.png)

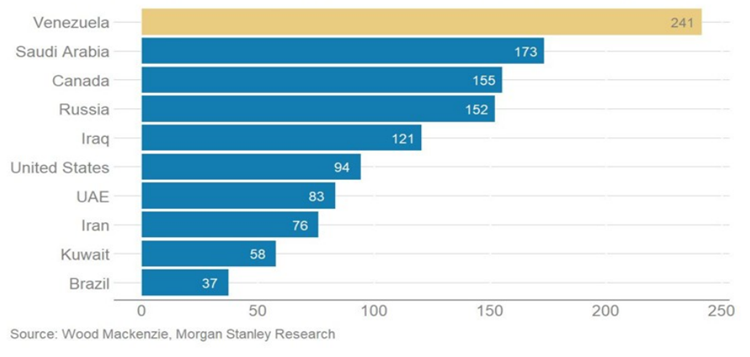

Securing energy resources appears to be a central consideration behind US actions in Venezuela. The country holds the world’s largest proven oil reserves and, according to Wood Mackenzie, has roughly 241 billion barrels of recoverable crude.

Proven Oil Reserves by Country (Billion Barrels)

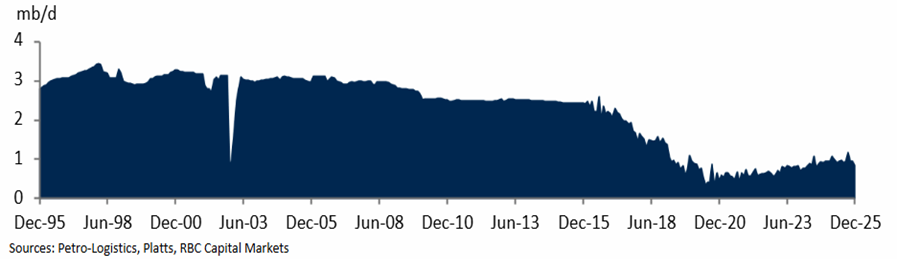

Yet Venezuela’s production history highlights how difficult those barrels are to unlock. Output peaked near 3 million bbl/d in the late 1990s, before political upheaval, strikes, and sector restructuring under Hugo Chávez triggered a long decline. US sanctions imposed from 2017 onward accelerated the collapse, pushing production below 500,000 bbl/d by 2020. Limited sanctions relief in recent years supported a modest rebound, but output today remains around 800,000–900,000 bbl/d.

Historical Total Venezuelan Supply

Expectations of a rapid supply surge risk overstating what is feasible. Iraq took nearly a decade and more than $200 billion to return to pre-war production levels, while Libya has yet to regain its 2010 peak.

Venezuela faces even steeper constraints. Its reserves are dominated by extra-heavy crude, requiring upgrading and imported diluents for transport. Years of underinvestment, sanctions, loss of skilled labour, and the decline of state oil company PDVSA have taken a heavy toll. Aging infrastructure, repeated refinery outages, and limited access to modern drilling and upgrading technology continue to constrain any rapid recovery.

PDVSA has indicated that facilities were not damaged during recent events, suggesting limited immediate disruption. In the near term, oil markets appear able to absorb uncertainty. Inventories are adequate, and OPEC+ has signalled that its 1.65 million bbl/d of voluntary cuts could be reversed if needed.

A pro-US government could enable sanctions relief, renewed foreign investment, and a gradual recovery in exports. However, returning to 3 million bbl/d or more would take years and substantial infrastructure investment. President Trump has already indicated that US oil companies would help operate and develop the Venezuelan oil sector.

Oil markets are tightening structurally. Global consumption now exceeds 101 million bbl/d, led by the United States, China, and rapidly growing demand in India. From a market perspective, the near-term effect may be a temporary rise in geopolitical risk premia. Over time, sidelined Venezuelan supply, close to 1 million bbl/d, could weigh on oil prices and support risk assets.

Source: The Coastal Journal

Source: The Coastal Journal

Venezuela’s resource base extends beyond oil, with deposits of iron ore, bauxite, gold, and nickel, as well as copper, zinc, and rare earth elements, mainly located in the Guayana Shield in the south of the country. Venezuela holds Latin America’s largest gold reserves. Official surveys point to potential scale in battery metals. The government claims reserves of up to 340 million tonnes of nickel alongside large copper resources. Despite this geological potential, commercial mining activity remains minimal. Most non-oil minerals account for less than 1% of national output, and large-scale foreign mining investment is largely absent, leaving much of the country’s mineral wealth undeveloped.

Source: Kalshi

Source: Kalshi

A political transition in Venezuela would primarily affect assets linked to debt restructuring, energy infrastructure, and oil supply chains.

Venezuelan bonds currently trade around 25–35 cents on the dollar, reflecting sanctions risk and legal uncertainty. In a regime-change scenario, several analysts estimate recovery values in the 30–55 cent range, driven by restructuring and sanctions relief.

Source: Bloomberg

Ashmore remains one of the largest institutional holders of Venezuelan sovereign debt. Advisory firms such as Houlihan Lokey, financial advisor to the Venezuela Creditor Committee, and Lazard, a long-standing leader in sovereign restructurings (Greece, Ukraine), would likely benefit from the scale and complexity of any restructuring. In such cases, advisors earn success fees and act as “picks and shovels” to the process. Venezuela’s debt stack is widely viewed as among the most complex on record.

Restarting Venezuela’s oil sector would require rapid rehabilitation of ageing assets. Technip, the historical architect of much of Venezuela’s critical oil infrastructure, is well positioned given its proprietary knowledge, particularly if no-bid or sole-source contracts are used to accelerate repairs. Graham Corporation, which supplies vacuum ejector systems used in heavy-oil upgrading and refining, could also benefit, as processing Venezuela’s crude requires vacuum distillation to prevent it from turning into solid coke.

Before exports can scale, Venezuela must import large volumes of diluent (naphtha or natural gasoline) to move heavy crude through pipelines. Targa Resources, which operates the Galena Park Marine Terminal in Houston, a key LPG and naphtha export hub, would be a logical beneficiary if Venezuela shifts back toward US diluent supply, displacing Iranian flows.