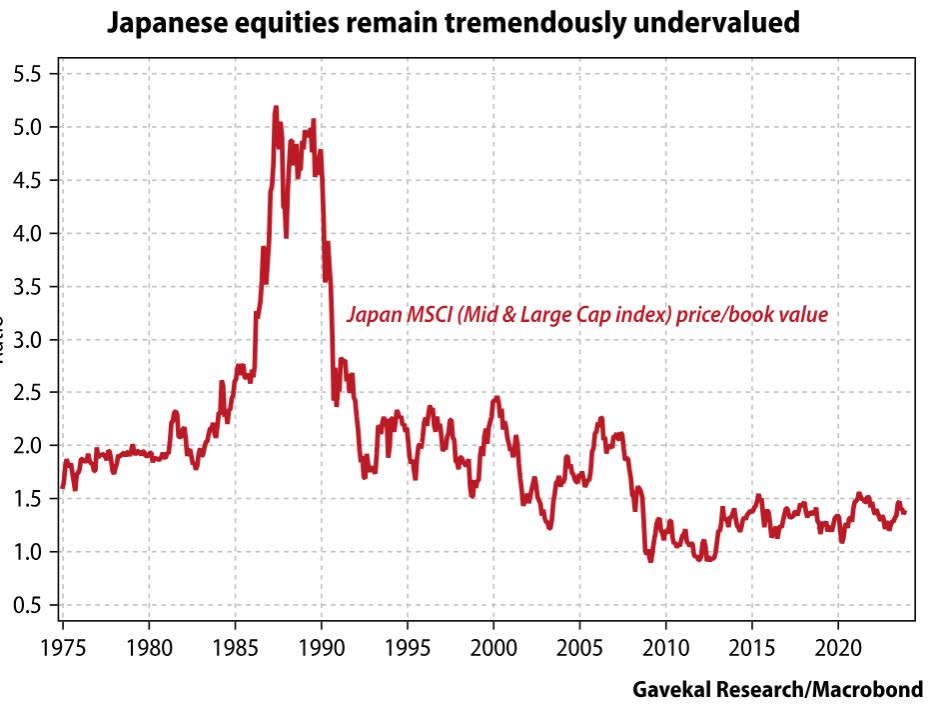

Is it now possible to identify markets that appear to be on a long-term uptrend, but with attractive valuations that are still under-represented in portfolios? Here are 5 examples of assets that seem to combine these characteristics.

Source: The Hub

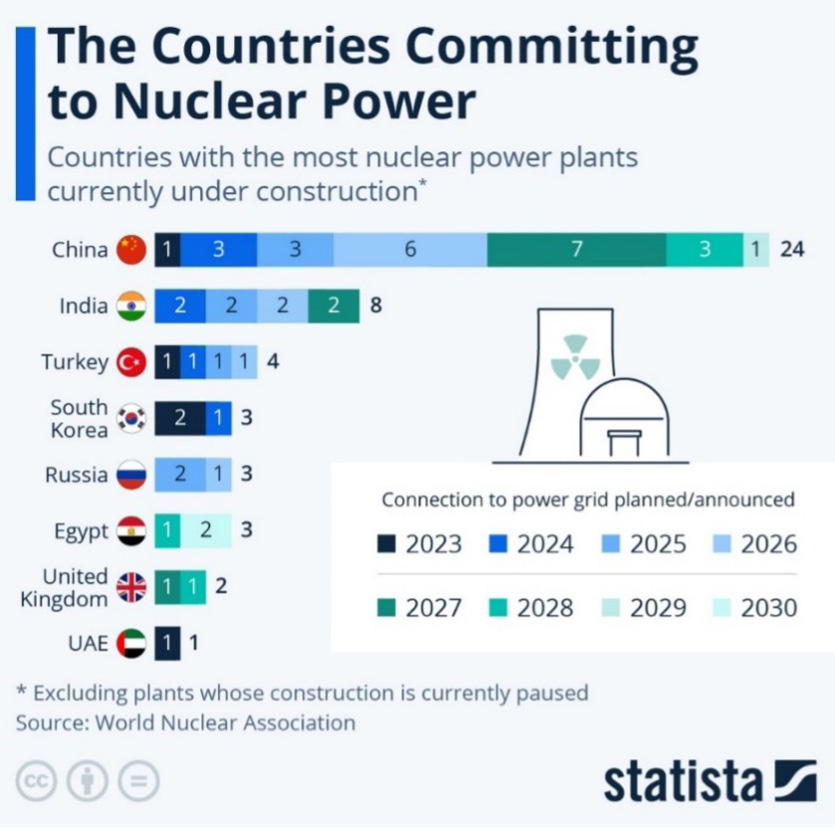

Unlike most raw materials, demand for uranium is not very price-sensitive, since price represents only a small part of the total cost of operating a nuclear power plant. Nor is it subject to substitution effects.

In addition, apart from Canada and Australia, most of the uranium produced in the world comes from destinations with a high geopolitical risk: Russia, Kazakhstan (where Russia's ability to tip the balance is colossal) and the Sahel, a vast region of Africa where the French Foreign Legion is increas-ingly being replaced by the Russian mercenaries of the Wagner group.

Despite all these positive factors and the sharp rise in uranium prices (see chart below), this theme is not very present in international portfolios. Admittedly, uranium is a niche market and there are few ways for investors to participate in a wider revival of nuclear energy. This is especially true as it seems likely that many of the nuclear power plants planned around the world will ultimately be built by Chinese or Indian companies. Investors can gain exposure to physical uranium through the Sprott Uranium Trust, which trades on the Toronto Stock Exchange. On the other hand, the companies that mine the commodity (Uranium mining companies) have a leverage effect on the price of the underlying. The Global X-Uranium ETF (URA) and the North Shore Global Uranium ETF (URNM) are exposed to this.