.png)

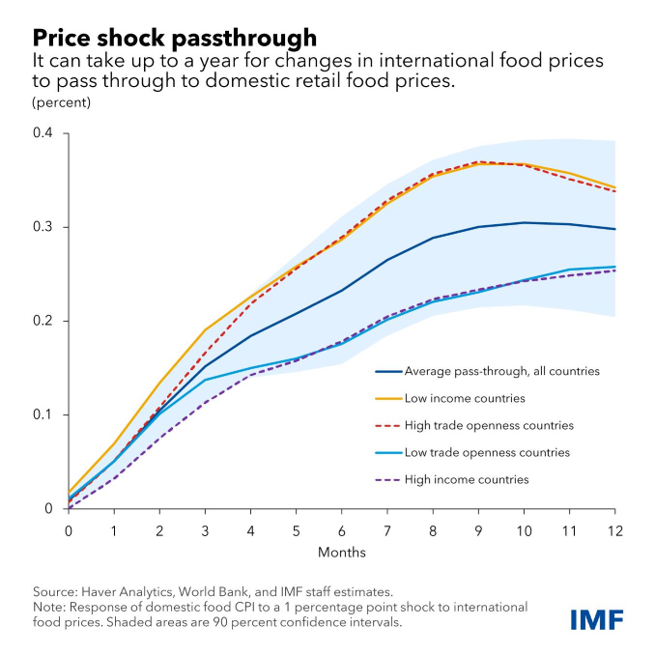

The macroeconomic impact of El Niño has been studied and measured. The main channel runs through commodities, especially food. Central-bank and academic research broadly points in the same direction. ENSO cycles have historically influenced commodity-price inflation.

Federal Reserve research suggests that close to 20% of commodity-price inflation movements can be linked to the ENSO cycle. A typical El Niño can lift real commodity-price inflation by roughly 3% over a six-to-twelve-month period, with food commodities carrying most of the impact. Cashin, Mohaddes and Raissi extend the evidence, estimating an increase of about 5% in global non-energy commodity prices, lasting between six and sixteen months.

Weather disruption can reduce harvests, lower crop quality, delay logistics and tighten physical supply. Prices react first in agricultural markets. Once higher input costs move through food supply chains and consumer prices, inflation data follows. Higher food inflation can also weaken currencies, raise imported inflation and limit the room for central banks to cut rates.

Source: IMF

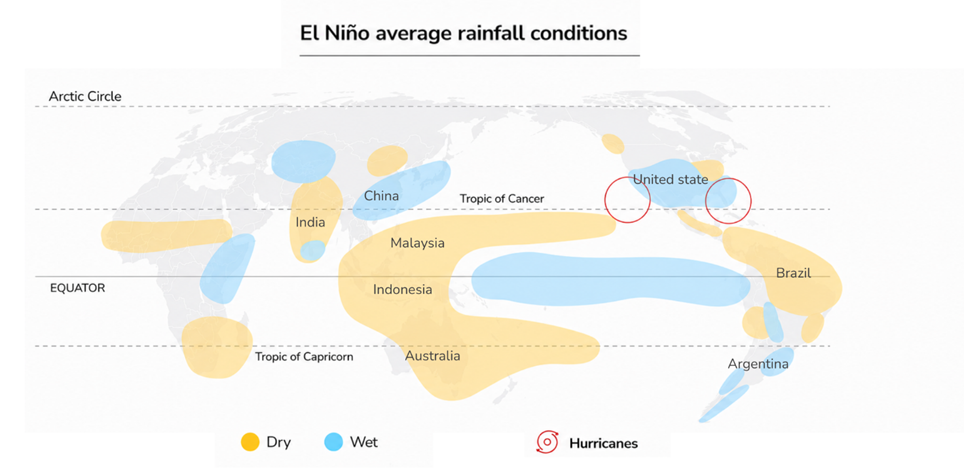

Two patterns are important. First, the growth impact varies sharply by country. Australia, India, Indonesia, Chile, parts of southern Africa and the Andes tend to face output losses when El Niño disrupts rainfall and agricultural production. The US and parts of Europe can see a milder or even slightly positive impact. In South America, the soy complex in Brazil and Argentina can benefit from wetter conditions.

