.png)

There is, once again, a paradox at the heart of markets, but this month it is the mirror image of May. A month ago, the puzzle was how equities refused to fall while the Strait of Hormuz was shut down. In June, the puzzle is the reverse: the very thing markets feared has gone away, and the relief has set off a violent reshuffling under the surface. The Strait is reopening, crude has collapsed back toward pre-war levels, headline inflation has likely peaked, and the consumer is about to receive a tax cut in the form of cheaper gasoline. By any conventional playbook, this is unambiguously good news. And yet the market’s former generals, such as the Magnificent 7, the AI complex, and even gold, are the ones now under pressure, while the dollar that almost everyone was short has ripped higher.

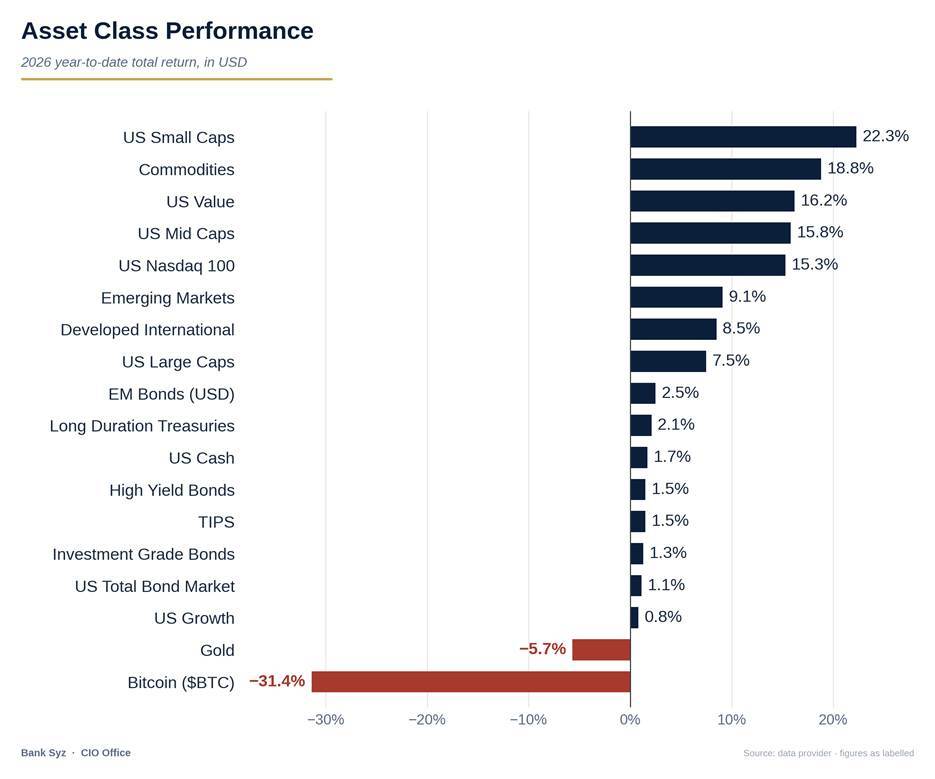

The single most arresting statistic of the year captures it: the two worst-performing major assets in 2026 are Bitcoin (−31%) and gold (−6%) –a combination we have never seen in any calendar year. The answer, in one phrase: the macro shock is reversing, and the reversal is rotating the market rather than lifting it. The oil spike everyone feared is unwinding –and as it unwinds, it is pulling the rug from under the very trade that carried markets through the spring.

