.png)

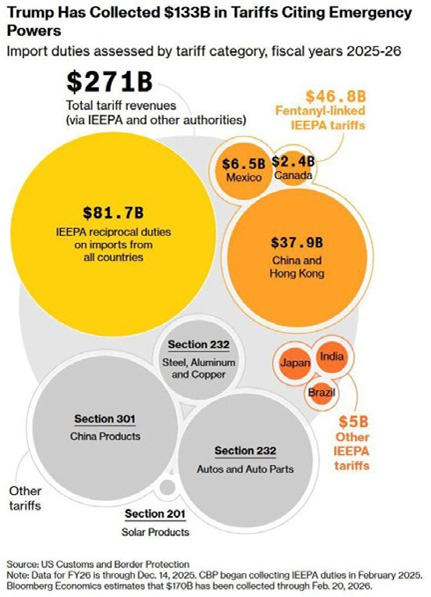

The refund question, however, is unresolved. The Court did not address whether importers are entitled to refunds, leaving that issue to lower courts. There is no established mechanism to return the tariff revenue, and no concrete proposal has been put forward. These payments could be contested in court for months, possibly years. Tariffs collected under emergency powers amount to roughly $133 bn. This represents about 0.45% of the $30 tr US economy, and an even smaller share of the $38.6 tr federal debt. Since November, companies have increasingly filed cases at the Court of International Trade to secure refunds. The legal battle is likely to continue.

Source: Bloomberg

Even as refund claims move through the courts, the decision does not dismantle the overall US tariff regime. Steel and aluminum tariffs imposed under separate authorities remain in place. The administration can also rely on alternative legal tools.

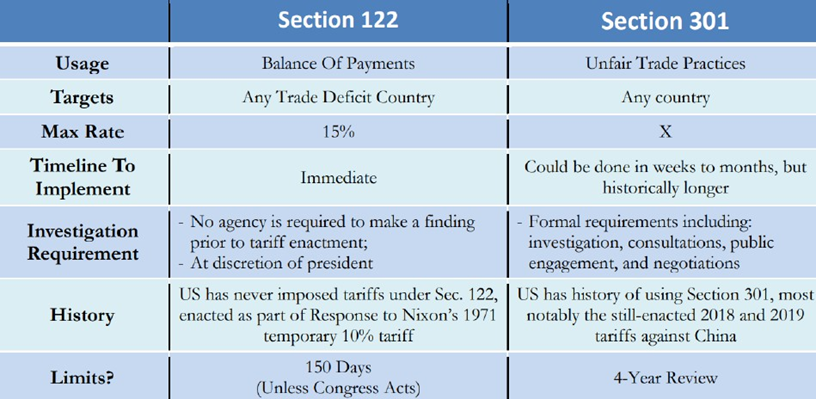

The second step takes longer. While the 15% Section 122 tariff remains in place, the administration plans to use Section 232, which targets national security risks, to launch formal Section 301 investigations addressing unfair trade practices.

Section 301 investigations must be conducted country by country and follow formal steps, which take time and cannot be completed quickly. Completing them within the 150-day Section 122 window will be difficult. The administration may try to speed up the process, but it cannot bypass it entirely. The advantage, however, is legal durability. Unlike IEEPA, Section 301 rests on a well-established statutory basis. If successful, it would provide a firmer and more sustainable foundation for the administration’s tariff policy.

Source: Strategas

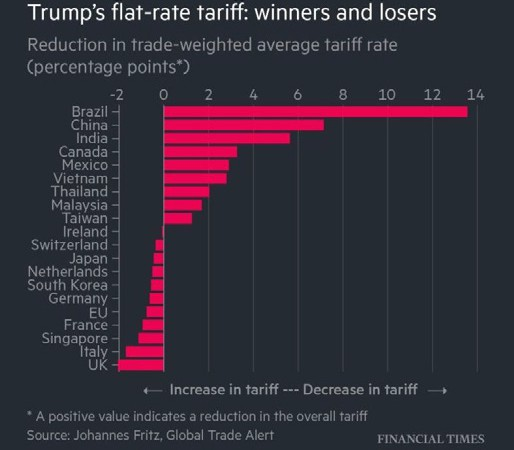

The trade-weighted average US tariff rate now stands at 13.2% under the new 15% Section 122 framework. This compares with 15.3% prior to the Supreme Court ruling and would have declined to 8.3% in the absence of a replacement. While the 15% blanket tariff takes effect this week, the more important development lies in the redistribution of tariff exposure.

The adjustment creates an unexpected realignment. Countries previously facing the highest tariff burdens now see the largest reductions. Brazil’s average tariff burden declines by 13.6%, China’s by 7.1%, and India’s by 5.6%. For Southeast Asian exporters Thailand, Vietnam, and Malaysia, this change is beneficial because their previous targeted tariffs are now replaced with a uniform 15% rate. From an equity perspective, the reduction in tariff pressure improves earnings visibility and strengthens external competitiveness. This should be supportive for equity market performance in these economies.

By contrast, several traditional US allies move in the opposite direction. The UK shifts from 10% to 15%, and parts of the EU and Japan move from lower historical rates into the new 15% framework. The UK, Italy, and Singapore register some of the largest increases in tariff exposure. In trade-weighted terms, the UK faces a 2.1% increase, Italy 1.7%, and Singapore 1.1%, positioning several close US trading partners among the most negatively impacted under the revised framework.

Source: Financial Times

Near-term uncertainty remains around the legal durability of replacement tariffs under Sections 232 and 301. However, Section 122 measures are capped at 15% and expire after 150 days unless extended by Congress. With IEEPA authority removed, the administration can no longer impose immediate, across-the-board tariff increases.

Tariff levels remain elevated relative to historical norms, but the overall burden is lower than before the ruling. The risk of sudden broad escalation has therefore diminished. Tariffs continue to shape trade policy, yet the reduced flexibility to raise them unilaterally lowers uncertainty around future changes.