Second, the inflation impact is asymmetric. The pressure is strongest in economies where food carries a large weight in CPI and currency pass-through is high. In these cases, higher food and energy prices can lift inflation expectations, weaken local currencies and amplify imported inflation. That leaves central banks with less room to cut rates, especially in commodity-importing emerging markets.

The euro area is less exposed. Banco de España finds that El Niño has historically reduced euro-area inflation by around 0.3 percentage points after twelve months, largely because of composition effects and the Common Agricultural Policy, which dampens the pass-through from global food prices to consumers.

Source: S&P Global

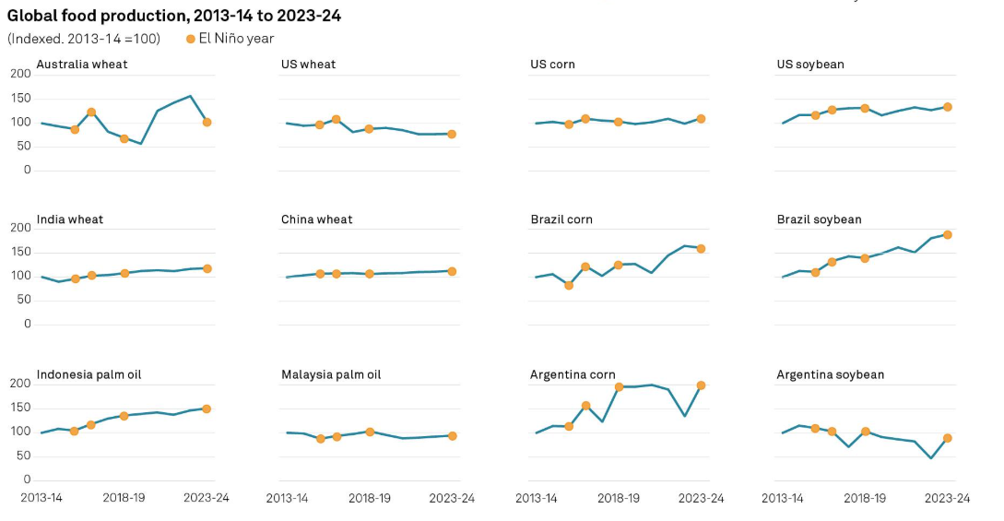

Commodity markets usually react before inflation data does. Crops trade on expectations, and expectations can change quickly when rainfall, heat and harvest quality come under pressure. This year, the weather risk arrives on top of an already tense input-cost backdrop. Farmers are still dealing with higher fertiliser and diesel costs after months of energy-market stress and geopolitical disruption. The World Bank expects headline commodity prices to rise by around 16% in 2026, the first annual increase since 2022, mainly because of energy and fertiliser. Agricultural prices are expected to fall in the baseline, which makes El Niño the upside risk to that view.

Past El Niño episodes have often been supportive for soft commodities. Cocoa, coffee, sugar, palm oil, cotton and rice all depend heavily on rainfall patterns in tropical regions. Yet, inventories, regional weather conditions and substitution effects can change the price response from one crop to another.

Cocoa looks particularly exposed. Ivory Coast and Ghana, the two largest producers, account for roughly half of global cocoa supply. Strong El Niño episodes have historically weighed on cocoa output, sometimes through drought, sometimes through excess rainfall and disease. The last episode showed how damaging that mix can be. Heavy rainfall first increased disease pressure on cocoa trees. Then intense heat and dry Harmattan winds hit already weakened crops. Prices nearly tripled in 2024 and rose above USD 12,000 per metric ton, turning cocoa into one of the most extreme commodity stories of the year.

Palm oil and cotton also offer direct exposure to Asian weather risk. Both are linked to conditions in Indonesia, Malaysia and India. A weak monsoon would quickly change supply expectations.

Coffee is exposed mainly through robusta. Vietnam and Indonesia produce around half of global robusta output, and El Niño usually brings hotter, drier weather during crop development. Arabica is more nuanced. Brazil can benefit from lower frost risk at first, but heat and dryness later in the year can still threaten the next crop.

Sugar is more cushioned. A weaker monsoon in India and Thailand can push prices higher but India could redirect 3–4 million tonnes from ethanol back to sugar, offsetting most of a moderate production loss.

Rice has the most direct link to the monsoon. A weak rainy season in Asia can quickly reduce production expectations and push food-security concerns higher, especially in countries where rice is a staple crop.

