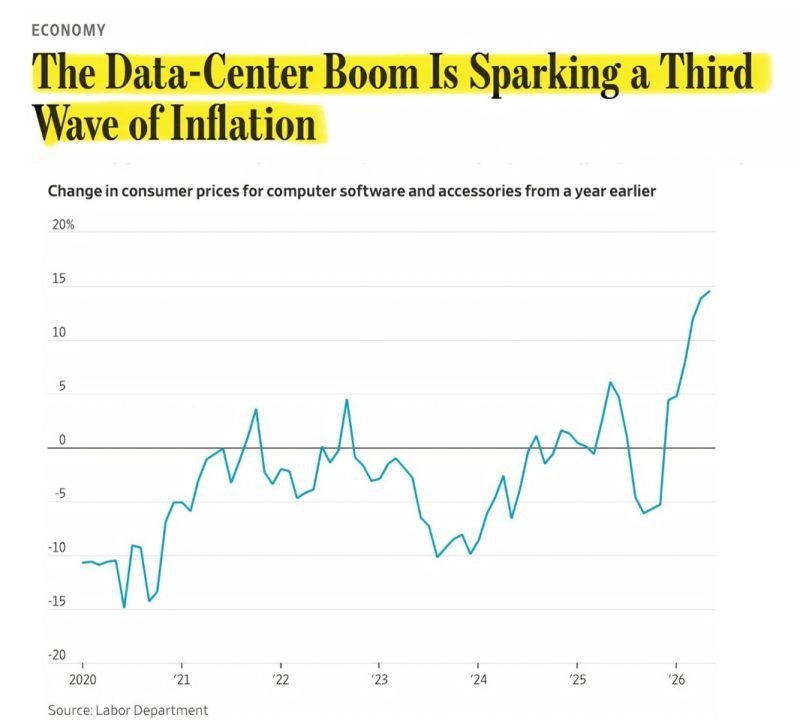

AI MAY BE TRIGGERING THE THIRD WAVE OF INFLATION.

Even Tim Cook recently said the current cost pressures are unlike anything he's seen in more than 40 years in the business. The first inflation wave came from supply chain disruptions. The second was driven by tariffs and energy prices. But this third wave could be different. Tariffs can be negotiated. Oil prices eventually fall as supply catches up. AI infrastructure spending doesn't work that way. This isn't a temporary supply shock. It's a massive demand shock that's still in its early stages. The five largest hyperscalers are expected to spend roughly $741 billion on AI infrastructure this year—up about 75% from last year. Much of that investment hasn't even translated into physical deployments yet. That means today's price pressures may be the beginning, not the peak. Here's why. AI requires enormous amounts of high-bandwidth memory and advanced chips. Those same components are also used in smartphones, laptops, gaming consoles, automobiles, and countless other electronics. As AI companies absorb a growing share of the available supply, they aren't just increasing the cost of AI—they're putting upward pressure on prices across the broader electronics market. We're already seeing signs of that. Apple and Microsoft recently raised prices on products including MacBooks, iPads, and Xbox consoles while pointing to higher component costs and memory constraints. Nintendo and Sony had already announced similar price increases weeks earlier. This isn't one company passing through higher costs. It's an entire hardware industry repricing around the same supply bottleneck. The Federal Reserve's long-term assumption is that AI will eventually offset these inflationary pressures through productivity gains. That may ultimately prove true. But several analysts, including UBS, argue those productivity benefits could take years to fully materialize, while the cost increases are happening today. That leaves the Fed facing a difficult balancing act: keeping interest rates elevated through a period where the technology expected to reduce inflation over the long run may be contributing to higher prices in the short run. If that's the case, this inflation cycle may prove more complex than the tariff- and energy-driven shocks policymakers have dealt with so far. Source: Bull Theory on X