The shock everyone feared is fading

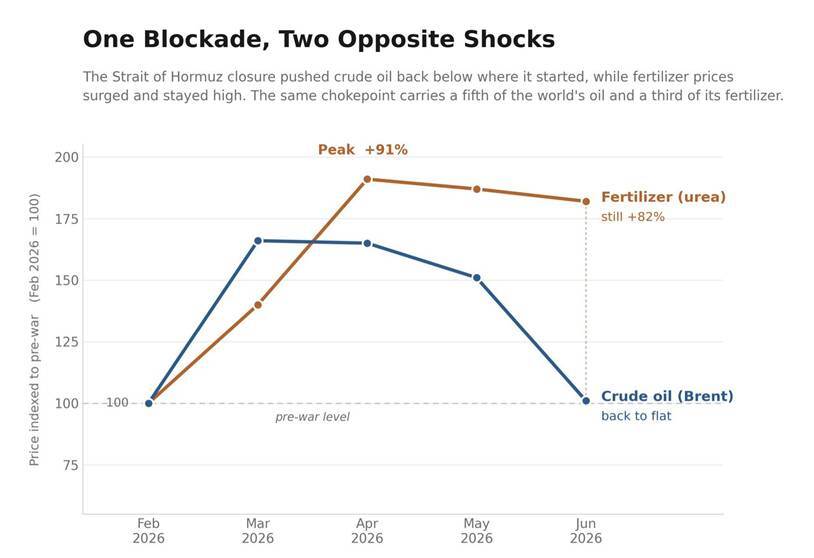

After the April ceasefire was extended and an interim deal to reopen the Strait of Hormuz was struck, the energy emergency has gone into reverse. There were renewed US–Iran strikes over the weekend and commercial traffic through the Strait remains well below pre-crisis levels, but Washington and Tehran have again agreed to pause hostilities and resume technical talks. Our base case is a swift recovery of shipping through Hormuz and a relatively quick re-adjustment of the global trade system. The market has already moved: WTI crude has tumbled to its 200-day moving average (see chart below), finding support just above its pre-war level and trading at its lowest in almost four months. Cracks in OPEC discipline (Iraq reportedly weighing its options on quotas) only reinforce the move.

The one counter-shock to watch is fertiliser: roughly a third of traded fertiliser transits Hormuz and prices are up nearly 80% since February, with no strategic reserves to cushion the blow.

Relief is disinflationary –and a tax cut for the consumer

Energy was the engine of this year’s inflation scare: it added a full 1.5 percentage points to May headline CPI, which hit 4.2% in the US. The drop in oil should reverse a good part of that, with the energy contribution easing toward roughly 1 percentage point in July and falling further through the summer — meaning the peak of the 2026 inflation spike is most likely now behind us. The relief lands directly on households: US gas prices are already down to almost $3.90 a gallon. That matters because households have absorbed the shock by running their savings rate down to just 3% while keeping spending up around 2.1% annualised. Cheaper energy gives them the firepower to spend and rebuild savings at the same time. There is a monetary twist, too: with May’s inflation print, the real Fed funds rate has turned negative (−0.4%) — policy is now passively easing even before any cut, simply because inflation rose faster than the nominal rate.

But the relief detonated a rotation, not a melt-up

Here’s the sting. The same lower-oil, broadening-growth story that helps the consumer is precisely what undermines the market’s crowded leadership. June brought a pronounced rotation: large-cap value beat growth by 368 basis points, the equal-weighted S&P 500 outpaced its cap-weighted twin, and the Russell 2000 and Dow advanced while the Nasdaq and S&P sagged under tech weakness.

The 10-year Treasury yield slid below 4.40% for the first time in over a month. Crucially, the Magnificent 7 are beginning to crack, and for the first time the AI capital-expenditure boom is feeding through into consumer prices: Apple has raised MacBook prices and Microsoft has lifted Xbox prices, both citing surging memory costs. Hyperscaler forward P/Es have fallen to a discount versus the S&P 500 – their lowest since ChatGPT launched – though this reflects expanding free-cash-flow multiples rather than collapsing fundamentals. Tellingly, the buyback support that once underpinned the rally has also given way to net equity issuance.

The strangest tell: havens sold off, the dollar roared back

The clearest sign that this is a positioning unwind rather than a fundamental break is what happened to the consensus trades. Gold suffered a “death cross” — its 50-day moving average crossing below its 200-day for the first time since September 2023 — and briefly broke below $4,000, its lowest since November 2025. Bitcoin slid back below $60,000 and through its 200-week moving average. Meanwhile the dollar – the year’s most hated asset – strengthened, with the DXY rising 2.5% in June as it decoupled from oil and began trading once again on macro data and rate expectations. The market was short the dollar and long the havens; the squeeze moved violently the other way.

Rotation, not rupture

Three things keep us constructive on the trend even as we respect the near-term turbulence. The long-term technical backdrop remains intact: the S&P 500, STOXX Europe 600, Nikkei 225 and MSCI Asia ex-Japan all sit in established uptrends.