Corn depends more on regional weather than on El Niño alone. Dryness in some producing areas can support prices, but the signal is less consistent because other regions may see better growing conditions.

Regarding soybeans, El Niño can create stress in some regions, but Brazil and Argentina may benefit from additional rainfall. That makes the soybean trade less straightforward than rice or palm oil.

Natural gas is the exception. A milder Northern Hemisphere winter usually reduces heating demand and weighs on prices. In 2026, however, that bearish signal has to be balanced against energy-market stress linked to the Strait of Hormuz.

The next catalyst is the Indian monsoon. Rainfall between June and September will shape the outlook for cotton, sugar, rice and palm oil. A normal season would keep part of the El Niño risk contained. A severe shortfall would bring the real upside risk back into focus.

There is also a timing gap between futures and physical markets. Forecasts are still affected by the spring predictability barrier, the period when El Niño models are less reliable before summer signals become clearer. Futures can start pricing 2026–27 weather risks several months ahead, while physical markets remain tied to current inventories, crop conditions and near-term supply-demand balances.

Commodity markets usually react before inflation data does. Crops trade on expectations, and expectations can change quickly when rainfall, heat and harvest quality come under pressure. This year, the weather risk arrives on top of an already tense input-cost backdrop. Farmers are still dealing with higher fertiliser and diesel costs after months of energy-market stress and geopolitical disruption. The World Bank expects headline commodity prices to rise by around 16% in 2026, the first annual increase since 2022, mainly because of energy and fertiliser. Agricultural prices are expected to fall in the baseline, which makes El Niño the upside risk to that view.

Past El Niño episodes have often been supportive for soft commodities. Cocoa, coffee, sugar, palm oil, cotton and rice all depend heavily on rainfall patterns in tropical regions. Yet, inventories, regional weather conditions and substitution effects can change the price response from one crop to another.

Cocoa looks particularly exposed. Ivory Coast and Ghana, the two largest producers, account for roughly half of global cocoa supply. Strong El Niño episodes have historically weighed on cocoa output, sometimes through drought, sometimes through excess rainfall and disease. The last episode showed how damaging that mix can be. Heavy rainfall first increased disease pressure on cocoa trees. Then intense heat and dry Harmattan winds hit already weakened crops. Prices nearly tripled in 2024 and rose above USD 12,000 per metric ton, turning cocoa into one of the most extreme commodity stories of the year.

Palm oil and cotton also offer direct exposure to Asian weather risk. Both are linked to conditions in Indonesia, Malaysia and India. A weak monsoon would quickly change supply expectations.

Coffee is exposed mainly through robusta. Vietnam and Indonesia produce around half of global robusta output, and El Niño usually brings hotter, drier weather during crop development. Arabica is more nuanced. Brazil can benefit from lower frost risk at first, but heat and dryness later in the year can still threaten the next crop.

Sugar is more cushioned. A weaker monsoon in India and Thailand can push prices higher but India could redirect 3–4 million tonnes from ethanol back to sugar, offsetting most of a moderate production loss.

Rice has the most direct link to the monsoon. A weak rainy season in Asia can quickly reduce production expectations and push food-security concerns higher, especially in countries where rice is a staple crop.

Corn depends more on regional weather than on El Niño alone. Dryness in some producing areas can support prices, but the signal is less consistent because other regions may see better growing conditions.

Regarding soybeans, El Niño can create stress in some regions, but Brazil and Argentina may benefit from additional rainfall. That makes the soybean trade less straightforward than rice or palm oil.

Natural gas is the exception. A milder Northern Hemisphere winter usually reduces heating demand and weighs on prices. In 2026, however, that bearish signal has to be balanced against energy-market stress linked to the Strait of Hormuz.

The next catalyst is the Indian monsoon. Rainfall between June and September will shape the outlook for cotton, sugar, rice and palm oil. A normal season would keep part of the El Niño risk contained. A severe shortfall would bring the real upside risk back into focus.

There is also a timing gap between futures and physical markets. Forecasts are still affected by the spring predictability barrier, the period when El Niño models are less reliable before summer signals become clearer. Futures can start pricing 2026–27 weather risks several months ahead, while physical markets remain tied to current inventories, crop conditions and near-term supply-demand balances.

Source: S&P Global