.png)

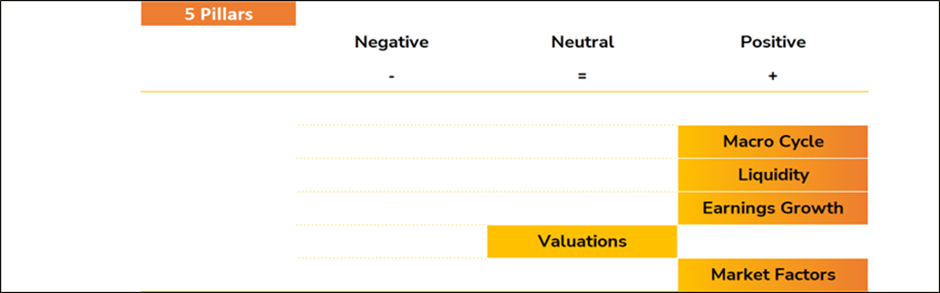

Our asset allocation preferences are based on 5 indicators, including 4 macro and fundamental indicators (leading) and 1 market dynamics (coincident). The weight of the evidence suggests a constructive view on equities (positive). Below we review the main drivers for each of them.

• Macro cycle (POSITIVE): Domestic fiscal stimulus should provide economic support in the US, China, and Eurozone. Trade uncertainties have recently deescalated and macroeconomic data has improved. In the US, macroeconomic data came in stronger than expected, building on an already solid level of economic activity, apart from the labour market. The latest labour market data were reassuring and exceeded consensus, while consumption now-casting indicators point to a rebound at the start of 2026 following the weak December retail print. In Europe, signs of economic recovery are finally appearing in hard macro data, including rising domestic orders and improvements in labor and housing market indicators. In China, domestic consumption remains weak, but the announced cancellation of the rigid 3 red lines” framework for deleveraging the property sector should lift sentiment real estate. Government programs to support domestic demand in the service sector have also just begun. On the industrial side, China’s anti-overcapacity campaign continues to weigh on business sentiment. Meanwhile, the latest figures from Asian emerging markets point to a recovery in the global manufacturing cycle, which is promising for emerging economies more broadly. These developments support our current positive macro assessment, although we continue to monitor elevated geopolitical risks and the likely end of the global central banks’ rate cutting cycle in 2026.

• Liquidity (POSITIVE): liquidity conditions for financial markets remain positive overall. The Fed has ended Quantitative Tightening and is purchasing Treasury bills to ease short-term funding conditions. Continuing global M2 growth and the US dollar’s softness contribute to a supportive liquidity environment for Q1.

• Earnings (POSITIVE): earnings remain a tailwind for equities with more sectors to show earnings growth improvement. Technology stocks will continue to benefit from the adoption of AI, while the “old economy” is set to recover from a low base.

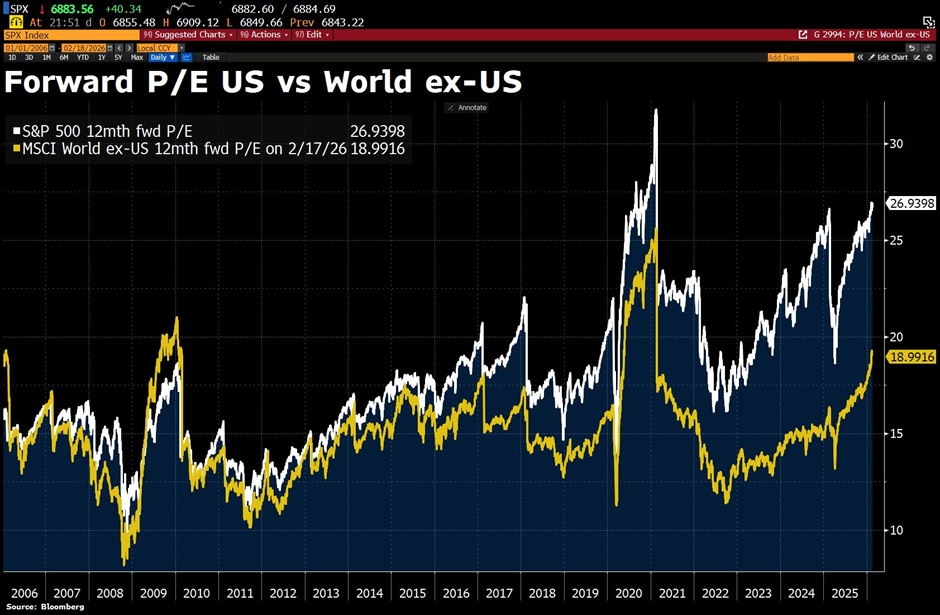

• Valuations (NEUTRAL): US large capitalisation stocks remain expensive while international equities are more reasonably valued. However, equity risk premiums remain low by historical standard in both the US and Europe.

