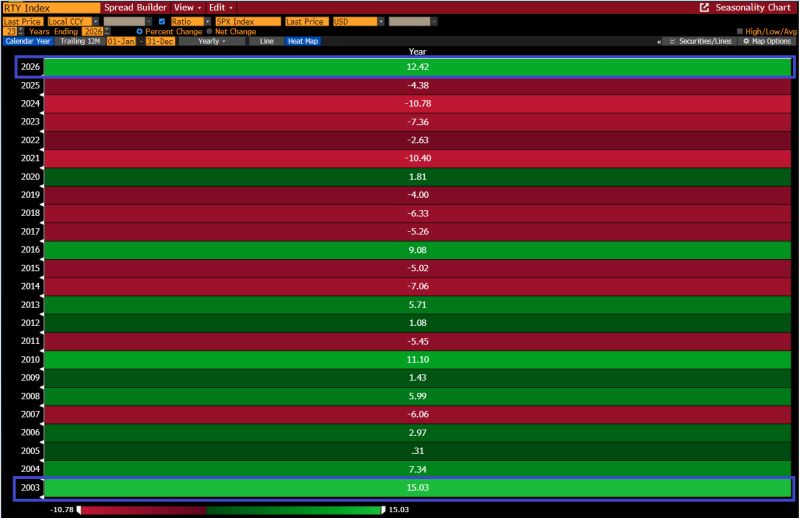

"The Russell 2000 small-caps index is outperforming the S&P500 by ~1,240 bps thus far in 2026: if this holds it would mark the largest year of Small Cap outperformance since 2003" - GS

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

Related Articles

June is shaping up to be their worst month on record. The Roundhill Magnificent Seven ETF ($MAGS) has plunged -12.9% month-to-date, including -5.9% this week alone. But this isn't just another tech selloff. Apple has raised MacBook prices. Microsoft has increased Xbox prices. Both point to the same culprit: rising memory costs driven by the AI infrastructure boom. For the first time, AI CapEx is flowing through the entire value chain and showing up in consumer prices. Now investors are asking a different question How long will markets keep rewarding record AI spending before demanding stronger returns? If confidence fades, the market won't just reprice Big Tech. It will start pricing in AI CapEx cuts. That would lower growth expectations for hyperscalers, hit semiconductor demand, and could trigger a much broader market selloff. The AI trade has been built on ever-higher investment. What happens if Wall Street starts expecting less? This is a key downside risk to monitor. Which also means that you need to be broadly diversified. Source: Dow Jones, Global Markets Investors

The equal-weighted basket of 10 space sector stocks has COLLAPSED -50% since its peak, the largest drawdown since April 2025 and the 2nd-largest since the 2022 bear market. SpaceX, $SPCX, alone is down -32% since its mid-June peak. This comes after retail investors purchased $405 million of SpaceX shares during its first 5 trading days after its June 12 IPO, the largest first-week retail purchases of any IPO ever. Mom-and-pop investors also piled into leveraged ETFs linked to SpaceX, purchasing $65.8 million of the 2x Leveraged Long SpaceX ETF, $SPCH, over its first few trading sessions. The fund is down -56% since the June 16 peak, posted on the 2nd trading day after its launch. Source: Thomas Callum, Topdown charts

Think about that. The market has effectively priced in a clean resolution to one of the largest geopolitical energy shocks in recent history. That's a powerful reminder that markets don't wait for certainty. They price the most likely outcome. But while the geopolitical risk premium may have disappeared from prices, that doesn't necessarily mean the underlying risk has... Stay tuned Source: Blackrock, UBS