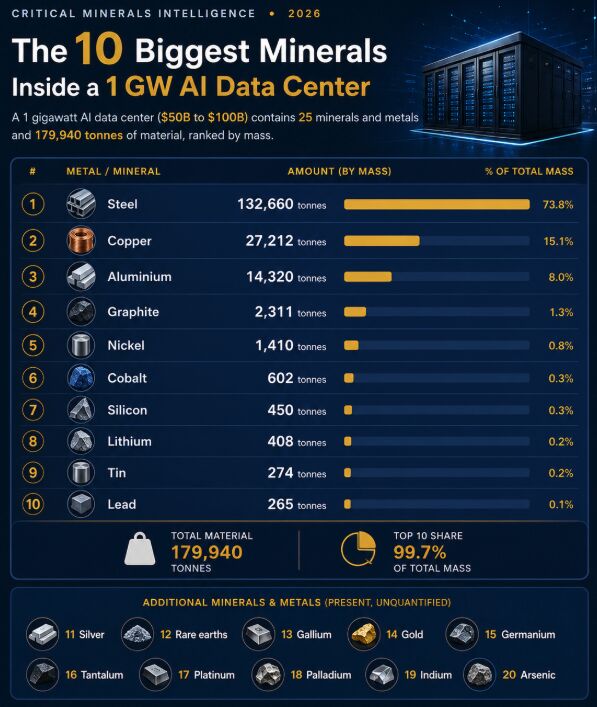

A single AI data center consumes 27,000 tonnes of COPPER.

Everyone talks about AI chips. Almost nobody talks about the metals underneath them. A 1-gigawatt AI data center requires: • 179,940 tonnes of raw materials • 25 different minerals • 132,660 tonnes of steel (74% of the total) • 27,212 tonnes of copper (15% of the build) Copper isn't just another input. It's the circulatory system of AI. Every server. Every rack. Every transformer. Every kilometer of cable. Without copper, AI doesn't run. Then come the other critical materials: → Aluminium: 14,320 tonnes → Graphite → Nickel → Silicon → Cobalt → Lithium → Tin → Lead The top 10 materials account for 99.7% of the total mass. And that's before you add the strategic minerals: • Rare earth elements • Gallium • Germanium • Tantalum • Indium Now zoom out. Hundreds of AI data centers are being built around the world. Every new gigawatt of AI compute means tens of thousands of tonnes of copper have to be mined, refined, and delivered. The AI revolution isn't just a software story. It's a commodities story. And that makes copper miners some of the biggest hidden winners of the AI boom. Before AI can scale... it needs metal. Source: Jack Prandelli on X

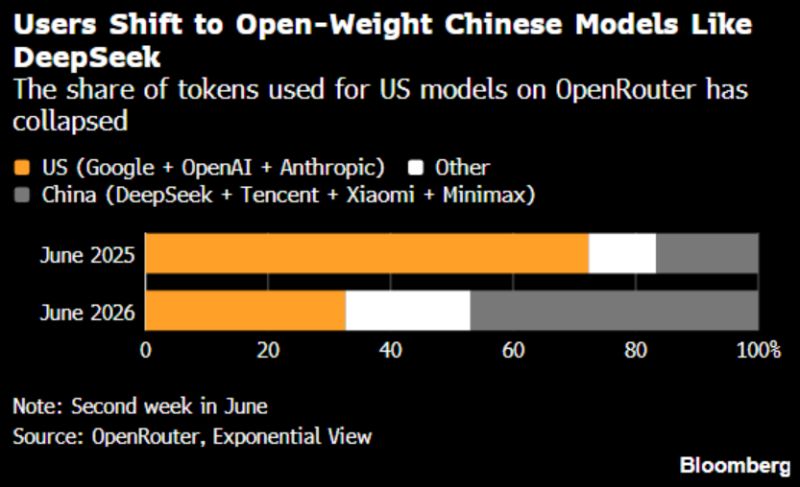

Tokens requested from Google, OpenAI and Anthropic relative to total fell to 33% in June 2026 from 72% a year earlier.