Participation is broad. Advance-decline lines are at or near record highs and more than 60% of industries remain above rising 200-day averages. Sentiment is far from euphoric, which historically reduces the risk that a correction marks the end of a bull market. Short-term breadth had thinned beneath the surface, signalling a stretched market due a consolidation, which is exactly what a healthy mid-cycle rotation looks like, not a top.

|

The hinge: watch the AI capex narrative The decisive variable is no longer the oil price; it is confidence in the AI investment cycle. For the first time, AI capex is bleeding into consumer prices, and investors are beginning to ask a different question: how long will markets keep rewarding record AI spending before demanding stronger returns? If Wall Street starts to expect less investment rather than more, the market would not merely reprice Big Tech; it would begin pricing in capex cuts – lowering hyperscaler growth, hitting semiconductor demand, and potentially triggering a broader selloff. The new Fed under Chair Warsh is the second hinge: with the real funds rate now negative, his hawkish debut is a credibility test the market is only half-buying. |

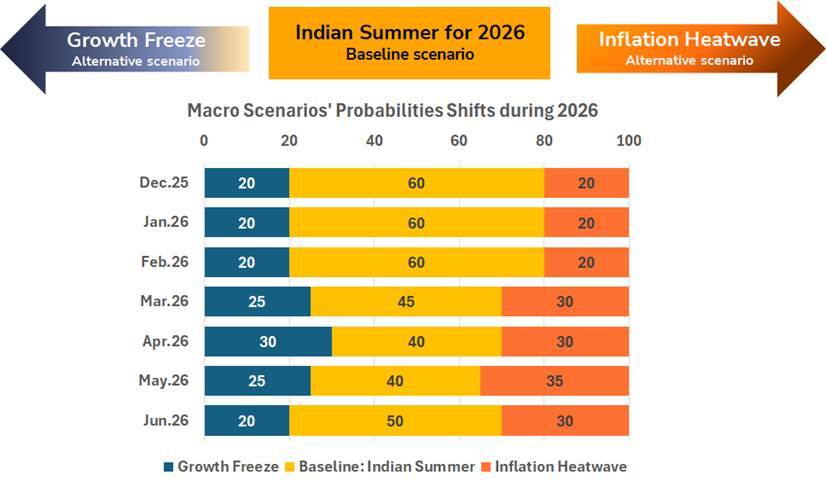

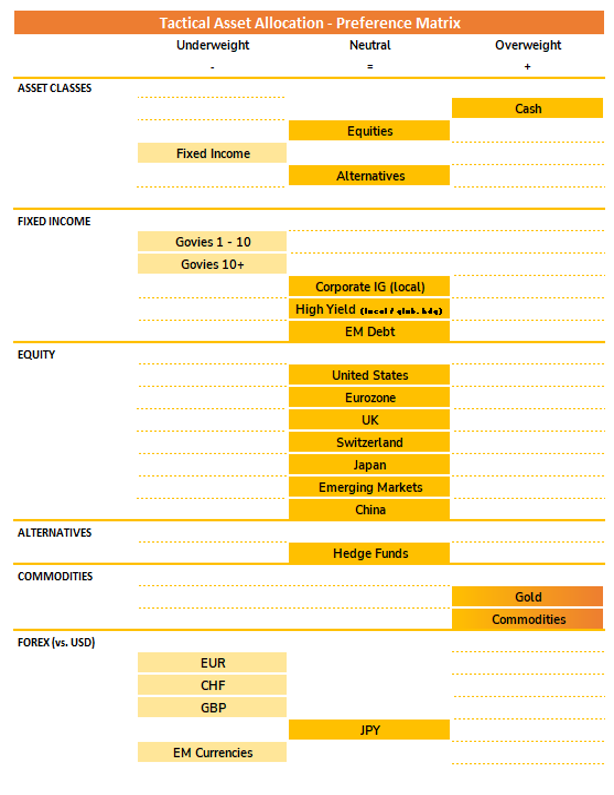

How does the picture translate into asset allocation preferences and portfolio positioning? Below we review the weight of the evidence and the subsequent investment decisions. The starting point is our three-scenario framework, where the de-escalation in the Middle East has shifted the balance of probabilities meaningfully toward the constructive outcome.

- Indian summer for 2026 (baseline — probability 50%): global growth is expected to do well in H2 2026 as the energy price shock and the ruptures in the trade system fade, while fiscal spending supports demand. The US remains stronger than most other regions as fiscal stimulus and AI-driven investments stay higher. The Eurozone returns to a moderate growth path after digesting the H1 energy shock. China and emerging markets benefit from lower trade uncertainty and a stronger global capex cycle. Global inflation should abate later in the second half of the year, thanks to the price decline in energy and related products and services and a moderation in demand. However, most larger countries and regions, i.e. the US, Eurozone, UK, Japan will likely run above central banks targets of 2%, only China and Switzerland will see a within target inflation.

