WSJ: "Nvidia $NVDA is in talks to provide a roughly $250 billion backstop for OpenAI as part of a massive data-center project

It is one of the most ambitious financial transactions yet in America’s artificial-intelligence boom The guarantees from Nvidia would help the ChatGPT maker lease a 10-gigawatt project that SoftBank’s energy subsidiary is developing in southern Ohio, people familiar with the matter said. In total, the project could cost more than $500 billion, including the chips that would go inside the data centers. It would be the largest data-center project announced to date".

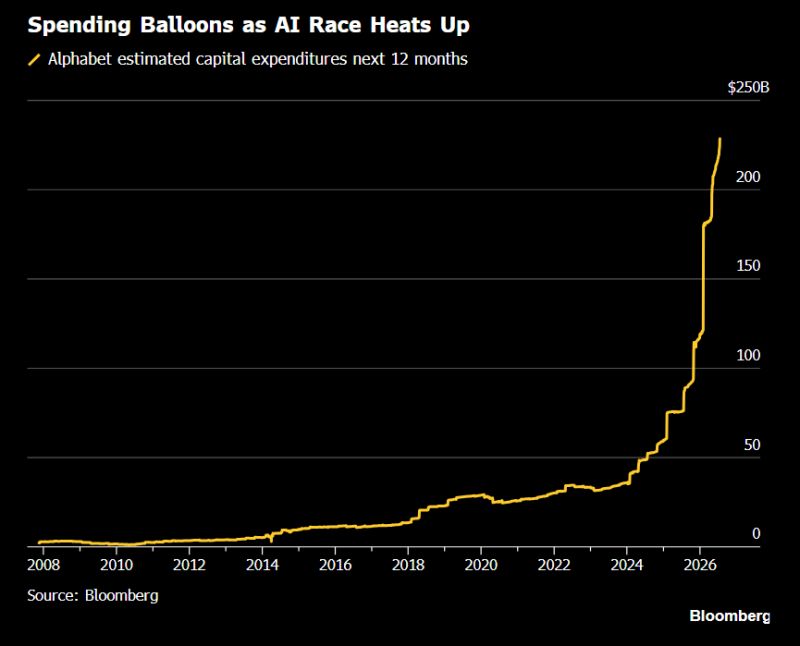

Google's capex is on track to nearly triple in two years

Source: Hedgeye @Hedgeye Bloomberg

Dell is up +11% today after Super Micro's record AI server orders boosted confidence across the entire sector.

$DELL has already built a $51.3 billion AI server backlog and raised its own revenue guidance to $60 billion. Its partnership with Nvidia gives it integrated AI infrastructure that larger enterprises are increasingly betting on. Source: Bull Theory

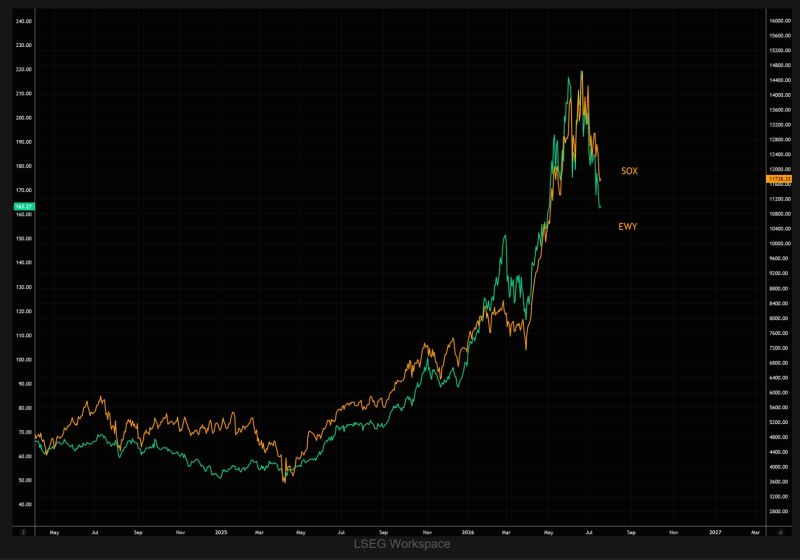

The chart below shows the SOX relative to the EWY iShares Korea ETF

Korea's speculative AI rally remains one of the key drivers of the broader AI trade, making this relationship well worth watching. Source: TME