Tokenomics matters, or at least it will soon enough. Chinese AI’s gains in the market are remarkable. Source: Bloomberg, Negligible Capital

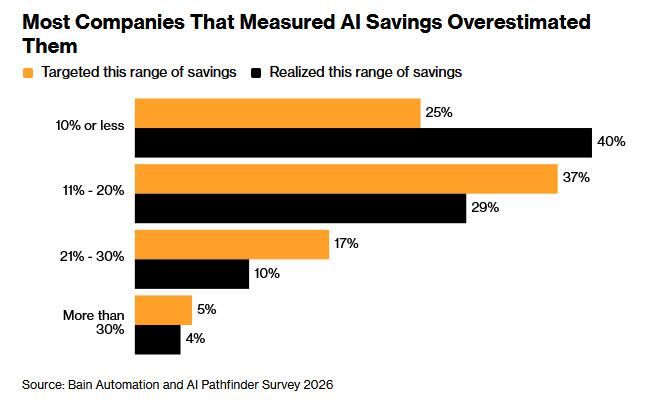

One statistic says everything about today's AI boom:

44% of large companies are funding their next wave of AI investments with savings from AI... that haven't happened yet. — Bain & Company Let that sink in. Almost half of large enterprises are reinvesting projected AI efficiencies before those efficiencies actually exist. That's not necessarily innovation. That's optimism. History has seen this movie before. Every transformational technology—from railroads to the internet—created enormous long-term value. But it also created bubbles where expectations outran reality. AI will absolutely reshape industries. That doesn't mean every AI investment, every AI startup, or every AI stock will justify today's valuations. The winners will survive. Many won't. Markets price the future, not the present. And when expectations become detached from execution, gravity eventually returns. The lesson? 🚀 Believe in AI. ⚠️ Be careful of AI hype. The biggest returns often come from identifying sustainable value—not chasing the last leg of a crowded trade. Innovation is real. Valuations are another story.

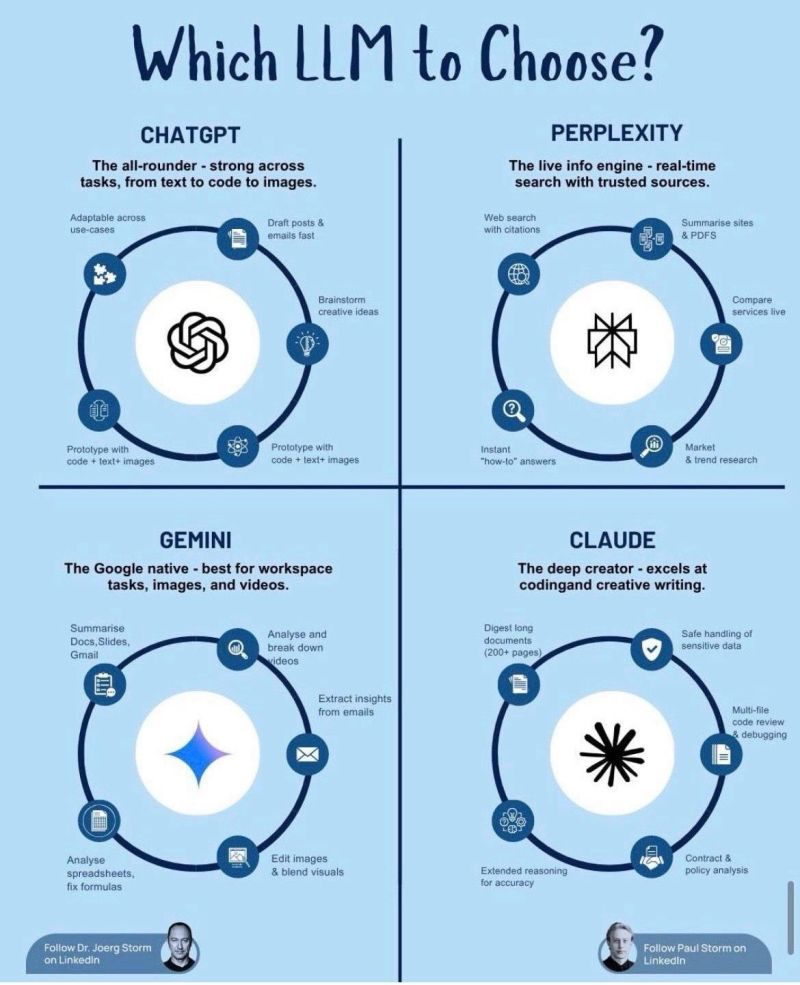

From “Which AI is best?” to “Which AI for which task?"