• Market Factors (POSITIVE): symphony indicators are positive at 75% allocation to equities (50% US / 25% EU).

• Earnings (POSITIVE): earnings remain a tailwind for equities with more sectors to show earnings growth improvement. Technology stocks will continue to benefit from the adoption of AI, while the “old economy” is set to recover from a low base.

• Valuations (NEUTRAL): US large capitalisation stocks remain expensive while international equities are more reasonably valued. However, equity risk premiums remain low by historical standard in both the US and Europe.

• Market Factors (POSITIVE): symphony indicators are positive at 75% allocation to equities (50% US / 25% EU).

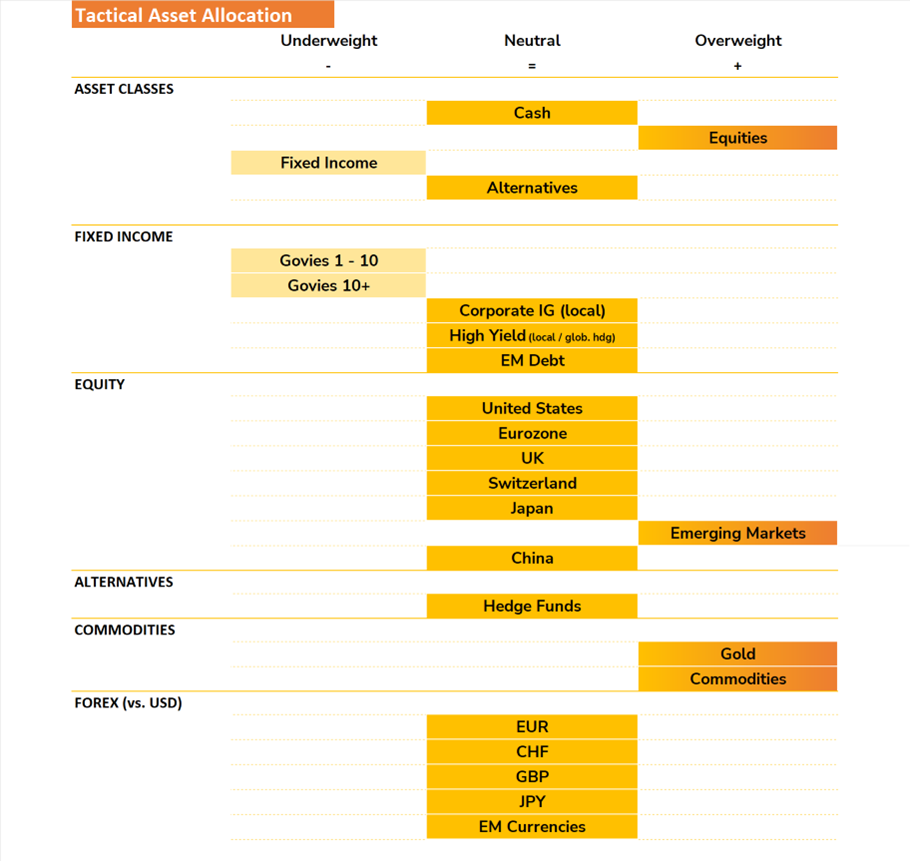

TACTICAL ASSET ALLOCATION (TAA) DECISIONS

The weight of the evidence lead us to keep an overweight stance on equities. Within our asset allocation grids, we are aligning the weights with the recent market drift, leading us to reducing US Equities while increasing the allocation to Emerging Markets equities.

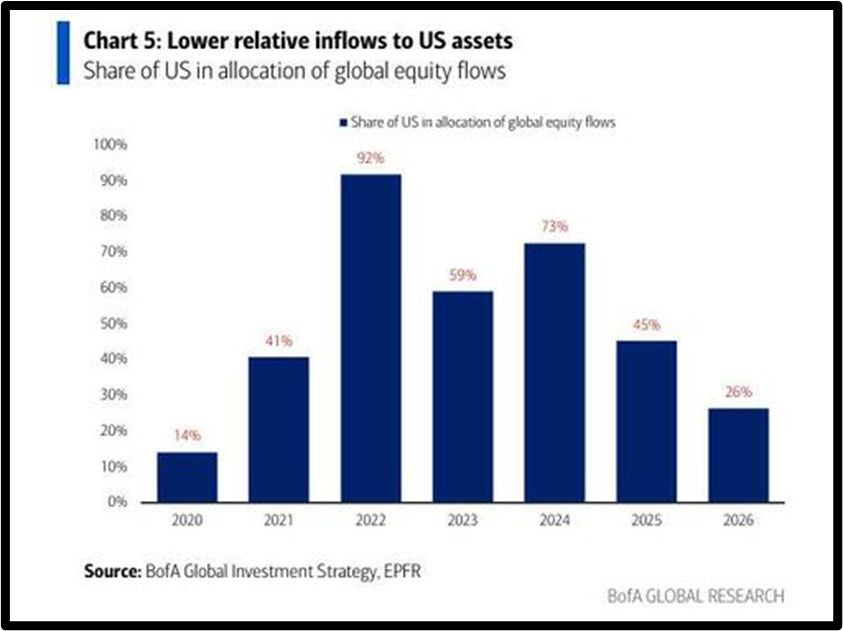

Indeed, while we keep a large allocation to US stocks, we find value outside the US. The shift from US to international markets that started in Q2 of 2025 seems to be gaining momentum, as shown in the chart below.