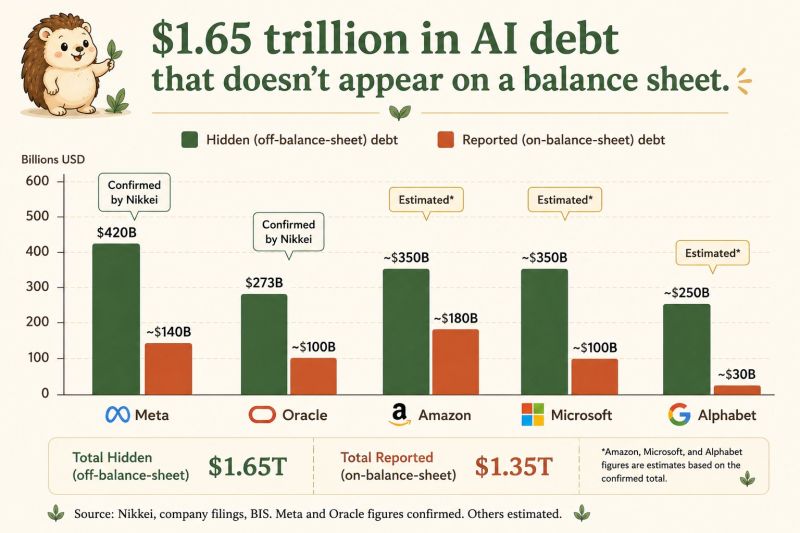

Bi Tech's AI debt may be far larger than investors realize.

A Nikkei investigation found that Alphabet, Microsoft, Amazon, Meta, and Oracle have $1.65 trillion of off-balance-sheet obligations, exceeding the $1.35 trillion of debt they officially report. These commitments—GPU contracts, data center leases, and joint ventures—remain largely invisible under current accounting rules until facilities become operational. Meta alone reportedly has $420 billion in hidden obligations, while Oracle's exposure has exploded over the past four years. The key risk? Investors focusing on earnings may be seeing only part of the picture. As AI infrastructure comes online, these commitments will gradually move onto balance sheets. If AI demand falls short of expectations, expensive assets could face write-downs, with losses ultimately flowing to shareholders and the private credit investors who financed the AI buildout. Source: Hedgie

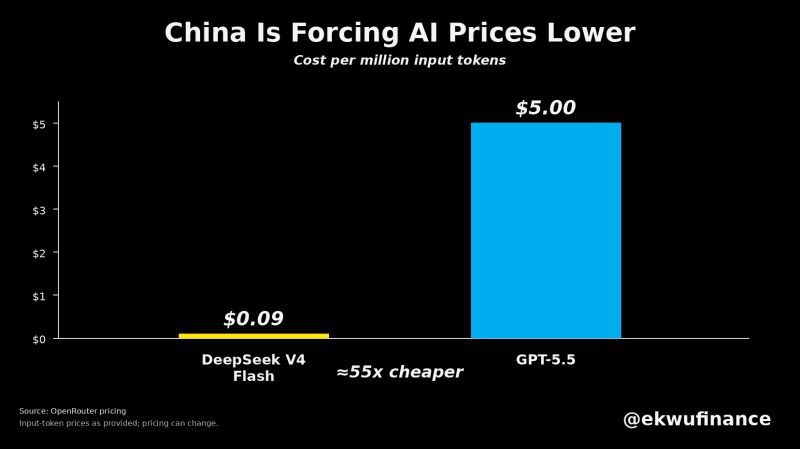

China is forcing AI prices lower

DeepSeek V4 Flash costs $0.09 per million input tokens. GPT-5.5 and Claude Opus 4.8 cost around $5. That's ~55× cheaper. Source: Lukas Ekwueme