- Inflation heatwave (probability 30%): We see several potential risks that could trigger such a scenario with fiscal stimulus and AI capex push growth into a boom that overheats inflation, the Fed turns too dovish and falls behind the curve, or a renewed trade or geopolitical energy shock reignites prices.

- Growth freeze (probability 20%): We see several potential risks that could trigger such a scenario with lower- and middle-income consumers retrench, the AI capex cycle disappoints on returns, credit strains emerge, or fiscal debt begins to backfire.

Our asset allocation preferences rest on five indicators: four macro and fundamental (leading) and one of market dynamics (coincident). The weight of the evidence keeps us constructive on equities overall, with two changes this month: an upgrade to the macro pillar and an offsetting downgrade to liquidity. Below we review the main drivers of each.

- Macro cycle (MODERATELY POSITIVE — upgraded from neutral): the global economy is proving more resilient than expected, particularly in the US, and the outlook has brightened. The fall in oil back toward pre-escalation levels should ease inflation pressure over coming quarters and support consumption, justifying the upgrade.

- Liquidity (NEUTRAL — downgraded from moderately positive): the prospect of Fed rate hikes and slowing Treasury purchases, combined with the drag of a stronger dollar on global liquidity, now offsets the still-positive short-term dynamics in our Global M2 proxy and accommodative financial conditions.

- Earnings growth (POSITIVE — unchanged): the fundamental backdrop remains strong. Q1 EPS growth materially exceeded historical norms with broad participation across sectors and market caps, guidance stayed constructive, and operating margins reached record highs across the US, Europe, Japan and Asia ex-Japan.

- Valuations (NEUTRAL — unchanged): US large-caps trade above their 10-year averages while international equities sit at a discount; the equity risk premium remains low in both the US and Europe.

- Market Factors (POSITIVE — unchanged): our Symphony indicators keep the model at 100% allocation to equities (75% US / 25% Europe). The US raw score remains elevated at 83 and the volume indicator turned positive; the European score oscillated through the month to close around 60, held back by weaker technicals and sentiment.

A momentum break, not a thesis break

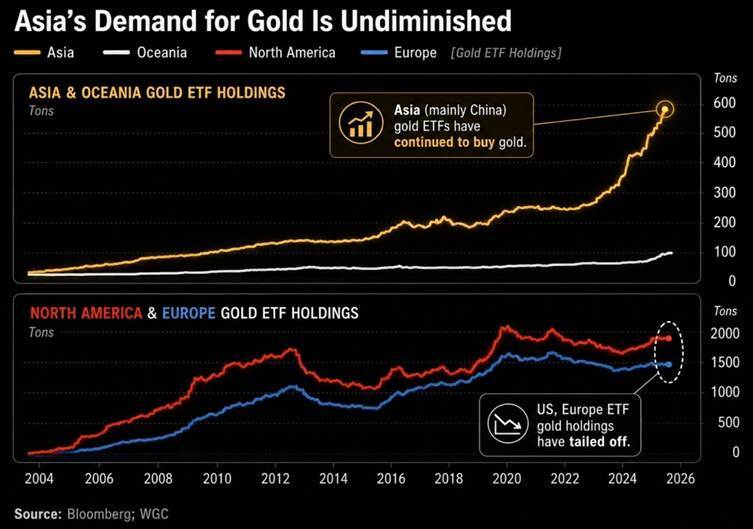

Gold’s month deserves its own examination because, at first glance, it appears to mark the repudiation of an entire thesis. The metal broke below its 200-day moving average and the $4,000 level, suffered its first death cross in nearly two years, and now ranks among the worst-performing major assets of 2026. Yet the contradiction is that none of the structural arguments for gold have actually changed — so what gave way?

What changed is positioning and the macro cross-currents, not the fundamentals. As the oil-inflation hedge unwound, the dollar firmed and real yields backed up; the West sold -- ETF outflows, tactical and momentum money heading for the exits. But the East bought the crash. Eastern ETF flows tell a starkly different story from Western ones, and the underlying central-bank and Asian retail accumulation has continued through the weakness. That is the asymmetry that matters: Western selling is price-sensitive and reversible, while Eastern buying is structural and largely price-insensitive, driven by reserve diversification and de-dollarisation.

Our long-term view is therefore unchanged and constructive. Gold remains, in our framing, a structural verdict on the dollar –underwritten by the US fiscal trajectory, persistent twin deficits and ongoing political pressure on the institutional set-up behind the currency. A death cross is a backward-looking momentum signal, not a break in that thesis. We use the pullback to retain, not reduce, our overweight.