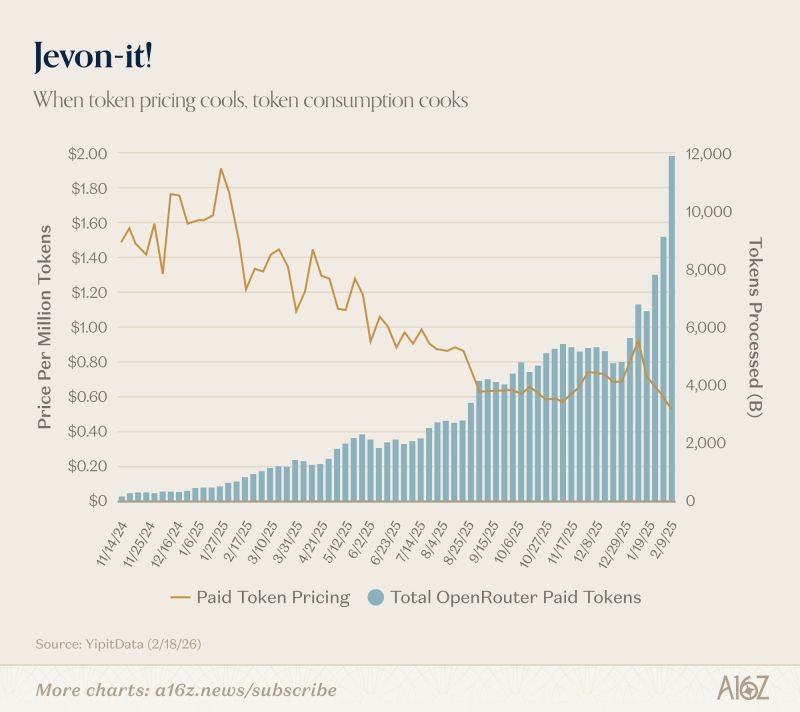

Jevon-paradox Token usage (blue bars) is exploding higher. It started in January when Agentic AI went mainstream with Claude Cowork and Moltbook (OpenClaw).

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document.

Related Articles

A report from Entelligence AI across 2,444 companies shows that for every $1 spent on AI tokens, $0.44 goes to bug fixes, $0.27 to rewriting AI-generated code, and $0.11 disappears into review and merge delays. Companies spending $100,000 on AI tokens and only $18,000 worth is reaching production. The other $82,000 is overhead generated by the tool itself. Lightrun's 2026 report found that 43% of all AI-generated code still requires manual debugging in production even after passing every quality test. Not a single engineering leader surveyed said they were fully confident AI code would behave correctly once deployed. Wall Street is pricing AI as a productivity tool and the data says 82% of the spend never reaches the actual product. SOURCE: @Aiswarya_Sankar Sam Boboev

Source: UBS, TME

Michael Burry reported that the upcoming public listings for SpaceX, OpenAI, and Anthropic are going to pull more capital out of the market than the entire dot-com wave of 2000. Adjusted for inflation, just these three companies will raise more money than the hundreds of tech firms that flooded the market at the peak of the 2000 bubble. The historical data from 2000 shows exactly why this is dangerous for stocks. That year, the market saw 446 IPOs raise a record $108.15 billion. The Nasdaq peaked on March 10, 2000, at the exact moment this massive supply of new shares hit the market, right before crashing 80%. The crash happened because of a simple liquidity drain. When giant companies go public, big institutional funds need cash to buy the new shares. To get that cash, they have to sell their existing stock positions. This creates immediate selling pressure on the most expensive tech stocks. Today, the setup is identical but much more concentrated. Instead of hundreds of small startups spreading out the drain, just three mega companies are absorbing the market's capital. This directly impacts current market leaders. Microsoft has 49% of its $627 billion cloud backlog tied to OpenAI, and Oracle has 54% of its pipeline dependent on it. The same big funds that need to buy the new IPOs are the ones currently holding these tech giants. In the first quarter of 2000, the average IPO nearly doubled on its first trading day because cash was easily available. By the fourth quarter, capital markets dried up. Gross IPO proceeds collapsed 63% in a single quarter, and average first-day gains dropped to just 14% as companies rushed into layoffs and bankruptcies. When an unprecedented amount of money is pulled out of existing stocks to fund a single massive IPO wave, the broader market historically runs out of the liquidity needed to sustain its peak. Source: Bull Theory