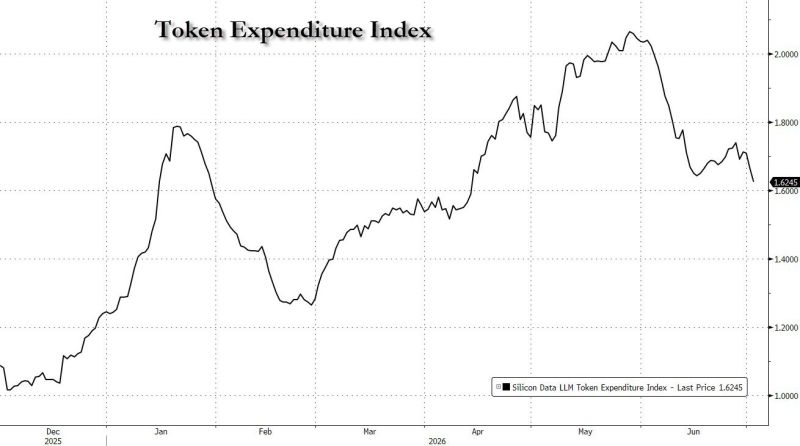

Token spending index rolling over again, down to 2.5 month low

Source: zerohedge

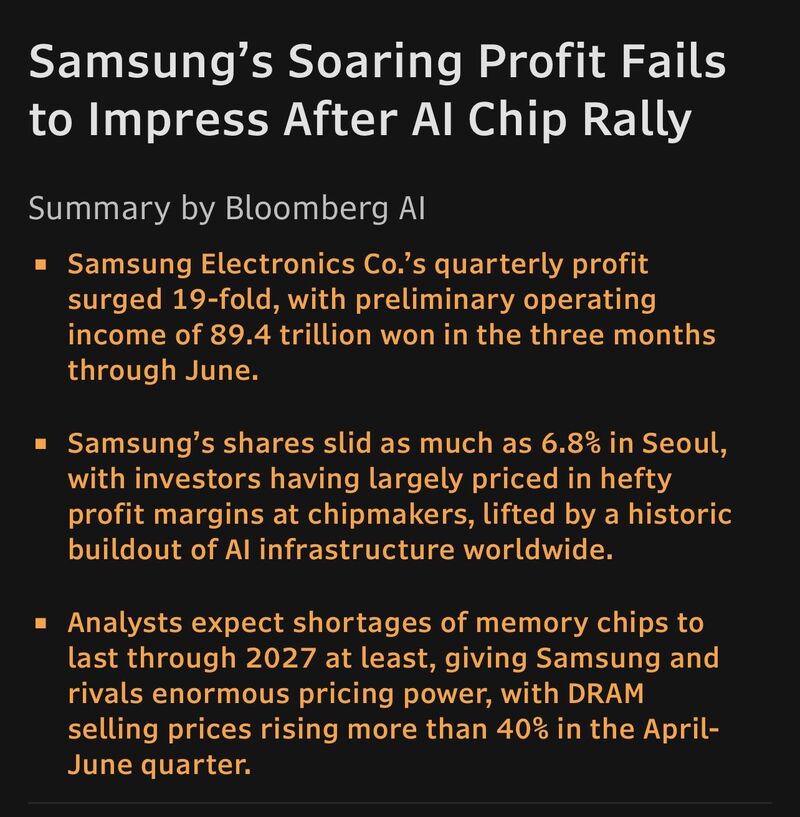

🚨 Samsung just delivered a reality check for the AI trade.

Its quarterly operating profit surged, powered by booming AI memory demand and higher DRAM prices. Analysts still expect memory shortages to persist through 2027. Yet the stock fell. Why? Because in today's market, good isn't good enough when perfection is already priced in. This marks an important shift. The first phase of the AI boom was driven by the obvious bottlenecks: semiconductors, memory, and AI infrastructure. Capital poured into the same names. Nvidia led. The semiconductor index soared. Now those trades are crowded. The fundamentals remain strong, but investors are asking a different question: Can earnings keep exceeding already sky-high expectations? AI isn't over. But the easy money from owning the obvious AI winners may be. Source: Bloomberg, James E. Thorne @DrJStrategy