Source: Strategas

According to Bank of America, we have seen a record 4-week inflow of $64.6bn, mostly Korea (memory stonks) and Japan (reflation narrative).

Looking at the Big Flow to Know, BofA calculated that in 2026, for every $100 of inflows to global equity funds, US stocks have accounted for $26—their lowest share since 2020.

Although global markets have narrowed the gap with the US in recent weeks, US equities still trade at a roughly 40% valuation premium to the rest of the world. That premium could shrink further if big tech companies lose their capital-light appeal due to rising capex and begin to be valued more like capital-intensive businesses.

Source: Bloomberg

From a macro perspective, Emerging Markets and Asia are currently the most compelling regions in our perspective. Aggregate valuations remain compelling and earnings growth expectations are accelerating.

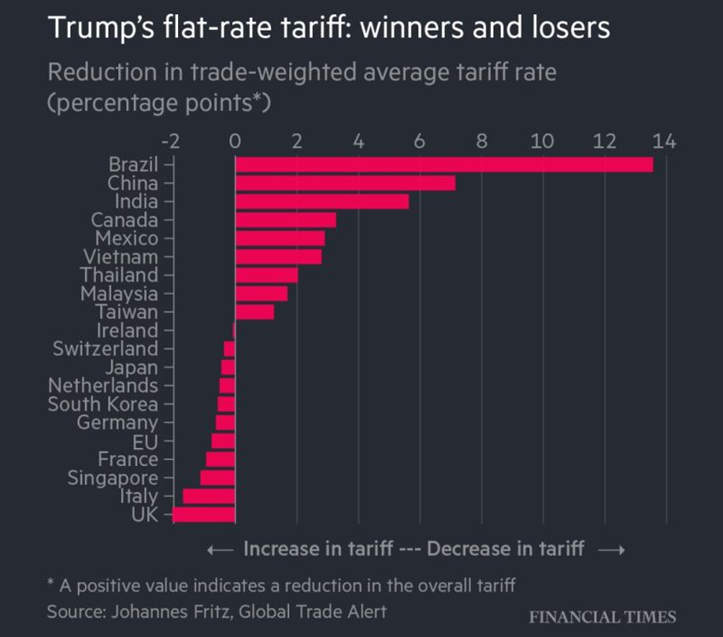

Emerging countries are the beneficiaries of the new 15% tariffs. According to new analysis from Global Trade Alert, the very countries frequently singled out for criticism are set to see their average tariff rates drop the most:

- Brazil: enjoying a massive 13.6% reduction in average tariff rates

- China: seeing a 7.1% reduction

- India: seeing a 5.6% reduction

- Vietnam, Thailand, & Malaysia: set to benefit significantly as previous specific levies are replaced by the blanket rate

In alternatives, we stay overweight gold and overweight commodities.

We stay neutral hedge funds.

We currently maintain an overall underweight stance on Fixed Income, due to a negative view on government bonds. Government bonds are not attractive in the current macroeconomic context, and do not bring reliable diversification in portfolios. We keep a constructive stance on Credit and Emerging Market (EM) debt. EM debt remains supported by global growth dynamic, a weaker US dollar, contained public debt and corporate leverage, as well as strong flows, even if spreads are tight. While Credit markets continue to exhibit tight spread levels despite the recent slight widening, those levels appear coherent with the positive economic growth backdrop and provide interesting carry and absolute yields for a fixed income portfolio.

We are neutral the dollar against all currencies.

On the EUR/USD, we still expect a weaker USD trajectory over the long-term. This is due to a likely looser monetary policy versus the EUR and higher accumulated inflation. Meanwhile, political intentions to weaken the USD remain—attempts to dismantle the institutional set up behind the USD—and the twin deficit persists.

Short term factors balance each other out, but economic policies seem key:

- An inflation differential outlook with US prices rising more than Eurozone -inflation speaks against USD

- A higher interest rate differential and a stronger economic activity in the US vs the EMU speaks for the USD

- The Fed is unlikely to adopt a more dovish stance than markets currently expect, while the ECB is expected to keep policy unchanged

We thus expect the USD to move sideways versus the EUR in the short term and stay negative USD long term.

These short and long-term views are also valid for the USD/CHF.