● ChatGPT → The all-rounder for fast creation ● Perplexity → The fact-checker for trusted data ● Gemini → The workspace genius for Google tools ● Claude → The deep thinker for long, complex tasks Source: Paul Felix Reinsch

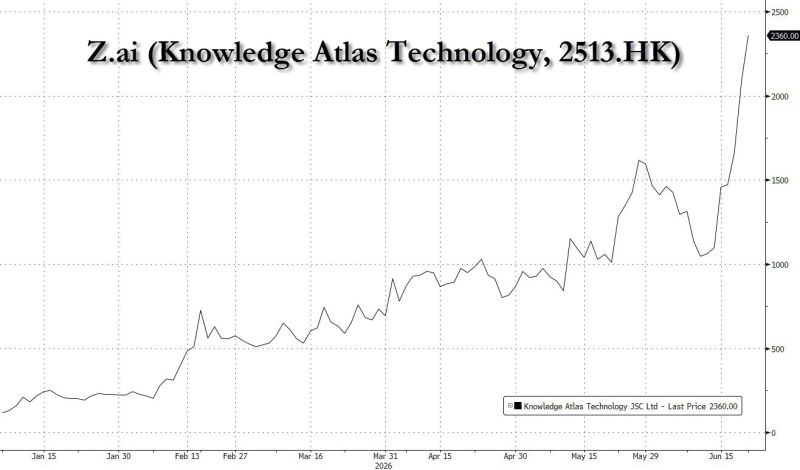

Open-weight models (Zhipu's GLM, DeepSeek, Qwen, MiniMax) are closing the capability gap on the closed "frontier" labs (OpenAI, Anthropic, Google)

The parabolic stock is the market voting on that idea, helped by its newly open-sourced GLM-5.2 and pending Hang Seng Tech Index inclusion. The caveat the meme omits: it's a deeply loss-making company (2025 revenue ~724m HKD, losses ~1.9bn) trading north of 1,000x sales. The sell-side average 12-month target sits ~45% below spot, ratings are split, and a large post-IPO lock-up overhang looms. So the chart reflects Hong Kong AI-IPO mania, index flows and a thin float as much as model quality. Bottom line: a real secular thesis (open models compressing frontier economics) wrapped around a priced-for-perfection single name. Useful as a sentiment gauge — not as proof the open-vs-closed debate is settled. Source: zerohedge

This is the AI leaders-vs-laggard basket

Source: zerohedge, Bloomberg

🚨 The AI race is entering a new phase.

Not because demand is slowing. Because costs are becoming impossible to ignore. Here are the numbers: 📈 Chinese AI models now process ~18.5 trillion tokens per week on OpenRouter. 🇺🇸 US models? Around 6 trillion. That's a 3x gap. Why? • Lower energy costs. • More efficient models. • Aggressive pricing that's reshaping the competitive landscape. Meanwhile, something interesting is happening inside large enterprises. Companies including Amazon, Walmart, Cisco, Uber, and Meta are reportedly introducing internal limits on AI usage as spending exceeds expectations. One striking example: A software company saw its AI bill jump 7x overnight after moving from a flat-rate subscription to usage-based pricing. Suddenly, the true cost of AI became visible. And this is only the beginning. 📊 Goldman Sachs estimates AI agents could increase token consumption by 24x by 2030. That creates a fundamental challenge: AI demand may keep exploding... while AI budgets become increasingly constrained. The next competitive advantage won't just be building the smartest models. It will be building the most cost-efficient ones. The AI story is evolving: ➡️ From "Who has the biggest model?" ➡️ To "Who delivers the lowest cost per useful output?" The winners of the next AI wave may not be those with the most compute... ...but those who make intelligence affordable at scale. Do you think AI spending is finally reaching a reality check, or is this just a temporary pause before the next investment wave? Source: FT, Global Markets Investors